PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844464

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844464

Hypochlorite Bleaches - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

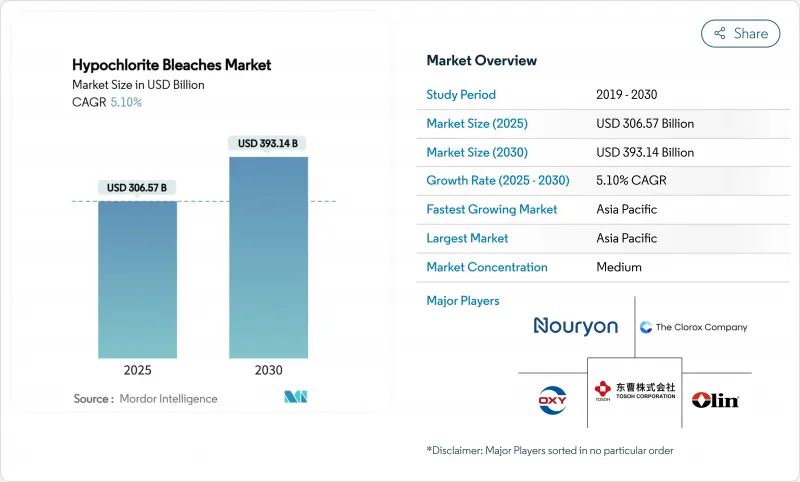

The Hypochlorite Bleaches Market size is estimated at USD 306.57 billion in 2025, and is expected to reach USD 393.14 billion by 2030, at a CAGR of 5.10% during the forecast period (2025-2030), which underscores the sector's capacity to adapt to shifting regulations and technological advances.

Infrastructure spending on municipal water and wastewater systems, particularly in Asia Pacific, is vaulting demand as utilities transition from chlorine gas to safer sodium hypochlorite solutions. Investment in localized production-often upwards of USD 70 million per plant-also strengthens supply-chain resilience, while energy-efficient membrane-cell electrolysis is lowering power use by 15% compared with open-cell units. The Hypochlorite bleaches market further benefits from regulatory clarity: the EPA's 2024 revisions streamline hypochlorite transport, and the European Union has authorized calcium hypochlorite biocidal product families through 2035, both of which favor solution adoption. Competitive pressures persist, however, as peroxide-based alternatives gain popularity in textile and pulp bleaching, and hazardous-materials rules raise handling costs for oxidizers.

Global Hypochlorite Bleaches Market Trends and Insights

Escalating Water-Treatment & Sanitation Spending

Global water-infrastructure outlays are trending toward USD 1 trillion by 2033, advancing at 5.9% and directly lifting the Hypochlorite bleaches market through higher municipal and industrial disinfection needs. India exemplifies this surge, as government programs such as Jal Jeevan Mission push the nation's water-chemicals demand toward USD 2.8 billion by 2025. Remote facilities increasingly favor on-site sodium hypochlorite generation, eliminating chlorine-gas transport; Prague's installation treats 3,000 L s-1 while keeping residual chlorine within 0.2-0.4 ppm, protecting 800,000 residents. Smart dosing controls and AI-enabled telemetry are now common, cementing hypochlorite's role in modern water grids.

Surging Pulp & Paper Output in Emerging Asia

China consumed 13 million t of wood pulp in 2024, over 60% imported, and India may require 9.2 million t by 2030, driving the Hypochlorite bleaches market across Asia's paper mills. Trend analysis shows mills swapping chlorine gas for safer hypochlorite or chlorine-dioxide stages that cut effluent AOX while meeting brightness targets. Pilot studies by RISE reveal that optimized hypochlorite sequences preserve paper strength and curb chemical usage, providing mills with cost and compliance advantages. New capacity across Southeast Asia frequently incorporates membrane-based electrochlorination units, embedding hypochlorite supply within mill utilities.

Rising Shift Toward Peroxide-Based Bleaching Chemistries

Hydrogen peroxide decomposes into water and oxygen, eliminating chlorinated by-products and appealing to mills and dye-houses pursuing eco-labels. Advanced oxidation processes pairing UV/H2O2 or ozone outperform hypochlorite for difficult organics, nudging the Hypochlorite bleaches market toward specialty niches. Premium textile houses in Europe already pay a sustainability premium for peroxide-bleached cotton, exerting market-share pressure on hypochlorite formulations.

Other drivers and restraints analyzed in the detailed report include:

- Capacity Additions in African Textile Finishing

- Roll-out of On-Site Hypochlorite Generators for Remote Utilities

- Strict Transport & Storage Rules for Oxidizing Chemicals

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sodium hypochlorite contributed 58.91% to the Hypochlorite bleaches market in 2024, supported by entrenched use in municipal disinfection and household cleaning. Calcium hypochlorite, however, is forecast to grow 5.73% annually, buoyed by its EU authorization for pool and potable-water treatment through 2035.

Sodium's supremacy rests on liquid supply chains and maturing on-site generation. Membrane-cell systems uplift concentration to 7% w/w with 15% lower electricity bills, enriching the Hypochlorite bleaches market size for plant operators investing in electrochemical upgrades. Conversely, calcium's stability and 65-70% available chlorine endear it to remote installations needing long shelf life. Lithium and potassium salts remain niche, limited by cost and specialized industrial needs.

