PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836665

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1836665

Vitamin E - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

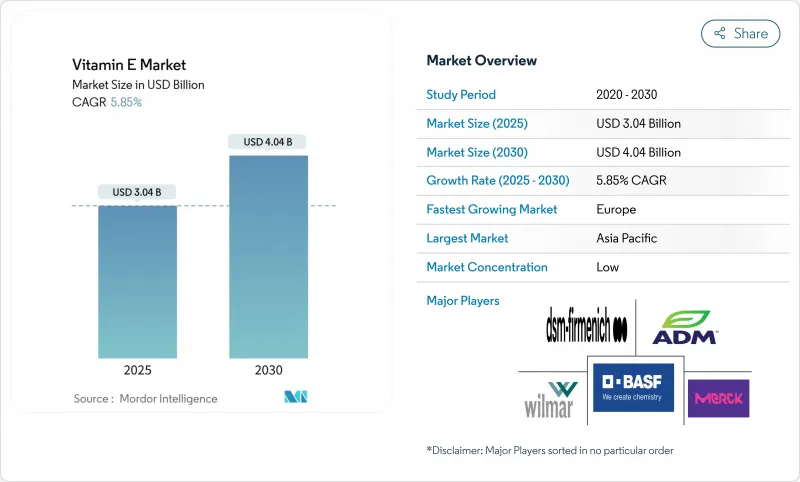

The global vitamin E market is anticipated to be valued at USD 3.04 billion in 2025, and is expected to reach USD 4.04 billion by 2030, growing at a CAGR of 5.85%.

The market growth stems from increased consumer awareness of vitamin E's health benefits, including its antioxidant properties, immune system support, and skin health benefits, driving demand in dietary supplements and functional foods. The market has seen a shift toward plant-based vitamin E sources, such as sunflower, soybean, and safflower oils, aligning with consumer preference for natural and clean-label products. The cosmetics and personal care industry's incorporation of vitamin E for its moisturizing and anti-aging properties has contributed to market expansion. The fortification of foods and beverages with essential nutrients has created opportunities in functional food segments. The market growth is further supported by urbanization, higher disposable incomes, and increased health awareness in emerging economies, particularly in the Asia-Pacific region.

Global Vitamin E Market Trends and Insights

Growing Aging Population Driving Demand for Dietary Supplements

The global demographic shift toward an aging population influences the consumption patterns of vitamin E (tocopherols and tocotrienols), as adults over 65 require increased antioxidant supplementation to combat age-related oxidative stress. The Food and Drug Administration (FDA)'s classification of tocopherols as generally safe substances under 21 CFR 182.3890 establishes regulatory compliance parameters for supplement manufacturers. This regulatory framework facilitates the development of vitamin E formulations specifically designed for the aging demographic. The demographic transition generates consistent market demand that persists beyond economic cycles, positioning vitamin E supplementation as a stable growth category in the nutraceuticals market. According to World Bank data, the United States population aged 65 and over increased from 16.92% in 2022 to 17.43% in 2023, strengthening the demand for vitamin E supplementation products .

Increasing Consumer Awareness about Preventive Healthcare and Nutritional Supplements

Growing awareness of micronutrient deficiencies through consumer education and digital health platforms has increased recognition of vitamin E deficiency symptoms, including skin problems, vision issues, and immune system impairment. The Philippines' implementation of vitamin classification guidelines, which set vitamin E limits at 536 mg per day, demonstrates regulatory adaptation to increased consumer demand for fortified foods and supplements. These regulations provide opportunities for manufacturers to develop formulations that optimize dosages while maintaining safety standards. The increased focus on preventive healthcare, driven by pandemic-related health awareness, has established vitamin E as an essential ingredient in wellness products.

High Production Costs and Raw Material Price Volatility Affect Market Profitability

The high production costs associated with extracting and processing Vitamin E, particularly from natural sources, significantly constrain the global Vitamin E market's growth and profitability. The extraction of natural Vitamin E from vegetable oils (soybean, sunflower, wheat germ, and safflower) requires complex processes of extraction, purification, and stabilization, which increase operational and manufacturing expenses. Raw material price volatility further compounds these costs, influenced by climatic changes, geopolitical instability, supply chain disruptions, and varying agricultural yields. For example, droughts in major soybean-producing regions like Brazil or the United States can reduce supply substantially, increasing prices of tocopherol-rich oils. Additionally, China's carbon reduction targets (aiming for carbon neutrality by 2060) have resulted in temporary shutdowns of energy-intensive industries, including chemical and pharmaceutical manufacturing, affecting the supply of intermediates needed for Vitamin E production.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Demand from Pharmaceutical Industry for Vitamin E-Based Medications

- Shift Toward Clean Label Products Accelerates Demand for Natural-Sourced Vitamin E

- Stringent Regulatory Norms slow down Global Product Approvals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Natural vitamin E holds 58.23% of the market share in 2024, as consumers increasingly choose bioavailable d-alpha tocopherol over synthetic alternatives. The natural segment is projected to grow at 6.12% CAGR during 2025-2030, supported by clean label trends and regulatory support for natural ingredients. The higher tissue retention and bioactivity of natural vitamin E support its premium pricing, especially in dietary supplements and cosmetics, where efficacy influences purchasing decisions. While synthetic vitamin E retains cost advantages in feed applications, it faces challenges from sustainability requirements and increased consumer awareness about bioavailability differences.

