PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844444

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844444

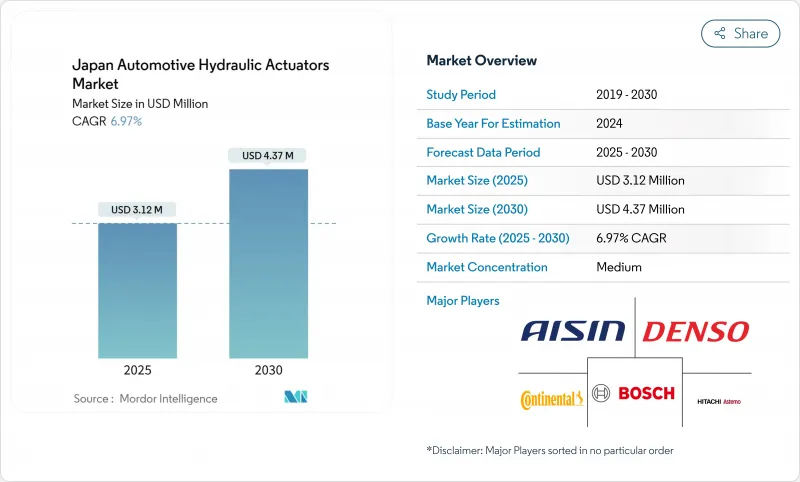

Japan Automotive Hydraulic Actuators - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Japan automotive hydraulic actuators market size was valued at USD 3.12 million in 2025 and is forecast to reach USD 4.37 million by 2030, expanding at a 6.97% CAGR.

Persistent demand for redundant brake circuitry outlined in the latest JIS D 0801 and UN R13-H rules sustains growth even as electrification advances. Government-backed hydrogen truck subsidies, rapid ADAS uptake, and predictive-maintenance adoption further bolster the Japan automotive hydraulic actuators market, while new 25% tariffs on parts imported into the United States and rising labor costs weigh on volumes. OEMs continue to favor hydraulic solutions in safety-critical functions because they deliver proven reliability under harsh duty cycles, especially in medium and heavy commercial vehicles that now qualify for sizable hydrogen incentives.

Japan Automotive Hydraulic Actuators Market Trends and Insights

Rising ADAS Penetration Calls for High-Response Hydraulic Brake Actuators

Automatic emergency braking is now mandatory across vehicle categories, creating a need for hydraulic brake actuators that achieve sub-50-ms response times. Hybrid brake-by-wire architectures keep hydraulic redundancy while enabling electronic precision, pushing suppliers to redesign units for seamless ECU integration. Forward-collision warning adoption reached 94% by model year 2023, and component makers that meet the tighter performance window command premium pricing. Bosch's recent brake-by-wire rollouts illustrate how electronic control overlays still rely on hydraulic backup for fail-safe assurance .

Stricter JIS D 0801 / UN R13-H Safety Rules Raise Hydraulic Redundancy Needs

New braking rules require multi-circuit hydraulic systems able to retain residual pressure even under single-circuit failure. Compliance efforts spur uptake of tandem master cylinders, dual-pump boosters, and integrated pressure sensors. Component certification now involves tighter audit trails after widely publicized type-approval misconduct cases, giving incumbents with robust quality systems a competitive edge .

EV Shift Toward Electro-Mechanical Actuators Erodes Hydraulic Content

Battery-electric platforms increasingly specify electromechanical brakes and suspension, reducing hydraulic fitment. ZF won a 5 million-vehicle contract for full brake-by-wire systems that eliminate hydraulic lines entirely. Subsidies that favor BEVs and fuel-cell cars intensify the pivot, pushing incumbent hydraulic suppliers to diversify into electronic actuation.

Other drivers and restraints analyzed in the detailed report include:

- Passenger-Car Production Rebound Boosts OEM Demand

- Ageing Fleet Lengthens Replacement Cycles, Expanding Aftermarket Volumes

- Domestic Vehicle Production Decline Limits Volume Growth Potential

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars retained a 68.55% share of the Japan automotive hydraulic actuators market in 2024, reflecting entrenched personal-mobility demand. Yet medium and heavy commercial vehicles will record the highest 8.16% CAGR to 2030, buoyed by hydrogen-truck incentives that specify advanced hydraulic units with corrosion-resistant seals. This shift marginally dilutes passenger-car share over the forecast window but enlarges total output value because commercial vehicles carry higher actuator content per unit. Light commercial vans continue to see steady adoption as last-mile delivery expands.

The Japan automotive hydraulic actuators market gains strategic depth from commercial-vehicle requirements for long-life, serviceable designs that withstand high duty cycles. Fleet operators prioritize actuators with integrated condition monitoring to minimize downtime, propelling demand for sensorized units. Passenger cars, though slower growing, remain vital for volume stability and serve as a testbed for hybrid hydraulic-electronic systems that later migrate to heavier platforms.

Brake actuators commanded 45.18% of the Japan automotive hydraulic actuators market size in 2024, sustained by safety regulations and near-universal fitment. However, fuel-injection actuators will be the fastest 7.34% CAGR through 2030 as OEMs refine combustion efficiency ahead of stricter emission caps. Embedded pressure and temperature sensors inside the injector actuator assembly enable predictive maintenance, reducing unplanned engine downtime.

HVAC blend-door and seat-adjustment systems add incremental volume, but their share trails powertrain and safety applications. Predictive maintenance also uplifts brake-actuator replacements because diagnostic data now pinpoints declining pressure build-up before pedal feel deteriorates, strengthening aftermarket sales.

The Japan Automotive Hydraulic Actuators Market Report is Segmented by Vehicle Type (Passenger Car, Light Commercial Vehicle, Medium and Heavy Commercial Vehicle, and More), Application Type (Brake Actuator, Throttle Actuator, and More), Actuator Design (Linear Hydraulic Actuators and Rotary Hydraulic Actuators), and Sales Channel (OEM and Aftermarket). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

List of Companies Covered in this Report:

- Denso Corporation

- Aisin Corporation

- Hitachi Astemo Ltd.

- Mitsubishi Electric Corporation

- KYB Corporation

- Akebono Brake Industry Co., Ltd.

- Robert Bosch GmbH

- Continental AG

- BorgWarner Inc.

- Nabtesco Corporation

- NSK Ltd.

- JTEKT Corporation

- Nissin Kogyo Co., Ltd.

- Parker Hannifin K.K.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising ADAS penetration calls for high-response hydraulic brake actuators

- 4.2.2 Stricter JIS D 0801 / UN R13-H safety rules raise hydraulic redundancy needs

- 4.2.3 Passenger-car production rebound post-pandemic boosts OEM demand

- 4.2.4 Ageing fleet lengthens replacement cycles, expanding aftermarket volumes

- 4.2.5 Smart-sensor-integrated actuators enable predictive-maintenance adoption

- 4.2.6 Hydrogen-truck subsidies accelerate demand for specialty hydraulic units

- 4.3 Market Restraints

- 4.3.1 EV shift toward electro-mechanical actuators erodes hydraulic content

- 4.3.2 Domestic vehicle production decline limits volume growth potential

- 4.3.3 Skilled-machinist shortage inflates precision hydraulic manufacturing costs

- 4.3.4 Oil-leak environmental penalties raise compliance cost pressures

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers/Consumers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Car

- 5.1.2 Light Commercial Vehicle

- 5.1.3 Medium and Heavy Commercial Vehicle

- 5.1.4 Buses and Coaches

- 5.2 By Application Type

- 5.2.1 Brake Actuator

- 5.2.2 Throttle Actuator

- 5.2.3 Seat Adjustment Actuator

- 5.2.4 Closure Actuator

- 5.2.5 Fuel-Injection Actuator

- 5.2.6 HVAC Blend-Door Actuator

- 5.2.7 Others

- 5.3 By Actuator Design

- 5.3.1 Linear Hydraulic Actuators

- 5.3.2 Rotary Hydraulic Actuators

- 5.4 By Sales Channel

- 5.4.1 OEM

- 5.4.2 Aftermarket

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Denso Corporation

- 6.4.2 Aisin Corporation

- 6.4.3 Hitachi Astemo Ltd.

- 6.4.4 Mitsubishi Electric Corporation

- 6.4.5 KYB Corporation

- 6.4.6 Akebono Brake Industry Co., Ltd.

- 6.4.7 Robert Bosch GmbH

- 6.4.8 Continental AG

- 6.4.9 BorgWarner Inc.

- 6.4.10 Nabtesco Corporation

- 6.4.11 NSK Ltd.

- 6.4.12 JTEKT Corporation

- 6.4.13 Nissin Kogyo Co., Ltd.

- 6.4.14 Parker Hannifin K.K.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment