PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836567

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836567

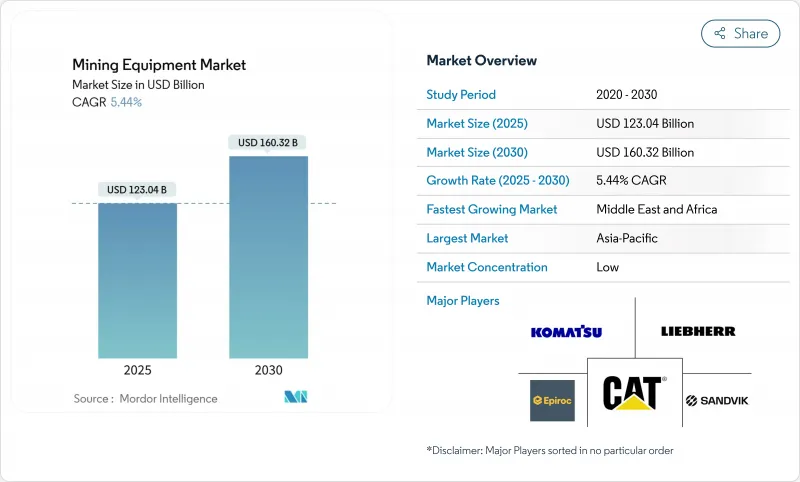

Mining Equipment - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The mining equipment market is valued at USD 123.04 billion in 2025 and is forecast to reach USD 160.32 billion by 2030, reflecting a 5.44% CAGR (2025-2030).

Growth is anchored in operators' drive to cut emissions, raise productivity, and secure the critical minerals needed for clean-energy supply chains. Electrified and autonomous fleets are moving from pilot to scale as regulators tighten carbon rules and investors reward low-emission strategies. Africa's rapid build-out of copper, cobalt, and lithium capacity, Asia Pacific's large mineral base, and North America's technology upgrades collectively reinforce demand for new-generation equipment. Competitive dynamics are intensifying as traditional OEMs accelerate digital services while fast-moving Chinese brands use cost advantage to seize share in price-sensitive segments.

Global Mining Equipment Market Trends and Insights

Surging Demand for Critical Minerals for Battery Supply Chains

Copper demand is on track to climb 70% to more than 50 million tons by 2050, amplifying the pull for high-capacity haul trucks, energy-efficient crushers, and AI-guided drills. IEA indicates that clean-energy goals will require a fourfold lift in critical-mineral output by 2040, ensuring a multiyear replacement cycle for precision equipment. AI-enhanced exploration is trimming drilling expense significantly and quadrupling discovery hit rates, enabling mine planners to commit capital earlier and drive fresh orders into the mining equipment market. Asian battery-gigafactory build-outs and North America's reshoring push generate localized hotspots for mineral-processing systems.

Accelerated Mine-Electrification Mandates

Canada, Chile, and Australia have set emission-reduction targets that force operators to retire diesel fleets faster than depreciation schedules originally assumed. Fortescue's plan to deploy 360 Liebherr T 264 battery-electric haul trucks by 2030 underscores the scale of this pivot. Field trials show electric machines can cut OPEX by 7-15% owing to fewer moving parts and eliminated fuel costs, findings echoed by the Future Battery Industries Cooperative Research Centre. Competitive stakes are rising as specialised BEV newcomers challenge incumbent OEMs, propelling the mining equipment market toward a permanently altered technology baseline.

Ore-Grade Deterioration Inflating Total Cost-of-Ownership

Falling grades force operators to move more material for the same output, raising energy use and spurring demand for higher-capacity shovels, conveyors, and mills. Global mining energy consumption could climb two to eightfold by 2060 if grade decline and mineral demand trends continue. OEMs are countering with energy-efficient comminution circuits, but the capital intensity of such systems challenges mid-tier miners, slowing procurement in certain deposits.

Other drivers and restraints analyzed in the detailed report include:

- Sustained CAPEX Up-cycle in African Projects

- Emissions-Linked Financing: Lowering the Cost of Capital

- Grid Constraints Delaying BEV Deployment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Underground Mining Equipment is expected to grow at a CAGR of 6.36% from 2025 to 2030 as battery-electric loaders and haul trucks mitigate ventilation costs and improve air quality. Sandvik's record BEV order book in 2025 signals an inflection point. The mining equipment market size for surface machines remains the largest with 67.25%, anchored by bulk iron ore and copper operations. Equipment OEMs continue to refine AI-sorting systems that raise ore recovery in crushing-screening lines, aligning with miners' drive to offset grade decline.

Second-generation electric drills and breakers integrate remote operation, advancing safety in high-risk headings. Ultra-class surface haul trucks dominate open-pit economics; yet the heavier batteries needed for BEV versions spur research into lighter composite housings and on-board fast-charging, a trend set to redefine product roadmaps across the mining equipment market.

Fully autonomous fleets are climbing at 14.2% CAGR, catalysed by persistent labour shortages and safety imperatives. More than 600 autonomy-enabled trucks are already in commercial service, with routes scripted by high-precision GPS and collision-avoidance algorithms. The mining equipment market benefits as each autonomous retrofit unlocks incremental spend on sensors, software, and connectivity.

Manual equipment accounts for the largest market share of 82.15% in 2024. However, semi-autonomous machines provide an intermediate step, letting operators switch between manual and remote control to fit geology or workforce constraints. The installed base of connected assets is slated to more than double from 1.3 million units in 2023 to 2.7 million by 2028, signaling a long runway for autonomy-ready hardware and analytics subscriptions.

The Mining Equipment Market Report is Segmented by Equipment Type (Surface Mining Equipment, Underground Mining Equipment, and More), Automation Level (Manual Equipment, Semi-Autonomous Equipment, and More), Power Train (ICE, BEV, and More) Power Output (Less Than 5HP and More), Application (Metal Mining, Mineral Mining, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific holds 60.90% of the mining equipment market in 2024, spearheaded by China's vast open-pits and Australia's high-tonnage iron ore corridors. Local OEM champions XCMG and SANY now leverage low-cost scale and domestic demand to penetrate export regions, pressuring incumbent price structures. Australia's push for solar-powered mines supports early adoption of battery-electric load-hauls, particularly in the Pilbara, where studies show 70% diesel-use cuts from integrated PV-storage micro-grids.

In Middle East and Africa represents the fastest-growing cluster, registering a 7.55% CAGR through 2030. In Africa, DRC cobalt, Zambian copper, and South African platinum projects anchor greenfield spending, while infrastructure gaps spur modular design requests. Government-community partnerships that channel revenue into local roads and power links further anchor fleet investment decisions, intensifying the pull on the mining equipment market.

North America and Europe trade on technology intensity and regulation. The United States incentivises automation through tax allowances, pushing miners to retrofit tele-remote drills across Nevada gold operations. Europe frames procurement around carbon neutrality, catalysing orders for zero-emission haulage prototypes. South America, dominated by Chilean and Brazilian majors, invests steadily although macro volatility trims some budgets. Grid-strength constraints in Andean highlands slow BEV scalability, yet hybrid power solutions keep momentum for electrification-ready platforms.

- Caterpillar Inc.

- Komatsu Ltd.

- Sandvik AB

- Liebherr-International AG

- Epiroc AB

- Hitachi Construction Machinery Co., Ltd.

- Atlas Copco AB

- Volvo Construction Equipment AB

- Metso Outotec Oyj

- Doosan Infracore Co.

- BEML Ltd.

- XCMG Group

- SANY Heavy Equipment

- Hyundai Construction Equipment Co.

- Terex Corporation

- Joy Global (Komatsu Mining)

- CNH Industrial N.V.

- JCB Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for critical minerals for battery supply chains (Asia & US)

- 4.2.2 Accelerated mine electrification mandates in Canada, Chile & Australia

- 4.2.3 Sustained CAPEX up-cycle in African copper, cobalt & lithium projects

- 4.2.4 Emissions-linked financing lowering cost of capital for electric fleets

- 4.2.5 Recovery of greenfield iron-ore projects in Western Australia & Brazil

- 4.2.6 Shift to predictive maintenance driving aftermarket parts pull-through

- 4.3 Market Restraints

- 4.3.1 Ore-grade deterioration inflating total cost-of-ownership

- 4.3.2 Grid constraints at remote mines delaying BEV deployment

- 4.3.3 Talent shortage for autonomous haul-truck operations

- 4.3.4 Uneven permitting timelines for new surface mines (EU & US)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD Billion)

- 5.1 By Equipment Type

- 5.1.1 Surface Mining Equipment

- 5.1.2 Underground Mining Equipment

- 5.1.3 Mineral Processing Equipment

- 5.1.4 Drills & Breakers

- 5.1.5 Crushing, Pulverizing & Screening

- 5.1.6 Loaders & Haul Trucks

- 5.2 By Automation Level

- 5.2.1 Manual Equipment

- 5.2.2 Semi-Autonomous Equipment

- 5.2.3 Fully Autonomous Equipment

- 5.3 By Powertrain Type

- 5.3.1 Internal-Combustion Engine Vehicles

- 5.3.2 Battery-Electric Vehicles

- 5.3.3 Hybrid Vehicles

- 5.4 By Power Output

- 5.4.1 Less than 500 HP

- 5.4.2 500 - 1,000 HP

- 5.4.3 Above 1,000 HP

- 5.5 By Application

- 5.5.1 Metal Mining

- 5.5.2 Mineral Mining

- 5.5.3 Coal Mining

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Chile

- 5.6.2.3 Peru

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Spain

- 5.6.3.5 Sweden

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Indonesia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 South Africa

- 5.6.5.4 Egypt

- 5.6.5.5 Turkey

- 5.6.5.6 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Caterpillar Inc.

- 6.4.2 Komatsu Ltd.

- 6.4.3 Sandvik AB

- 6.4.4 Liebherr-International AG

- 6.4.5 Epiroc AB

- 6.4.6 Hitachi Construction Machinery Co., Ltd.

- 6.4.7 Atlas Copco AB

- 6.4.8 Volvo Construction Equipment AB

- 6.4.9 Metso Outotec Oyj

- 6.4.10 Doosan Infracore Co.

- 6.4.11 BEML Ltd.

- 6.4.12 XCMG Group

- 6.4.13 SANY Heavy Equipment

- 6.4.14 Hyundai Construction Equipment Co.

- 6.4.15 Terex Corporation

- 6.4.16 Joy Global (Komatsu Mining)

- 6.4.17 CNH Industrial N.V.

- 6.4.18 JCB Ltd.

7 Market Opportunities & Future Outlook