PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836598

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836598

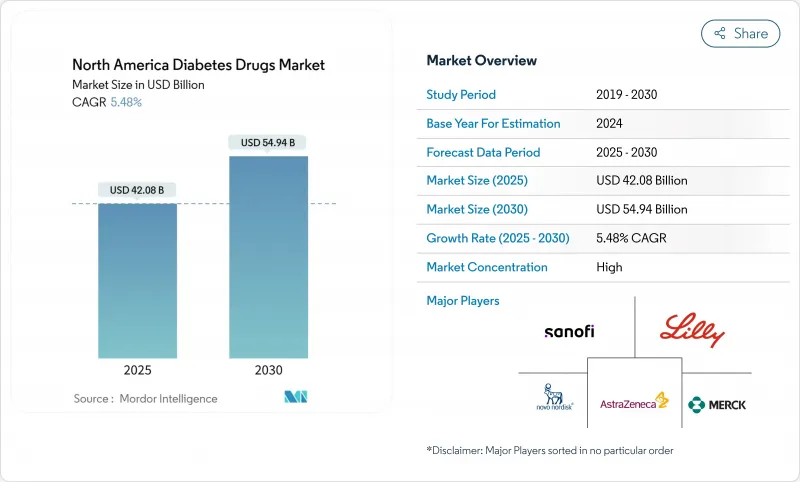

North America Diabetes Drugs - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America diabetes drugs market stood at USD 42.08 billion in 2025 and is forecast to reach USD 54.94 billion by 2030, translating to a 5.48% CAGR during the period.

A growing convergence of diabetes and obesity treatment, coupled with rapid uptake of next-generation GLP-1 receptor agonists, is providing much of the forward momentum. U.S. prescription drug spending climbed 10.2% in 2024, and GLP-1s already rank as the largest and fastest-growing therapeutic spend category.Oral anti-diabetics continue to control the majority of therapy volumes even as injectable innovation accelerates, and biosimilar insulin introductions are compressing prices in key segments. Tight Medicare negotiations, state price-cap statutes, and payer prior-authorization rules are reshaping formulary choices, yet therapeutic innovations keep total spending on an upward trajectory. Mexico's emergence as a manufacturing hub and the expansion of online pharmacies are also altering competitive economics and patient access across the region.

North America Diabetes Drugs Market Trends and Insights

Increasing adoption of GLP-1 agonists in obese T2DM

GLP-1 receptor agonists unify obesity and diabetes management, a nexus relevant to more than 88% of people with Type 2 diabetes. Tirzepatide reached roughly 12% prescription share of glucose-lowering drugs by end-2023, and its popularity among non-diabetic weight-management users underscores the therapeutic blur between metabolic indications. Dual GLP-1/GIP activity delivers greater body-weight and HbA1c reductions than single-target drugs, while emerging triple-agonists such as retatrutide have posted 24% weight loss at 48 weeks, setting new clinical benchmarks. Fast-tracked FDA approvals for wider cardiometabolic indications are expanding reimbursement horizons and encouraging prescribers to adopt these therapies earlier in care pathways.

Reimbursement expansion for dual & triple incretins

Payers are recalibrating formularies to recognize the cardiovascular and renal benefits of dual and triple incretins. Medicare's price negotiations apply greater pressure on legacy oral agents, while newer GLP-1s gain Tier-preferred coverage, thus lowering out-of-pocket costs for seniors.Commercial insurers now classify obesity as a medical condition, unlocking pharmacotherapy budgets previously reserved for diabetes. Employer health plans are bundling obesity and diabetes care contracts tied to outcome metrics, reinforcing utilization growth.

Payer prior-authorization throttles GLP-1 volumes

US payers continue to impose multi-step therapy rules that delay or deny GLP-1 initiation despite favorable clinical profiles, leading to patient drop-out and slower overall market penetration. Medicare Advantage plans remain especially cautious in approving weight-management uses, preserving utilization caps that curb early growth.

Other drivers and restraints analyzed in the detailed report include:

- Biosimilar insulin price wars accelerate uptake

- CGM-linked dosing algorithms spur drug adherence

- API tariff risk from China supply concentration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Oral agents secured 68.23% of the North America diabetes drugs market in 2024 and are projected to expand at 7.52% CAGR through 2030, sustaining leadership despite injectable breakthroughs. SGLT-2 inhibitors such as canagliflozin continue to gain based on cardio-renal outcome data and Health Canada labeling updates.

Non-insulin injectables are climbing rapidly on the back of GLP-1, dual GIP/GLP-1, and emerging triple-agonist classes. Triple-mechanism drugs are positioned as premium therapies offering weight, cardiovascular, and renal benefits, thereby lifting value per prescription within the North America diabetes drugs market. Alpha-glucosidase inhibitors retain a niche among geriatric cohorts, and combination pills that merge multiple mechanisms aim to simplify dosing and boost adherence.