The Hypochlorite Bleaches Market Report is Segmented by Product (Sodium Hypochlorite, Calcium Hypochlorite, Lithium Hypochlorite, Potassium Hypochlorite), Form (Liquid, Solid), Application (Pulp and Paper, Disinfectants, Textiles, Aquaculture, Laundry Bleach, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific generated 43.26% of Hypochlorite bleaches market revenue in 2024 and will likely rise at 5.67% CAGR to 2030 as governments channel record sums into water networks and as regional pulp mills pivot to safer bleaching routes. China's paper industry alone consumes 13 million t of wood pulp yearly, creating a sizable pull for hypochlorite solutions. India's Jal Jeevan Mission stokes chemical demand while De Nora's 20-unit CECHLO deployment in Hong Kong shows municipal enthusiasm for on-site generation.

North America is a mature yet evolving arena for the Hypochlorite bleaches market. The EPA's 2024 hazmat rules tighten chlorine-gas usage, catalyzing a wave of USD 70 million-plus local bleach plants and buoying revenue at integrated producers; Olin's Chlor Alkali segment topped USD 924.5 million in Q1 2025, up 4.5% year on year. Membrane-cell retrofits bolster energy efficiency, ensuring domestic competitiveness.

Europe faces decarbonization pressure worth an estimated USD 550 billion across the chlor-alkali chain, yet regulatory backing for hypochlorite continues via calcium authorization. Prague's conversion to on-site sodium hypochlorite highlights safety gains, processing 3,000 L s-1 for 800,000 residents. The Middle East and Africa are nascent, but textile-finishing investments and water-scarcity countermeasures suggest above-average growth potential for the Hypochlorite bleaches market.

- Aditya Birla Chemicals

- AGC Chemicals

- Arkema SA

- Chlorum Solutions USA

- Cleanwater1 Inc.

- Clorox Company

- COVENTYA Group

- Ecoviz Kft

- Electrolytic Technologies LLC

- Hangzhou ASIA Chemical Engineering Co., Ltd

- HTH Pools (Arch Chemicals)

- Inovyn

- JSC AVANGARD

- Lanxess AG

- Lonza Group

- Nouryon

- Occidental Chemical (OxyChem)

- Odyssey Manufacturing Co.

- Olin Corporation

- Osaka Soda Co. Ltd.

- Shijiazhuang Xinlongwei Chemical

- Shouguang Tianwei Chemical

- Tianjin Yufeng Chemical

- Tosoh Corporation

- Union Overseas Enterprise Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating water-treatment and sanitation spending

- 4.2.2 Surging pulp and paper output in emerging Asia

- 4.2.3 Capacity additions in African textile finishing

- 4.2.4 Roll-out of on-site hypochlorite generators for remote utilities

- 4.2.5 Chlorine-gas phase-out regulations benefitting hypochlorites

- 4.3 Market Restraints

- 4.3.1 Rising shift toward peroxide-based bleaching chemistries

- 4.3.2 Strict transport and storage rules for oxidising chemicals

- 4.3.3 Growth of advanced oxidative processes (ozone/AOP)

- 4.3.4 Decarbonisation pressure on chlor-alkali value chain

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts(Value)

- 5.1 By Product

- 5.1.1 Sodium Hypochlorite

- 5.1.2 Calcium Hypochlorite

- 5.1.3 Lithium Hypochlorite

- 5.1.4 Potassium Hypochlorite

- 5.2 By Form

- 5.2.1 Liquid

- 5.2.2 Solid (Granular/Tablets/Powder)

- 5.3 By Application

- 5.3.1 Pulp and Paper

- 5.3.2 Disinfectants

- 5.3.3 Textiles

- 5.3.4 Aquaculture

- 5.3.5 Laundry Bleach

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN

- 5.4.1.6 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis (%)/Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Aditya Birla Chemicals

- 6.4.2 AGC Chemicals

- 6.4.3 Arkema SA

- 6.4.4 Chlorum Solutions USA

- 6.4.5 Cleanwater1 Inc.

- 6.4.6 Clorox Company

- 6.4.7 COVENTYA Group

- 6.4.8 Ecoviz Kft

- 6.4.9 Electrolytic Technologies LLC

- 6.4.10 Hangzhou ASIA Chemical Engineering Co., Ltd

- 6.4.11 HTH Pools (Arch Chemicals)

- 6.4.12 Inovyn

- 6.4.13 JSC AVANGARD

- 6.4.14 Lanxess AG

- 6.4.15 Lonza Group

- 6.4.16 Nouryon

- 6.4.17 Occidental Chemical (OxyChem)

- 6.4.18 Odyssey Manufacturing Co.

- 6.4.19 Olin Corporation

- 6.4.20 Osaka Soda Co. Ltd.

- 6.4.21 Shijiazhuang Xinlongwei Chemical

- 6.4.22 Shouguang Tianwei Chemical

- 6.4.23 Tianjin Yufeng Chemical

- 6.4.24 Tosoh Corporation

- 6.4.25 Union Overseas Enterprise Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Demand from the Aquaculture Industry