PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035124

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035124

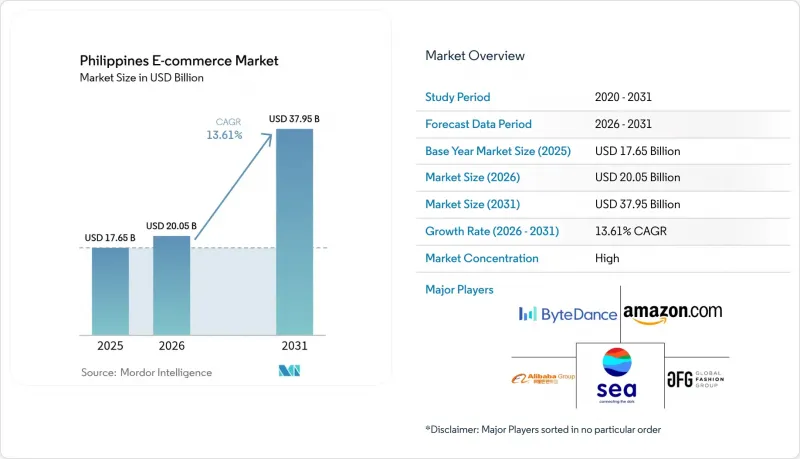

Philippines E-commerce - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Philippines e-commerce market size is expected to grow from USD 17.65 billion in 2025 to USD 20.05 billion in 2026 and is forecast to reach USD 37.95 billion by 2031 at 13.61% CAGR over 2026-2031.

Its growth has been propelled by nationwide mobile-wallet penetration that exceeded 65% in 2024, the rollout of provincial logistics mini-hubs that shorten delivery routes across 7,641 islands, and policy targets that position digital trade as a core engine for the PHP 1.2 trillion e-commerce sector. Intensifying platform competition, the rapid uptake of Buy-Now-Pay-Later (BNPL) credit, and the concerted push to utilize the Regional Comprehensive Economic Partnership (RCEP) for tariff-free cross-border shipments have further expanded the Philippines e-commerce market's addressable base. Merchant digitization programs led by the Department of Trade and Industry (DTI) accelerated SME onboarding, while AI-enhanced live-commerce tools raised conversion rates, especially in fashion and beauty streams.

Philippines E-commerce Market Trends and Insights

Soaring Mobile-Wallet Penetration Transforms Payment Infrastructure

GCash amassed 94 million users by early 2025, while Maya widened its wallet with credit extensions such as the Maya Black card, raising digital payments to 52.8% of retail transaction volume in 2023. Visa's integrations let 87% of surveyed Filipinos fund wallets using cards, blurring lines between traditional banking and app-based finance. Seamless linkages between wallets and marketplaces have lowered merchant onboarding hurdles, pushed unbanked consumers into formal channels, and enlarged the Philippines e-commerce market's daily active buyer pool. Super-app roadmaps now embed savings, credit, and insurance modules that tether users to commerce ecosystems. This payment ubiquity has shortened checkout flows and lifted repeat-purchase frequency.

Logistics Mini-Hubs Enable Provincial Commerce Expansion

Courier groups such as J&T Express and Ninja Van scaled fleet capacity and opened sub-depot networks in Cebu, Iloilo, and Davao, cutting delivery lead-times by up to 30% relative to Metro Manila fulfilment routes. Central Visayas, which logged 7.3% GRDP growth in 2024, now enjoys same-day delivery for high-velocity SKUs, unlocking pent-up provincial demand. Mini-hub economics also reduce failed-delivery rates in remote municipalities, boosting merchant margins. Enhanced route density improves asset utilization, persuading platforms to list bulky and perishable goods that previously faced prohibitive freight costs. The model is replicable across Mindanao's secondary cities, indicating sustained upside for the Philippines e-commerce market.

High Last-Mile Costs Outside NCR

Deliveries to far-flung islands often exceed 15% of order value, eroding margins on low-ticket grocery and FMCG items that are climbing at 14.67% CAGR. Multi-modal routes involving inter-island ferries and provincial roads remain vulnerable to typhoons, creating fulfillment unpredictability. Although mini-hubs narrow cost gaps, network density in Luzon-Other and Mindanao is still thin, compelling couriers to levy surcharges. Consumers outside NCR also show lower disposable income, compressing price ceilings for delivery fees. Without accelerated infrastructure spending under public-private logistics partnerships, last-mile friction will keep suppressing the Philippines e-commerce market's rural penetration.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Cross-Border Social-Commerce Adoption

- AI-Powered Live-Commerce Engagement

- Fragmented VAT Compliance Among Merchants

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

B2C held 91.72% of the Philippines e-commerce market share in 2025, translating into sizeable absolute GMV, yet the B2B vertical is expanding at 14.76% CAGR and is set to unlock larger basket values. The Philippines e-commerce market size associated with electronic procurement for manufacturers and distributors is rising as firms migrate away from fax and phone orders in favor of digital portals that consolidate spending and integrate credit terms.

Corporate buyers now demand embedded finance-UnionBank's API partnerships allow invoice-based lending directly within procurement dashboards-signaling that payment rails will shape B2B platform selection. Investor appetite for wholesaler-centric marketplaces such as Growsari, which raised USD 17.8 million, underscores confidence that B2B service depth will compress B2C's historical dominance in the Philippines e-commerce market.

Mobile wallets represented 64.74% of transaction value in 2025, but Other Payment Modes are forecast to log a 15.45% CAGR, expanding the Philippines e-commerce market size accessible to underbanked shoppers. BillEase, already profitable in 2023, embedded its installment option across 10,000 merchants, enabling small-ticket splits without card credentials.

Wallet operators like Maya now white-label BNPL plugins, merging credit scoring with wallet KYC data to mitigate default risk. Cash-on-delivery has shrunk as trust in digital refunds improves, while real-time bank transfers receive regulatory backing under the InstaPay rail. Payment providers that deliver holistic ecosystems-credit, savings, insurance-will capture the Philippines e-commerce market's next growth wave.

The Philippines E-Commerce Market Report is Segmented by Business Model (B2B, and B2C), Payment Mode for B2C E-Commerce (Debit/Credit Cards, Mobile Wallets, and More), Product Category for B2C E-Commerce (Beauty and Personal Care, Consumer Electronics, and More), and Device Type for B2C E-Commerce (Smartphones, Desktops/Laptops, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Shopee Philippines (Sea Ltd.)

- Lazada Philippines (Alibaba Group)

- TikTok Shop Philippines (ByteDance Ltd.)

- Zalora Philippines (Global Fashion Group)

- Amazon Global Selling Philippines (Amazon .com Inc.)

- Alibaba.com Philippines (Alibaba Group)

- Globe Fintech Innovations Inc. (GCash)

- Maya Philippines Inc.

- SM Retail Inc.

- Robinsons Retail Holdings Inc.

- UnionBank of the Philippines

- GrabExpress Philippines

- Ninja Van Philippines

- J&T Express Philippines

- Entrego Fulfillment Solutions Inc.

- LBC Express Holdings Inc.

- PayMongo Philippines

- Dragonpay Corporation

- Xendit Philippines

- Meta Platforms Inc. (Facebook Marketplace PH)

- Kumu Holdings Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring mobile-wallet penetration (GCash, Maya)

- 4.2.2 Logistics mini-hubs in provincial cities

- 4.2.3 Rapid cross-border social-commerce adoption

- 4.2.4 Digital-payment mandates for government fees

- 4.2.5 MSME onboarding incentives (tax perks)

- 4.2.6 AI-powered live-commerce engagement

- 4.3 Market Restraints

- 4.3.1 High last-mile costs outside NCR

- 4.3.2 Fragmented VAT compliance among merchants

- 4.3.3 Data-privacy skills gap in SMEs

- 4.3.4 Port congestion and customs delays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of New Entrants

- 4.7.5 Threat of Substitutes

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Business Model

- 5.1.1 B2B

- 5.1.2 B2C

- 5.2 By Payment Mode for B2C E-commerce

- 5.2.1 Credit/Debit Cards

- 5.2.2 Mobile Wallets

- 5.2.3 Other Payment Modes for B2C E-commerce

- 5.3 By Product Category

- 5.3.1 Beauty and Personal Care

- 5.3.2 Consumer Electronics

- 5.3.3 Fashion and Apparel

- 5.3.4 Food and Beverages

- 5.3.5 Furniture and Home

- 5.3.6 Toys, DIY and Media

- 5.3.7 Other Product Categories for B2C E-commerce

- 5.4 By Device Type for B2C E-commerce

- 5.4.1 Smartphone

- 5.4.2 Desktop/Laptop

- 5.4.3 Other Device Types for B2C E-commerce

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Shopee Philippines (Sea Ltd.)

- 6.4.2 Lazada Philippines (Alibaba Group)

- 6.4.3 TikTok Shop Philippines (ByteDance Ltd.)

- 6.4.4 Zalora Philippines (Global Fashion Group)

- 6.4.5 Amazon Global Selling Philippines (Amazon .com Inc.)

- 6.4.6 Alibaba.com Philippines (Alibaba Group)

- 6.4.7 Globe Fintech Innovations Inc. (GCash)

- 6.4.8 Maya Philippines Inc.

- 6.4.9 SM Retail Inc.

- 6.4.10 Robinsons Retail Holdings Inc.

- 6.4.11 UnionBank of the Philippines

- 6.4.12 GrabExpress Philippines

- 6.4.13 Ninja Van Philippines

- 6.4.14 J&T Express Philippines

- 6.4.15 Entrego Fulfillment Solutions Inc.

- 6.4.16 LBC Express Holdings Inc.

- 6.4.17 PayMongo Philippines

- 6.4.18 Dragonpay Corporation

- 6.4.19 Xendit Philippines

- 6.4.20 Meta Platforms Inc. (Facebook Marketplace PH)

- 6.4.21 Kumu Holdings Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment