PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844448

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844448

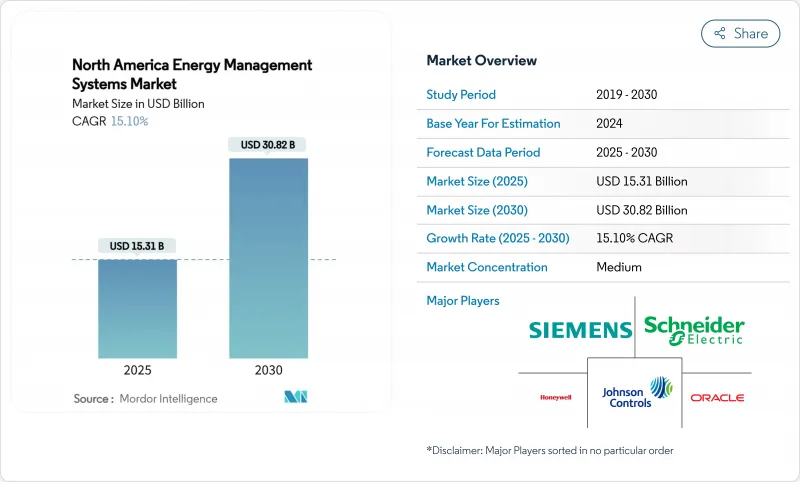

North America Energy Management Systems - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The North America energy management systems market size stood at USD 15.31 billion in 2025 and is projected to reach USD 30.82 billion by 2030, registering a firm 15.10% CAGR.

The doubling of value in just five years underlines the region's swift shift toward intelligent, software-defined infrastructure that cuts emissions and optimizes power use. Federal incentives, corporate net-zero mandates, and rapid advances in AI-enabled optimization tools are the primary forces behind this rise. US dominance, the cloud pivot, and wireless connectivity all accelerate adoption by shrinking payback periods. At the same time, mid-sized enterprises and public institutions unlock fresh savings through performance-based contracts that transfer risk to service providers. Rising data-center loads, strengthened building codes, and dynamic utility tariffs further widen the addressable pool for the North America energy management systems market.

North America Energy Management Systems Market Trends and Insights

US Inflation Reduction Act Retrofit Incentives

Generous tax credits and rebates under the USD 370 billion Inflation Reduction Act cut retrofit payback periods and spur immediate procurement of networked controls and analytics platforms. Commercial buildings can now deduct up to USD 5.00 per square foot of qualifying upgrades, while states such as California have secured USD 291 million to deliver whole-home rebates that target 20-35% savings. Domestic production credits encourage local EMS hardware output and cushion supply chains. As evidence, Johnson Controls reports USD 8.4 billion in customer savings created by performance contracts that ride on federal and state incentive stacks.

Smart-Grid Roll-outs and AMI Penetration

Utilities invested USD 320 billion in grid upgrades during 2023, including USD 50.9 billion for distribution assets that host advanced metering infrastructure. AMI data feeds granular load curves into AI engines embedded in modern platforms and enables virtual power plant (VPP) participation. The US Department of Energy projects 80-160 GW of VPP capacity by 2030. Edge analytics shrinks response times by up to 92%, letting buildings monetize flexibility while preserving occupant comfort. Mexico's USD 23 billion grid program adds cross-border demand for compatible solutions.

High Upfront and O&M Costs

Turnkey systems for mid-sized offices can surpass USD 50,000 before maintenance fees, and life-cycle costs often climb to five times the initial outlay. Residential buyers feel the pinch even more sharply when local incentives are limited. Energy-as-a-service contracts mitigate risk: Cobb County's USD 7.1 million deal guarantees USD 2 million utility savings over 20 years. Still, semiconductor shortages and the capital demands of cleaner chip fabrication inflate hardware prices in the near term.

Other drivers and restraints analyzed in the detailed report include:

- Corporate VPP and Net-Zero Procurement Strategies

- Dynamic Real-Time Utility Tariffs

- Data-Security and Privacy Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Building Energy Management Systems retained a commanding 62% share of the North America energy management systems market in 2024, anchored by large commercial portfolios that prize operational transparency and tenant comfort. Yet Home Energy Management Systems are scaling swiftly on the back of smart-speaker ubiquity, utility rebates, and maturing interoperability standards. The segment's 17.23% CAGR through 2030 makes it the most disruptive pocket of the North America energy management systems market.

Annual data show HEMS installations reducing household consumption by more than 20% once machine-learning algorithms adjust HVAC and appliance schedules. Matter protocol adoption simplifies device pairing and propels mainstream appeal. Industrial EMS offerings occupy a middle niche, providing process-specific analytics and compliance dashboards for heavy manufacturing clients. Collectively, these dynamics keep the North America energy management systems market diversified and resilient.

Services captured 43% share in 2024 and delivered the highest 17.02% CAGR to 2030, underscoring a decisive tilt away from one-off hardware deals toward continuous optimization agreements. Recurring revenue streams cover monitoring, analytics, and guaranteed-savings contracts that shift performance risk to providers. Hardware is indispensable but increasingly commoditized, while cloud software layers create value through predictive controls.

Service-led engagements often bundle financing, retro-commissioning, and operator training, forming an integrated pathway to energy-as-a-service delivery. Limbach Holdings uses data-driven reviews to uncover hundreds of actionable insights per site, illustrating how analytics skills eclipse pure equipment know-how. These developments sustain the North America energy management systems market momentum even when capital budgets tighten.

The North America Energy Management Systems Market Report is Segmented by EMS Type (Building Energy Management Systems (BEMS), Home Energy Management Systems (HEMS), and More), Component (Hardware, Software, and Services), Deployment Mode (On-Premise, Cloud-Based, and More), End-User Sector (Commercial, Residential, and More), Communication Technology (Wired and Wireless), and Geography.

List of Companies Covered in this Report:

- Johnson Controls International plc

- Honeywell International Inc.

- Siemens AG

- Schneider Electric SE

- General Electric Company

- Oracle Corporation

- Panasonic Holdings Corporation

- Uplight Inc.

- Enel X North America

- ABB Ltd.

- IBM Corporation

- Eaton Corporation plc

- Rockwell Automation Inc.

- Cisco Systems Inc.

- Honeywell Building Technologies

- Schneider EcoStruxure

- Itron Inc.

- GridPoint Inc.

- Trane Technologies plc

- Schneider EcoStruxure (division)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing electricity prices and sustainability commitments

- 4.2.2 Stringent energy-efficiency regulations and building codes

- 4.2.3 Smart-grid roll-outs and AMI penetration

- 4.2.4 US Inflation Reduction Act retrofit incentives

- 4.2.5 Corporate VPP and net-zero procurement strategies

- 4.2.6 Dynamic real-time utility tariffs

- 4.3 Market Restraints

- 4.3.1 High upfront and OandM costs

- 4.3.2 Data-security and privacy concerns

- 4.3.3 Integrator skill-set shortage

- 4.3.4 Fragmented legacy protocols and interoperability gaps

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By EMS Type

- 5.1.1 Building Energy Management Systems (BEMS)

- 5.1.2 Home Energy Management Systems (HEMS)

- 5.1.3 Industrial Energy Management Systems (IEMS)

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Deployment Mode

- 5.3.1 On-Premise

- 5.3.2 Cloud-based

- 5.3.3 Edge / Hybrid

- 5.4 By End-User Sector

- 5.4.1 Commercial

- 5.4.2 Industrial and Manufacturing

- 5.4.3 Residential

- 5.4.4 Healthcare Facilities

- 5.4.5 Education Campuses

- 5.4.6 Utilities and Energy Providers

- 5.5 By Communication Technology

- 5.5.1 Wired (BACnet, Modbus, etc.)

- 5.5.2 Wireless (Zigbee, Wi-Fi, Bluetooth, Z-Wave)

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Johnson Controls International plc

- 6.4.2 Honeywell International Inc.

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric SE

- 6.4.5 General Electric Company

- 6.4.6 Oracle Corporation

- 6.4.7 Panasonic Holdings Corporation

- 6.4.8 Uplight Inc.

- 6.4.9 Enel X North America

- 6.4.10 ABB Ltd.

- 6.4.11 IBM Corporation

- 6.4.12 Eaton Corporation plc

- 6.4.13 Rockwell Automation Inc.

- 6.4.14 Cisco Systems Inc.

- 6.4.15 Honeywell Building Technologies

- 6.4.16 Schneider EcoStruxure

- 6.4.17 Itron Inc.

- 6.4.18 GridPoint Inc.

- 6.4.19 Trane Technologies plc

- 6.4.20 Schneider EcoStruxure (division)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment