PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842527

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1842527

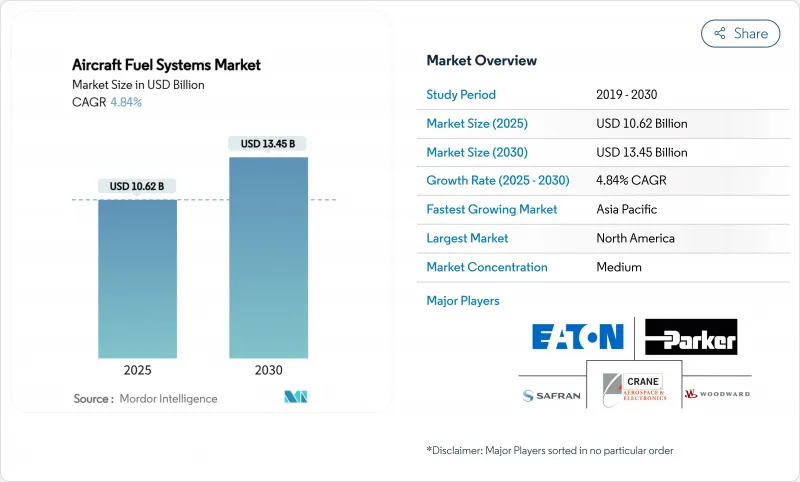

Aircraft Fuel Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The aircraft fuel systems market size stands at USD 10.62 billion in 2025 and is forecasted to reach USD 13.45 billion by 2030, translating into a steady 4.84% CAGR.

Heightened aircraft production schedules, autonomy-driven refueling programs, and digital retrofits reinforce demand even as raw-material shortages challenge supply continuity. Airbus alone handed over 51 aircraft in May 2025, led by the A321neo and A321XLR, underscoring a rebound in single-aisle deliveries that depend on advanced fuel-saving architectures. Parallel momentum stems from a USD 898 million US Navy order covering three MQ-25 Stingray unmanned tankers, inauguring autonomous aerial refueling at sea. North American incumbents such as Parker Hannifin recorded 12% aerospace revenue growth to USD 1.6 billion in Q3 2025, signalling healthy aftermarket pull-through. Asia-Pacific provides the fastest regional lift, posting a 5.78% CAGR on the back of airport infrastructure expansion and rising defence budgets. Regulatory insistence on nitrogen-inerting and shifting toward sustainable aviation fuels (SAF) further stimulates technology upgrades, offsetting certification cost pressures and titanium supply disruptions that persist across civil and military value chains.

Global Aircraft Fuel Systems Market Trends and Insights

Surging Global Commercial Aircraft Deliveries

Airframers are elevating output to meet airline refurbishment cycles. Airbus aims for 820 deliveries in 2025 and prioritizes long-range single-aisle models that utilise multiple centre- and auxiliary-tank arrangements to achieve up to 4,700 NM range. Boeing's concurrent production of F-15EX fighters sustains fuel pump and valve demand for combat platforms. Component suppliers, therefore, face enlarged call-offs for precision pumps, probes, and transfer valves while MRO providers register faster consumable replacement cycles as utilization returns to pre-pandemic flight hours.

Expansion of Military Aerial-Refueling Programs

The MQ-25 Stingray marks the first carrier-based unmanned tanker capable of transferring 15,000 lb of fuel beyond 500 NM, pushing requirements for fault-tolerant flow metering and autonomous shut-off logic. The USAF's KC-46A Pegasus expansion and allied European acquisitions reinforce multi-point refuelling demand, each necessitating high-capacity boost pumps and actively damped boom-actuation manifolds.

High Certification and Qualification Costs for New Fuel Technologies

Novel hydrogen or SAF-ready fuel systems routinely require multi-year test campaigns and FAA certification plans. The agency's December 2024 Hydrogen Roadmap highlights data gaps that could cost manufacturers tens of millions in qualification expenditure. Small suppliers face disproportionate burdens that slow market entry and limit price competition.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Fleet Modernization Toward Fuel-Efficient Platforms

- Predictive Analytics Integration for Real-Time Fuel-System Health

- Aviation-Grade Titanium and Elastomer Supply Bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Gravity-feed architectures retained 45.76% of the aircraft fuel systems market share in 2024, underscoring their cost-effective appeal for general aviation and selected military fleets. Within the same period, the aircraft fuel systems market size for fuel-injection platforms advanced at a 6.34% CAGR, the fastest among all types, as operators embraced FADEC-compatible hardware that can trim fuel burn by about 15% through real-time mixture optimization. Pump-feed solutions continued to serve the performance middle ground, supporting airframes that require positive pressure delivery without the full digital overlay.

Suppliers are embedding machine-learning logic into next-gen injectors to predict flow requirements and balance tanks autonomously, turning the fuel circuit into a sensor-rich data source. Safran's FADEC 4 illustrates the leap, delivering 10 times greater processing power than earlier units while elevating overall efficiency. As IoT connectivity spreads across flight decks, traditional gravity systems face competitive pressure from injection assemblies that promise tighter consumption control, predictive health monitoring, and lower lifecycle cost, accelerating the technology shift within the broader aircraft fuel systems market.

Fuel tanks held the largest 36.58% revenue share in 2024. Nonetheless, inerting assemblies-spanning nitrogen generators, membranes, and distribution plumbing-advanced at a 5.78% CAGR on the back of mandatory retrofit programs. The aircraft fuel systems market size for inerting solutions stood near USD 1.8 billion in 2025 and is on track to exceed USD 2.4 billion by decade-end. Operators accept higher capital costs in exchange for flammability-exposure compliance and insurance benefits.

Variable-speed electric pumps and smart motor-operated valves augment safety by harmonising tank pressures during inert gas injection. Coupled with embedded oxygen sensors, these systems notify crews or maintenance teams when purity drifts outside thresholds, reinforcing the aircraft fuel systems market's emphasis on real-time data visibility.

The Aircraft Fuel Systems Market Report is Segmented by Type (Gravity Feed, Pump Feed, and Fuel Injection Systems), Component (Fuel Tanks, Fuel Pumps, and More), Aircraft Class (Commercial Aircraft, Military Aircraft, and More), End Use (OEM and Aftermarket), Technology (Conventional Mechanical Systems, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's aviation services outlay will rise from USD 52 billion in 2025 to USD 129 billion in 2043, implying compound 4.81% growth and a proportional uptick in fuel system spares. Maintenance spend alone accelerates at 5.0% yearly, creating space for predictive analytics licensors and specialty seal manufacturers. China's civil expansion partners with indigenous wide-body programs, pushing the localization of titanium tank fittings. India's SAF push underlines the need for dual-fuel-compatible seals by 2030, while Singapore's early 1% SAF blending rule from 2026 makes it a live testbed for filter adaptability.

North America's 42.35% market share derives from entrenched OEM and MRO ecosystems across Kansas, Washington, and Georgia. The USAF continues to order the F-15EX and KC-46A, locking in steady valve, pump, and hose procurements through 2030. FAA flammability mandates further generate retrofit workscopes for nitrogen generation and monitoring lines.

Europe maintains primacy in environmental regulation. The ReFuelEU Aviation Act begins with 2% SAF by 2025 and scales to 70% by 2050, compelling filter-housing redesigns for bio-derived fuels with higher solvency. Airbus' partnership with TotalEnergies targets 1.5 million t annual SAF output by 2030, underpinning nozzle, gasket, and seal demand that can withstand novel fuel chemistries.

- Eaton Corporation plc

- Parker-Hannifin Corporation

- Safran SA

- Crane Aerospace & Electronics (Crane Company)

- Woodward, Inc.

- RTX Corporation

- GKN Aerospace Services Limited (Melrose plc)

- Triumph Group Inc.

- SECONDO MONA S.p.A.

- Honeywell International Inc.

- Robertson Fuel Systems, LLC (HEICO Corporation)

- Marshall of Cambridge (Holdings) Ltd

- Weldon Pump. LLC.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging global commercial aircraft deliveries

- 4.2.2 Expansion of military aerial-refueling programs

- 4.2.3 Rapid fleet modernization toward fuel-efficient platforms

- 4.2.4 Rising UAV procurement across civil and defense sectors

- 4.2.5 Predictive analytics integration for real-time fuel-system health

- 4.2.6 Mandatory retrofit of nitrogen-inerting systems for safety

- 4.3 Market Restraints

- 4.3.1 High certification and qualification costs for new fuel technologies

- 4.3.2 Aviation-grade titanium and elastomer supply bottlenecks

- 4.3.3 Fuel-price volatility curbing airline capital expenditure

- 4.3.4 Cyber-security risks in digital gauging and control networks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Gravity Feed

- 5.1.2 Pump Feed

- 5.1.3 Fuel Injection Systems

- 5.2 By Component

- 5.2.1 Fuel Tanks

- 5.2.2 Fuel Pumps

- 5.2.3 Valves and Manifolds

- 5.2.4 Gauges and Sensors

- 5.2.5 Inerting Systems

- 5.2.6 Fuel Filters

- 5.3 By Aircraft Class

- 5.3.1 Commercial Aircraft

- 5.3.1.1 Narrowbody Aircraft

- 5.3.1.2 Widebody Aircraft

- 5.3.1.3 Regional Aircraft

- 5.3.2 Military Aircraft

- 5.3.2.1 Combat Aircraft

- 5.3.2.2 Non-Combat Aircraft

- 5.3.2.3 Helicopters

- 5.3.3 General Aviation Aircraft

- 5.3.3.1 Business Jets

- 5.3.3.2 Turboprop Aircraft

- 5.3.3.3 Piston Aircraft

- 5.3.3.4 Helicopters

- 5.3.4 Unmanned Aerial Vehicles (UAVs)

- 5.3.1 Commercial Aircraft

- 5.4 By End Use

- 5.4.1 OEM

- 5.4.2 Aftermarket

- 5.5 By Technology

- 5.5.1 Conventional Mechanical Systems

- 5.5.2 FADEC-Integrated Electric Systems

- 5.5.3 Inerting-Enabled Systems

- 5.5.4 Smart/Connected Fuel Systems

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Russia

- 5.6.2.5 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 United Arab Emirates

- 5.6.5.1.2 Saudi Arabia

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 Egypt

- 5.6.5.2.2 South Africa

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Eaton Corporation plc

- 6.4.2 Parker-Hannifin Corporation

- 6.4.3 Safran SA

- 6.4.4 Crane Aerospace & Electronics (Crane Company)

- 6.4.5 Woodward, Inc.

- 6.4.6 RTX Corporation

- 6.4.7 GKN Aerospace Services Limited (Melrose plc)

- 6.4.8 Triumph Group Inc.

- 6.4.9 SECONDO MONA S.p.A.

- 6.4.10 Honeywell International Inc.

- 6.4.11 Robertson Fuel Systems, LLC (HEICO Corporation)

- 6.4.12 Marshall of Cambridge (Holdings) Ltd

- 6.4.13 Weldon Pump. LLC.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment