PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844471

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844471

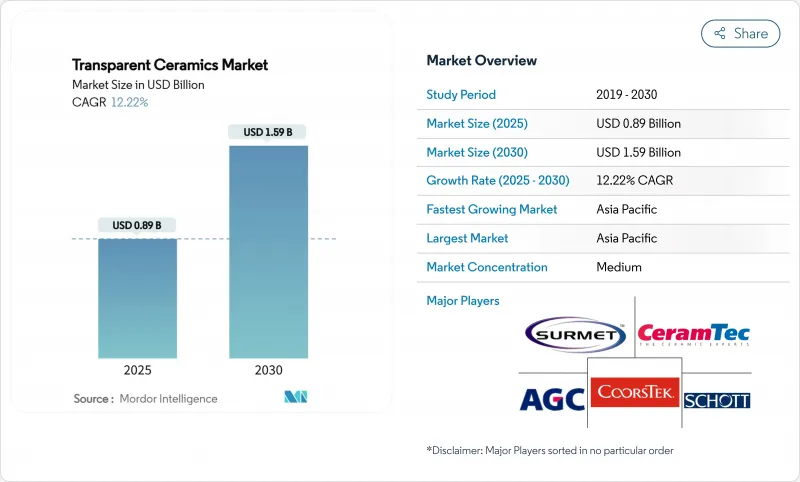

Transparent Ceramics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Transparent Ceramics Market size is estimated at USD 0.89 billion in 2025, and is expected to reach USD 1.59 billion by 2030, at a CAGR of 12.22% during the forecast period (2025-2030).

Demand for fusion-grade laser optics, hypersonic vehicle domes, and next-generation optoelectronic components continues to redefine performance baselines, spurring investment in manufacturing technologies that shrink defect rates and expand throughput. Asia Pacific, supported by semiconductor and aerospace buildouts in China and Japan, contributes the largest revenue block and simultaneously registers the fastest regional growth, reflecting scale economics and coordinated industrial policy. Crystalline-structure ceramics dominate current shipments, especially in military optics, yet cost-advantaged glass-ceramic variants are closing ground as consumer electronics brands pivot to scratch-resistant, high-clarity covers. Material leadership resides with sapphire, but aluminum oxynitride's ballistic performance is allowing it to seize design-in wins for next-generation infrared (IR) windows on hypersonic platforms. The competitive field, while moderately consolidated, is tilting toward vertical integration as players race to secure rare-earth inputs and proprietary sintering know-how, lowering unit costs and unlocking capacity for high-volume sectors such as dental implants and LED lighting.

Global Transparent Ceramics Market Trends and Insights

Accelerating Usage in Optics & Optoelectronics

Laser-driven manufacturing, lidar, and photonic-integrated circuits are fueling record off-take for high-purity, low-defect transparent ceramics. Titanium:sapphire-on-insulator prototypes have delivered compact layouts that cut system footprints while boosting power density, signaling commercial feasibility for wafer-level laser arrays. Ce-doped garnet ceramics now demonstrate luminance saturation thresholds of 65 W mm-2, offering durable, thermally stable alternatives to single-crystal gain media in LED backlights and industrial lasers. The transparent ceramics market is, therefore, intertwined with broadband communications, where miniaturization pressures amplify the value of materials that can survive intense photon flux and elevated junction temperatures.

Growing Demand from Aerospace & Defense

Transparent ceramics meet the dual mandate of optical transmission and high-temperature resilience imposed by supersonic aircraft, missile seekers, and satellite sensor windows. Porous Si3N4 radomes have reached 56% porosity while preserving mechanical integrity, trimming overall weight for long-range interceptors. Transparent domes on hypersonic glide bodies must tolerate 2,000 °C skin temperatures; AlON and spinel exceed such thresholds while resisting thermal shock. U.S. federal roadmaps name these ceramics as cornerstone materials for resilient energy weapon optics and directed-energy systems. Substitution away from germanium windows further elevates the transparent ceramics market, alleviating strategic mineral supply risk through chalcogenide glass derivatives that match sensor bandwidth needs.

High Production Cost

Transparent ceramics require high-purity feedstocks and multi-stage sintering profiles that push furnace dwell times and electricity usage well above standard tile or structural ceramics. Two-step sintering raises density but demands precision thermal ramps, while diamond-wheel finishing of sapphire parts adds capex for high-RPM spindles and coolant systems. Industry carbon-footprint scrutiny is accelerating shifts to green hydrogen kilns, but near-term conversion expenses weigh on margins.

Other drivers and restraints analyzed in the detailed report include:

- Advanced Ceramics Increasingly Replacing Plastics and Metals

- Fusion-Grade High-Power Ceramic Lasers

- Manufacturing Complexity & Yield Losses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Crystalline variants secured 64.67% transparent ceramics market share in 2024, validated by consistently higher transmission in the 0.3-5 μm band and compressive strengths above 2 GPa. Fine-grain sapphire domes and YAG laser slabs illustrate the segment's versatility across radomes and solid-state lasers. Non-crystalline glass-ceramics, conversely, capitalized on agile melt-casting lines and lower scrap rates, capturing handset lens covers and smart-watch backplates. Their 12.78% CAGR underscores demand elasticity in price-sensitive consumer channels.

Cordierite glass-ceramics that combine 82.3% transmittance with sub-2.6 ppm °C-1 thermal expansion pave the way for monolithic mobile screens that forego polymer lamination. Meanwhile, advanced nucleant systems-P2O5 + ZrO2 + TiO2-shift crystallization to the bulk, enhancing mechanical tensile strength without sacrificing clarity. Spark plasma sintering reduces processing windows from hours to minutes, halving energy input and shrinking grain boundaries to suppress scattering.

The Transparent Ceramics Market Report is Segmented by Structure (Crystalline, Non-Crystalline), Material (Sapphire, Yttrium Aluminum Garnet, Aluminum Oxynitride, and More), Application (Optics & Optoelectronics, Aerospace & Defense, Mechanical & Chemical Processing, and More), and Geography (Asia Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific controlled 56.67% of 2024 sales, buoyed by entrenched sapphire boules in Hunan and wide-aperture AlON plates in Nagoya. Government stimulus for local semiconductor etching and display fabs furnishes anchor demand, while export-oriented defense conglomerates in China adopt spinel domes for next-generation ISR drones. By 2030, the region is poised to generate significant incremental revenue, growing at a rate of 14.23% CAGR. South Korea's nano transparent screen initiative cuts per-inch costs to one-tenth of OLED, broadening addressable display footprints and deepening local supply chains.

North America remains the technology vanguard, leveraging DARPA and DoE grants to demonstrate directed-energy laser couplers and fusion-grade optics. LightPath Technologies is substituting BDNL4 chalcogenide glass for germanium, insulating the defense base from geopolitical risk. Mexico's electronics maquiladoras integrate glass-ceramic heat spreaders into power modules, signaling outward regional diffusion of advanced materials.

Europe positions itself on value-added, low-carbon production. SCHOTT's EUR 450 million capital program includes a hydrogen-fired float line that delivered its first CO2-neutral glass in 2024, validating feasibility for ceramic sintering kilns. Germany's Ceramic Composites network targets a doubling of oxide-fiber throughput by 2025, critical for ceramic-matrix composites in aerospace turbines. The Middle East and Africa record nascent but strategic uptake, especially in concentrated solar power fields where dust-resistant, IR-transparent shields elongate heliostat lifetimes.

- AGC Inc.

- CeramTec GmbH

- CILAS

- CoorsTek Inc.

- Deisenroth Engineering GmbH

- Fraunhofer IKTS

- General Electric

- II-VI Optical Systems

- Konoshima Chemical Co. Ltd

- Kyocera Corporation

- Meller Optics Inc

- Murata Manufacturing

- OptoCity Inc.

- Philips Lighting Holdings

- Raytheon Technologies (RTX)

- Saint-Gobain Group

- SCHOTT AG

- Surmet Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating usage in optics and optoelectronics

- 4.2.2 Growing demand from aerospace and defense

- 4.2.3 Advanced Ceramics Increasingly Replacing Plastics and Metals

- 4.2.4 Fusion-grade high-power ceramic lasers

- 4.2.5 Rising use of transparent ceramics in IR domes for hypersonic vehicles

- 4.3 Market Restraints

- 4.3.1 High production cost

- 4.3.2 Manufacturing complexity and yield losses

- 4.3.3 Sustainability issues in rare-earth mining

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts

- 5.1 By Structure

- 5.1.1 Crystalline

- 5.1.2 Non-crystalline (Glass-ceramic)

- 5.2 By Material

- 5.2.1 Sapphire (Al2O3)

- 5.2.2 Yttrium Aluminum Garnet (YAG)

- 5.2.3 Aluminum Oxynitride (AlON)

- 5.2.4 Spinel (MgAl2O4)

- 5.2.5 Yttria-stabilized Zirconia (YSZ)

- 5.2.6 Other Advanced Materials

- 5.3 By Application

- 5.3.1 Optics and Optoelectronics

- 5.3.2 Aerospace and Defense

- 5.3.3 Mechanical and Chemical Processing

- 5.3.4 Healthcare and Dental

- 5.3.5 Consumer Electronics and Goods

- 5.3.6 Energy and Power

- 5.3.7 Others Applications

- 5.4 By Geography

- 5.4.1 Asia Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 Australia and New Zealand

- 5.4.1.6 ASEAN countries

- 5.4.1.7 Rest of Asia Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 NORDIC

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 UAE

- 5.4.5.3 South Africa

- 5.4.5.4 Egypyt

- 5.4.5.5 Nigeria

- 5.4.5.6 Rest of Middle East and Africa

- 5.4.1 Asia Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 AGC Inc.

- 6.4.2 CeramTec GmbH

- 6.4.3 CILAS

- 6.4.4 CoorsTek Inc.

- 6.4.5 Deisenroth Engineering GmbH

- 6.4.6 Fraunhofer IKTS

- 6.4.7 General Electric

- 6.4.8 II-VI Optical Systems

- 6.4.9 Konoshima Chemical Co. Ltd

- 6.4.10 Kyocera Corporation

- 6.4.11 Meller Optics Inc

- 6.4.12 Murata Manufacturing

- 6.4.13 OptoCity Inc.

- 6.4.14 Philips Lighting Holdings

- 6.4.15 Raytheon Technologies (RTX)

- 6.4.16 Saint-Gobain Group

- 6.4.17 SCHOTT AG

- 6.4.18 Surmet Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment

- 7.2 Increasing Demand in the Medical Sector