Therapies for Type 2 diabetes continue to dominate revenue, yet Type 1 options are showing the strongest incremental gains. Integration of weekly semaglutide with automated insulin delivery lifted time-in-range metrics from 69.4% to 74.2%, a meaningful clinical advance. The resulting enthusiasm is expanding the North America diabetes drugs market size for Type 1 adjuncts. Gene-therapy programs aimed at beta-cell regeneration are still pre-commercial but underscore the pipeline depth.

The North America Diabetes Drugs Market Report is Segmented by Drug Class (Insulins [Biosimilar Insulin and More], Non-Insulin Injectable, Oral Anti-Diabetic and Combination Drugs), Diabetes Type (Type 1 Diabetes and Type 2 Diabetes), Drug Origin (Branded and Generic/Biosimilar), Distribution Channel (Hospital Pharmacies, Retail Pharmacies and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Novo Nordisk

- Eli Lilly and Company

- Sanofi

- AstraZeneca

- Merck

- Boehringer Ingelheim

- Bristol-Myers Squibb

- Pfizer

- Johnson & Johnson

- Takeda Pharmaceuticals

- Teva Pharmaceutical Industries

- Astellas Pharma

- GlaxoSmithKline

- Amgen

- Viatris

- MannKind

- Adocia SA

- Innovent Biologics

- Sun Pharmaceuticals Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Adoption of GLP-1 Agonists in Obese T2DM

- 4.2.2 Reimbursement Expansion for Dual & Triple Incretins

- 4.2.3 Biosimilar Insulin Price Wars Accelerate Uptake

- 4.2.4 CGM-linked Dosing Algorithms Spur Drug Adherence

- 4.2.5 Employer Obesity-Diabetes Bundled Contracts

- 4.2.6 US-Mexico Near-shoring of Pen-fill Finish Lines

- 4.3 Market Restraints

- 4.3.1 Payer Orior-authorization Throttles GLP-1 Volumes

- 4.3.2 API Tariff Risk from China Supply Concentration

- 4.3.3 Litigation Over Pancreatitis & Thyroid C-cell Tumors

- 4.3.4 Rising State Drug Price-cap Legislation

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technology Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Drug Class

- 5.1.1 Insulins

- 5.1.1.1 Basal / Long-acting

- 5.1.1.2 Bolus / Fast-acting

- 5.1.1.3 Traditional Human Insulin

- 5.1.1.4 Biosimilar Insulin

- 5.1.2 Non-Insulin Injectables

- 5.1.2.1 GLP-1 Receptor Agonists

- 5.1.2.2 Dual / Triple Agonists (e.g., Tirzepatide, Retatrutide)

- 5.1.2.3 Amylin Analogues

- 5.1.3 Oral Anti-Diabetics

- 5.1.3.1 Biguanides

- 5.1.3.2 SGLT-2 Inhibitors

- 5.1.3.3 DPP-4 Inhibitors

- 5.1.3.4 Alpha-Glucosidase Inhibitors

- 5.1.3.5 Sulfonylureas

- 5.1.3.6 Meglitinides

- 5.1.3.7 Thiazolidinediones

- 5.1.4 Combination Drugs

- 5.1.1 Insulins

- 5.2 By Diabetes Type

- 5.2.1 Type 1 Diabetes

- 5.2.2 Type 2 Diabetes

- 5.3 By Drug Origin

- 5.3.1 Branded

- 5.3.2 Generic / Biosimilar

- 5.4 By Distribution Channel

- 5.4.1 Hospital Pharmacies

- 5.4.2 Retail Pharmacies

- 5.4.3 Online Pharmacies

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.3.1 Novo Nordisk A/S

- 6.3.2 Eli Lilly & Co.

- 6.3.3 Sanofi S.A.

- 6.3.4 AstraZeneca plc

- 6.3.5 Merck & Co.

- 6.3.6 Boehringer Ingelheim

- 6.3.7 Bristol Myers Squibb

- 6.3.8 Pfizer Inc.

- 6.3.9 Johnson & Johnson (Janssen)

- 6.3.10 Takeda Pharmaceutical

- 6.3.11 Teva Pharmaceuticals

- 6.3.12 Astellas Pharma

- 6.3.13 GSK plc

- 6.3.14 Amgen Inc.

- 6.3.15 Viatris Inc.

- 6.3.16 MannKind Corporation

- 6.3.17 Adocia SA

- 6.3.18 Innovent Biologics

- 6.3.19 Sun Pharma

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment