PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044165

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044165

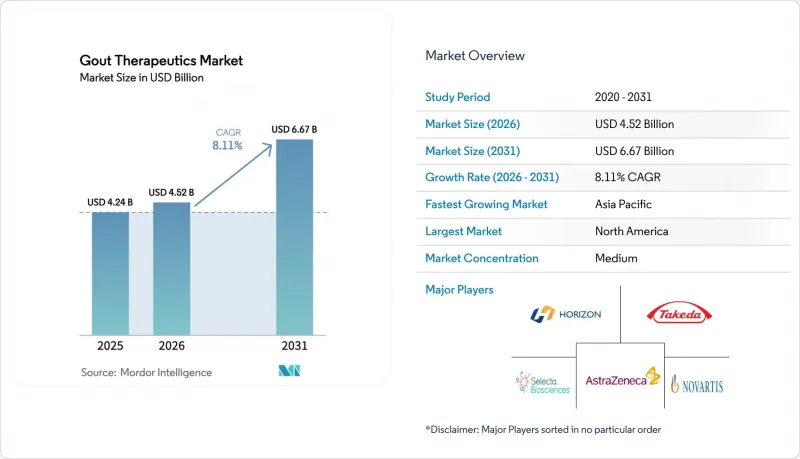

Gout Therapeutics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Gout Therapeutics Market size is projected to be USD 4.24 billion in 2025, USD 4.52 billion in 2026, and reach USD 6.67 billion by 2031, growing at a CAGR of 8.11% from 2026 to 2031.

Demand is being driven by an aging population, increasing cases of obesity-related hyperuricemia, and updated clinical guidelines that emphasize treat-to-target serum urate thresholds. The introduction of biologics for treatment-refractory conditions is expanding therapeutic options for physicians while enabling premium pricing opportunities. At the same time, fixed-dose oral combinations are positioned to protect market share as generic price erosion pressures margins. Digital monitoring tools, integrating smartphone urate meters with algorithm-based flare prediction, are accelerating diagnostics and aligning with payer strategies to reduce costly emergency department visits. However, growth prospects are tempered by cardiovascular safety warnings linked to febuxostat, payer-imposed prior-authorization requirements for pegloticase, and increasing generic competition within the xanthine oxidase inhibitor class.

Global Gout Therapeutics Market Trends and Insights

Rising Disease Prevalence Due to Aging and Obesity

By 2025, the global prevalence of gout reached 41 million cases, with high-income economies experiencing the fastest growth due to obesity rates exceeding 30%. Hyperinsulinemia reduces renal urate clearance, while fructose metabolism accelerates purine catabolism, collectively driving higher serum urate levels. In China, shifting urban dietary preferences toward red meat and sugary beverages led to a twofold increase in gout diagnoses between 2015 and 2024. The demographic profile of gout patients has also evolved, with cases now commonly emerging in individuals in their thirties and forties, rather than in men in their sixties as in historical trends. This demographic shift is expanding the treated population annually and extending the duration of therapeutic interventions. In Japan, 2025 health statistics rank gout among the top ten chronic outpatient conditions for men over 50, equating its prevalence with that of hypertension and diabetes.

Adoption of Evidence-Based Urate-Lowering Treatment Guidelines

The American College of Rheumatology's 2024 update establishes serum urate targets of <6 mg/dL for all gout patients and <5 mg/dL for those with tophi. Similarly, European guidelines emphasize the early initiation of xanthine oxidase inhibitors within weeks of diagnosis, replacing prior wait-and-see approaches. A 2025 Medicare claims analysis highlights a significant improvement: 68% of newly diagnosed U.S. patients initiated urate-lowering therapy within 90 days, compared to 42% in 2019. Fixed-dose oral combinations, designed to align with guideline-recommended dual therapy, are progressing through late-stage pipelines, although regulatory bodies require evidence of superiority over titrated monotherapy. In Germany and the United Kingdom, reimbursement frameworks now link rheumatologist incentives to the electronic documentation of serum-urate targets, driving the adoption of point-of-care testing devices.

Safety Concerns with Existing and Emerging Therapies

Febuxostat carries a boxed cardiovascular warning after the CARES trial showed a 34% rise in cardiac death versus allopurinol. The EMA's 2024 label update restricts use to second-line therapy, redirecting EU prescriptions toward allopurinol. Pegloticase requires infusion-center monitoring because of anaphylaxis, adding USD 1,500-2,000 in facility fees per dose. Colchicine overdoses in renally impaired patients prompted a 2025 FDA safety alert, spotlighting its narrow therapeutic index. These signals lengthen payer approval cycles, with prior-authorization delays averaging 12 days and contributing to patient attrition before therapy begins.

Other drivers and restraints analyzed in the detailed report include:

- Introduction of Novel Mechanisms of Action

- Expansion of Digital Health and Tele-Rheumatology Channels

- Suboptimal Patient Adherence to Long-Term Gout Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Xanthine oxidase inhibitors, dominated by the widespread use of allopurinol and selective utilization of febuxostat in cases with manageable cardiovascular risks, captured 46.34% of the gout therapeutics market revenue in 2025. Uricosurics are projected to grow at a strong 9.54% CAGR, driven by the increasing adoption of combination treatment protocols and the anticipated launch of next-generation URAT1 antagonists with improved renal safety profiles. Although recombinant uricase accounted for less than 5% of the market size in 2025, it delivered significant value, supported by Krystexxa's premium pricing of approximately USD 18,000 per month. Furthermore, IL-1 targeted agents, such as canakinumab, are addressing the flare-prophylaxis segment for patients intolerant to NSAIDs and colchicine, thereby expanding treatment options without directly reducing urate levels.

Pricing pressures are reshaping the oral therapeutics segment, with colchicine's generic price dropping below USD 0.50 per tablet in most markets. NSAIDs and corticosteroids contribute limited long-term value as clinical guidelines increasingly discourage their chronic use. Meanwhile, microbiome-based enzymes that metabolize dietary purines are emerging as potential oral alternatives to biologics, contingent on successful phase-I safety outcomes. However, the lack of FDA guidance on regulatory endpoints for microbiome therapeutics presents a significant challenge for sponsors. With additional febuxostat generics entering global markets, the impending patent cliffs highlight the critical need for innovation beyond traditional xanthine oxidase inhibition strategies.

The Gout Therapeutics Market Report is Segmented by Drug Class (Xanthine Oxidase Inhibitors, and More), Route of Administration (Oral and Injectable), Disease Type (Acute Gout, Chronic Refractory Gout, and Tophaceous Gout), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 42.43% of 2025 global gout therapeutics market value. High obesity prevalence above 40% in several U.S. states and Medicare Part B coverage for infused biologics sustain premium demand. Private payers are expanding site-of-care options, contracting with ambulatory-infusion centers to trim hospital overhead. Canada's publicly funded systems list generics readily, but biologic uptake lags outside private plans, creating disparate patient access. Mexico remains price-sensitive; generic allopurinol dominates, with biologics confined to metropolitan specialty hospitals.

Asia-Pacific is forecast to lead growth at an 8.43% CAGR through 2031. China's gout population exceeded 17 million in 2025, clustered along affluent coastal provinces where seafood and alcohol intake are highest. Japan benefits from universal insurance and early adoption of treat-to-target practice, supporting steady febuxostat sales despite global safety concerns. India's diagnosis gap persists; rheumatologist density is under 0.1 per 100,000 inhabitants, and branded biologics often exceed monthly household income. However, tele-rheumatology pilots in urban centers are beginning to chip away at unmet need.

Europe's reimbursement gatekeepers, including NICE and Germany's G-BA, subject biologics to stringent cost-effectiveness tests. Pegloticase access is restricted to oral-therapy failures, capping volume. Southern European markets favor low-cost colchicine, while France's community pharmacies report brisk generic febuxostat turnover following 2024 patent expiry. Eastern Europe shows nascent demand, handicapped by limited specialist access and share-of-wallet constraints. The Middle East and Africa contribute modest revenue; Gulf states mirror Western therapy patterns among expatriate populations, whereas sub-Saharan markets remain early in epidemiologic transition. South America centers on Brazil and Argentina, where public formularies reimburse generics, and patient-assistance programs bridge affordability gaps for biologics.

- Arthrosi Therapeutics

- AstraZeneca (Ardea Biosciences)

- Atom Bioscience

- Boehringer Ingelheim

- Hanmi Pharmaceutical

- Horizon Biosciences (Verinurad)

- Horizon Therapeutics (Amgen)

- JW Pharmaceutical

- Mitsubishi Tanabe Pharma

- Novartis

- Pfizer

- Protalix BioTherapeutics

- Regeneron Pharmaceuticals

- Sanofi

- Selecta Biosciences

- Sobi

- Takeda Pharmaceutical Co.

- Teijin Pharma

- UCB

- XORTX Therapeutics

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Disease Prevalence Due to Aging and Obesity

- 4.2.2 Adoption of Evidence-Based Urate-Lowering Treatment Guidelines

- 4.2.3 Introduction of Novel Mechanisms of Action

- 4.2.4 Expansion of Digital Health and Tele-Rheumatology Channels

- 4.2.5 Advances in Personalized Medicine and Biomarker Monitoring

- 4.2.6 Emergence of Microbiome-Based Therapeutics and Enzyme Therapies

- 4.3 Market Restraints

- 4.3.1 Safety Concerns with Existing and Emerging Therapies

- 4.3.2 Suboptimal Patient Adherence to Long-Term Gout Management

- 4.3.3 Generic Competition and Price Erosion Reducing Profitability

- 4.3.4 Regulatory Actions Limiting Promotion of High-Purine Diets and Alcohol

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat Of New Entrants

- 4.7.2 Bargaining Power Of Suppliers

- 4.7.3 Bargaining Power Of Buyers

- 4.7.4 Threat Of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Drug Class

- 5.1.1 Xanthine Oxidase Inhibitors

- 5.1.2 Uricosurics

- 5.1.3 Recombinant Uricase

- 5.1.4 IL-1 Inhibitors

- 5.1.5 Colchicine

- 5.1.6 NSAIDs

- 5.1.7 Corticosteroids

- 5.1.8 Other Classes

- 5.2 By Route Of Administration

- 5.2.1 Oral

- 5.2.2 Injectable

- 5.3 By Disease Type

- 5.3.1 Acute Gout

- 5.3.2 Chronic Refractory Gout

- 5.3.3 Tophaceous Gout

- 5.4 Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 India

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 Middle East & Africa

- 5.4.4.1 GCC

- 5.4.4.2 South Africa

- 5.4.4.3 Rest of Middle East & Africa

- 5.4.5 South America

- 5.4.5.1 Brazil

- 5.4.5.2 Argentina

- 5.4.5.3 Rest of South America

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles {(Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)}

- 6.3.1 Arthrosi Therapeutics

- 6.3.2 AstraZeneca (Ardea Biosciences)

- 6.3.3 Atom Bioscience

- 6.3.4 Boehringer Ingelheim

- 6.3.5 Hanmi Pharmaceutical

- 6.3.6 Horizon Biosciences (Verinurad)

- 6.3.7 Horizon Therapeutics (Amgen)

- 6.3.8 JW Pharmaceutical

- 6.3.9 Mitsubishi Tanabe Pharma

- 6.3.10 Novartis AG

- 6.3.11 Pfizer Inc.

- 6.3.12 Protalix BioTherapeutics

- 6.3.13 Regeneron Pharmaceuticals

- 6.3.14 Sanofi

- 6.3.15 Selecta Biosciences

- 6.3.16 Sobi

- 6.3.17 Takeda Pharmaceutical Co.

- 6.3.18 Teijin Pharma

- 6.3.19 UCB Pharma

- 6.3.20 XORTX Therapeutics

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment