PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445522

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1445522

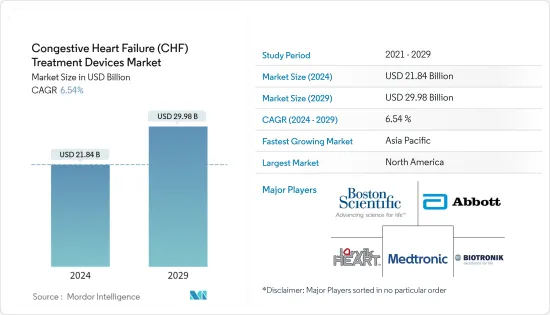

Congestive Heart Failure (CHF) Treatment Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2024 - 2029)

The Congestive Heart Failure Treatment Devices Market size is estimated at USD 21.84 billion in 2024, and is expected to reach USD 29.98 billion by 2029, growing at a CAGR of 6.54% during the forecast period (2024-2029).

Due to the high infection rate and lockdown regulations brought on by the COVID-19 pandemic, surgical procedures have been affected. The congestive heart failure market has been impacted, and patients with cardiovascular disorders have further encountered delays in diagnosis and treatment as a result of fewer individuals visiting hospitals and diagnostic centers. For instance, a March 2022 research study published in the National Library of Medicine found that between February 2020 and January 2021, there was a 52.7% decrease in the volume of adult cardiac surgery and a 65.5% decrease in elective cases, which shows the negative impact of COVID-19 on the cardiac surgical procedures. But as the COVID-19 instances subsided and the market began to recover, the number of operations increased. Various research has been conducted by scientists to find the impact of COVID-19 infection and cardiac diseases. A group of scientists in the United States researched COVID-19 patients and published the article in the National Library of Medicine in April 2022. The article also stated that COVID-19 hospitalized patients possess a high risk of the development of atrial or ventricular arrhythmias in the United States. Thus, such risk of arrhythmias among hospitalized patients in the country increased the demand for CHF treatment devices used for various cardiac procedures. Thus, such increasing chances of CHF due to COVID-19 are expected to increase the market growth.

An increasing patient pool of cardiovascular diseases (CVDs) and a surge in congestive heart failure (CHF) cases are prime factors augmenting the growth of the CHF treatment devices market. The surge in CVDs leads to a rising in risk related to heart failure, thereby driving the demand for devices used in the treatment of CHF. Sedentary lifestyles, junk food consumption, and mental stress are other key factors associated with the development of CVDs. The increasing geriatric population is also leading to an upsurge in the cases of CVDs, worldwide. For instance, as per the November 2021 report published by the Asian Pacific Observatory on Health Systems and Policies, by 2050, about one-fourth population of the Asia-Pacific region will be 60 years or older due to the decreasing fertility rate in the region and increasing longevity which is further expected to increase the burden of the cardiovascular diseases and thus, driving the demand for the effective and advanced treatment procedures thus increasing market growth. This demographic is prone to chronic diseases, including CHF. It is characterized by low immunity levels, thereby serving as a high-impact rendering driver for the growth of these products over the forecast period. As a result, the latest treatments available in cardiac care are expected to increase the lifespan of the elderly population.

The World Heart Federation report published in 2022 stated that cardiovascular disease, which includes heart disease and stroke, is the most common non-communicable disease globally. Thus, the increasing prevalence of cardiovascular diseases is responsible for boosting the growth of the market. According to a June 2021 article by the National Library of Medicine, age-standardized estimates of cardiovascular disease prevalence in Italy are similar to the global prevalence. Still, the country's crude prevalence is almost two times higher than the global prevalence (12.9% vs. 6.6%). The increasing prevalence of cardiovascular diseases is expected to increase the demand for various congestive heart failure devices, such as pacemakers which are expected to increase the market growth over the forecast period.

Additionally, technological advancements in CHF treatment devices are working in favor of the overall market. For instance, in August 2022, released data from Abbott stated that the HeartMate 3 heart pump improves patients' lives by at least five years and represents a definite life-saving alternative for those dealing with severe disease. The MOMENTUM 3 experiment was the randomized clinical research ever conducted to evaluate long-term outcomes in patients being treated for severe heart failure with a left ventricular assist device (also known as an LVAD or heart pump). Thus, such clinical trials provide insight into the technological advancement in the market, which increases the market growth over the forecast period.

However, the high cost of CHF treatment devices may hamper the growth of the market over the forecast period.

Congestive Heart Failure (CHF) Treatment Devices Market Trends

The Implantable Pacemakers Segment is Expected to Hold a Significant Market Share Over the Forecast Period

The implantable pacemaker is a device that uses electrical impulses to regulate the heart rhythm. An internal pacemaker is one in which the electrodes are placed in the heart, and electronic circuitry and the power supply are implanted within the body. Moreover, by regulating the heart's rhythm, a pacemaker can often eliminate the symptoms of bradycardia, which means individuals often have more energy and less shortness of breath.

The major factors driving the growth of implantable pacemakers include rising cardiovascular patients and technological advancements, such as exclusive algorithms to accurately detect and reduce the likelihood of atrial fibrillation. Atrial fibrillation, often called AFib or AF, is the most common type of heart arrhythmia. An arrhythmia is when the heart beats too slowly, too fast, or in an irregular way. According to a press release by CDC in October 2022, it is estimated that 12.1 million people in the United States will have AFib in 2030. Similarly, in February 2022, a research article published in the National Library of Medicine stated that It had been estimated that 6-12 million people worldwide will suffer this condition in the US by 2050 and 17.9 million people in Europe by 2060. Thus, the increasing prevalence of AFib is expected to increase the demand for CHF devices for treatment, which is expected to increase market growth over the forecast period.

The market leaders are involved in the advancement of technology with clinical trials. For instance, in December 2021, Boston Scientific Corporation initiated the MODULAR ATP clinical trial to evaluate the safety, performance, and effectiveness of the mCRM Modular Therapy System, which includes the EMPOWER Modular Pacing System (MPS), which is designed to be the leadless pacemaker capable of delivering both bradycardia pacing support and anti-tachycardia pacing (ATP). Thus, such clinical trials are expected to increase market growth over the forecast period by providing advanced technology.

Thus, all the above factors, such as increasing CVDs and clinical trials, are expected to contribute to the good growth of this segment over the forecast period.

North America is Expected to Hold a Significant Market Share Over the Forecast Period

Some of the factors driving the market growth in the North American region include increasing demand for congestive heart failure (CHF) treatment, the increasing prevalence of target disorders, high expenditure on healthcare, and an increase in awareness among the population regarding the availability of treatment devices. Moreover, a strong clinical pipeline, favorable reimbursement policies for therapeutic products, and higher adoption of these devices are the other factors anticipated to promote revenue growth.

The increasing prevalence of heart diseases in the region is one of the key factors in market growth. For instance, as stated by the American Heart Association 2021 journal, it is estimated that by the year 2035, more than 130 million adults in the United States will have some type of heart disease. Additionally, the statistics provided by the Heart and Stroke Foundation of Canada in February 2022 state that there are 750,000 people currently living with heart failure, and 100,000 people are diagnosed with this condition each year in Canada. Thus, the increasing prevalence of heart diseases is expected to increase the adoption of devices for the treatment of such diseases, which is expected to increase market growth over the forecast period.

Furthermore, initiatives such as product approvals are expected to increase market growth. For instance, in April 2022, Abbott received the Food and Drug Administration (FDA) approval for leadless pacemaker technology with its new Aveir single-chamber VR pacemaker system, which features increased battery longevity over current commercially available leadless pacemakers. Thus, such approvals are expected to increase market growth as it provides new innovative technology in the market. Similarly, in June 2021, the American College of Cardiology (ACC) and GE Healthcare collaborated to support and participate in ACC's Applied Health Innovation Consortium to build a roadmap for artificial intelligence (AI) and digital technology in cardiology and develop new strategies for improved health outcomes.

Thus, considering the aforementioned factors, such as the increasing prevalence of CVDs, and initiatives by key market players are expected to fuel the market growth in the North American region over the forecast period.

Congestive Heart Failure (CHF) Treatment Devices Industry Overview

The congestive heart failure (CHF) treatment devices market is moderately consolidated, in terms of competition, with major international companies competing with each other. Companies are more focused on developing high-utility products which can deliver personalized care. Some of the major market players include Jarvik Heart Inc., Medtronic PLC, Boston Scientific Corporation, Abbott Laboratories, and Biotronik SE & Co. KG, among others.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Cardiovascular Diseases (CVD)

- 4.2.2 Surge in Number of Congestive Heart Failure (CHF) Cases

- 4.2.3 Advent of Technologically Advanced Products

- 4.3 Market Restraints

- 4.3.1 High Cost of Devices

- 4.4 Porter Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers/Consumers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitute Products

- 4.4.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION (Market Size by Value - USD million)

- 5.1 Product

- 5.1.1 Ventricular Assist Devices (VADs)

- 5.1.1.1 LVAD

- 5.1.1.2 RVAD

- 5.1.1.3 BiVAD

- 5.1.2 Counter Pulsation Devices

- 5.1.3 Implantable Cardioverter Defibrillators

- 5.1.3.1 Transvenous ICD

- 5.1.3.2 Subcutaneous ICD

- 5.1.4 Pacemakers

- 5.1.4.1 Implantable

- 5.1.4.2 External

- 5.1.5 Cardiac Resynchronization Therapy

- 5.1.5.1 Cardiac Resynchronization Therapy-Defibrillators (CRT-D)

- 5.1.5.2 Cardiac Resynchronization Therapy-Pacemakers (CRT-P)

- 5.1.1 Ventricular Assist Devices (VADs)

- 5.2 Geography

- 5.2.1 North America

- 5.2.1.1 United States

- 5.2.1.2 Canada

- 5.2.1.3 Mexico

- 5.2.2 Europe

- 5.2.2.1 Germany

- 5.2.2.2 United Kingdom

- 5.2.2.3 France

- 5.2.2.4 Italy

- 5.2.2.5 Spain

- 5.2.2.6 Rest of Europe

- 5.2.3 Asia-Pacific

- 5.2.3.1 China

- 5.2.3.2 Japan

- 5.2.3.3 India

- 5.2.3.4 Australia

- 5.2.3.5 South Korea

- 5.2.3.6 Rest of Asia-Pacific

- 5.2.4 Middle-East and Africa

- 5.2.4.1 GCC

- 5.2.4.2 South Africa

- 5.2.4.3 Rest of Middle-East and Africa

- 5.2.5 South America

- 5.2.5.1 Brazil

- 5.2.5.2 Argentina

- 5.2.5.3 Rest of South America

- 5.2.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles

- 6.1.1 Abbott Laboratories

- 6.1.2 Berlin Heart GmbH

- 6.1.3 Biotronik SE & Co. KG

- 6.1.4 Boston Scientific Corporation

- 6.1.5 Jarvik Heart Inc.

- 6.1.6 Lepu Medical Technology(Beijing)Co.,Ltd.

- 6.1.7 Magenta Medical Ltd

- 6.1.8 MEDICO S.R.L.

- 6.1.9 Medtronic PLC

- 6.1.10 Oscor, Inc.

- 6.1.11 OSYPKA MEDICAL

- 6.1.12 Shree Pacetronix Ltd

7 MARKET OPPORTUNITIES AND FUTURE TRENDS