Natural vitamin E manufacturers are strengthening supply chain transparency and implementing sustainable sourcing practices to serve premium market segments. The development of improved extraction technologies and biofortification methods is increasing natural vitamin E yields from oilseed crops, which may reduce production costs while preserving quality benefits. Synthetic vitamin E manufacturers are implementing process improvements and cost reduction measures, but encounter difficulties in markets where natural origin is a key consumer requirement. This creates distinct market segments for natural and synthetic forms, each with unique growth patterns and profit potential.

The Vitamin E Market is Segmented by Ingredient Type (Natural and Synthetic), by Application (Functional Foods and Beverages, Dietary Supplements, Cosmetics and Personal Care, Infant Nutrition, Animal Feed, and Others), by Form (Oil, Powder, and Others), and by Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific holds 41.83% of the global vitamin E market in 2024, primarily due to its position as the world's largest palm oil producer and manufacturing hub for natural and synthetic vitamin E. The region's advantages in raw material access and production capacity strengthen its position in both domestic and export markets. China's 14th Five-Year Plan (2021-2025) promotes national nutrition and functional food industries, supporting vitamin E supplementation to address aging-related diseases and oxidative stress. Indonesia's palm oil supply chain developments, including corporate farming models for smallholder integration, improve the sustainability of natural vitamin E feedstock supply. The region maintains manufacturing capabilities across the value chain, from raw material processing to finished product formulation.

Europe exhibits the highest growth rate at 7.87% CAGR during 2025-2030, supported by strict regulations that favor natural ingredients and premium products. The region's clean label requirements and sustainability standards create opportunities for vitamin E suppliers who meet traceability and environmental criteria. BASF's production facilities in Germany and Denmark support the region's premium markets, while their transition to 100% renewable electricity demonstrates environmental commitment. The European market's preference for natural and sustainable ingredients enables suppliers to maintain higher margins despite increased regulatory compliance costs.

North America maintains a significant market position through established dietary supplement and functional food distribution channels. The Food and Drug Administration (FDA)'s regulatory framework for dietary supplements and food fortification provides market stability while enabling product differentiation through health claims. The region's informed consumer base creates demand for premium formulations and innovative delivery systems, expanding vitamin E applications beyond basic commodities.

- BASF SE

- DSM-Firmenich NV

- Archer-Daniels-Midland Company

- Wilmar International Limited

- Merck KGaA

- Nagase Group

- Jilin Beisha Pharmaceutical Co., Ltd.

- Btsa Biotecnologias Aplicadas SL

- Aryan Food Ingredients

- Orah Nutrichem Pvt. Ltd.

- Matrix Life Science Private Limited

- KLK Oleo

- Matrix Fine Sciences

- Shandong Luwei Pharmacy Limited Company

- Botanic Healthcare Pvt. Ltd.

- Riken Vitamin Co., Ltd.

- Vance Group Ltd.

- ExcelVite Sdn. Bhd.

- Zhejiang Medicine Co., Ltd.

- Fenchem Biotek

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing aging population driving demand for dietary supplements

- 4.2.2 Increasing consumer awareness about preventive healthcare and nutritional supplements

- 4.2.3 Expanding demand from pharmaceutical industry for vitamin E-based medications

- 4.2.4 Widening use of vitamin E in animal feed for livestock health and productivity

- 4.2.5 Shift Toward Clean Label Products Accelerates Demand for Natural-Sourced Vitamin E

- 4.2.6 Surging private label manufacturing boosts ingredient-level demand

- 4.3 Market Restraints

- 4.3.1 High production costs and raw material price volatility affect market profitability

- 4.3.2 Stringent regulatory norms slow down global product approvals

- 4.3.3 High Quality and Certification Standards Limit Market Access for Small and New Entrants

- 4.3.4 Limited availability of raw materials

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE, USD)

- 5.1 By Ingredient Type

- 5.1.1 Natural

- 5.1.2 Synthetic

- 5.2 By Application

- 5.2.1 Functional Foods and Beverages

- 5.2.2 Dietary Supplements

- 5.2.3 Cosmetics and Personal Care

- 5.2.4 Infant Nutrition

- 5.2.5 Animal Feed

- 5.2.6 Others

- 5.3 By Form

- 5.3.1 Oil

- 5.3.2 Powder

- 5.3.3 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 BASF SE

- 6.4.2 DSM-Firmenich NV

- 6.4.3 Archer-Daniels-Midland Company

- 6.4.4 Wilmar International Limited

- 6.4.5 Merck KGaA

- 6.4.6 Nagase Group

- 6.4.7 Jilin Beisha Pharmaceutical Co., Ltd.

- 6.4.8 Btsa Biotecnologias Aplicadas SL

- 6.4.9 Aryan Food Ingredients

- 6.4.10 Orah Nutrichem Pvt. Ltd.

- 6.4.11 Matrix Life Science Private Limited

- 6.4.12 KLK Oleo

- 6.4.13 Matrix Fine Sciences

- 6.4.14 Shandong Luwei Pharmacy Limited Company

- 6.4.15 Botanic Healthcare Pvt. Ltd.

- 6.4.16 Riken Vitamin Co., Ltd.

- 6.4.17 Vance Group Ltd.

- 6.4.18 ExcelVite Sdn. Bhd.

- 6.4.19 Zhejiang Medicine Co., Ltd.

- 6.4.20 Fenchem Biotek

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK