PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844475

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844475

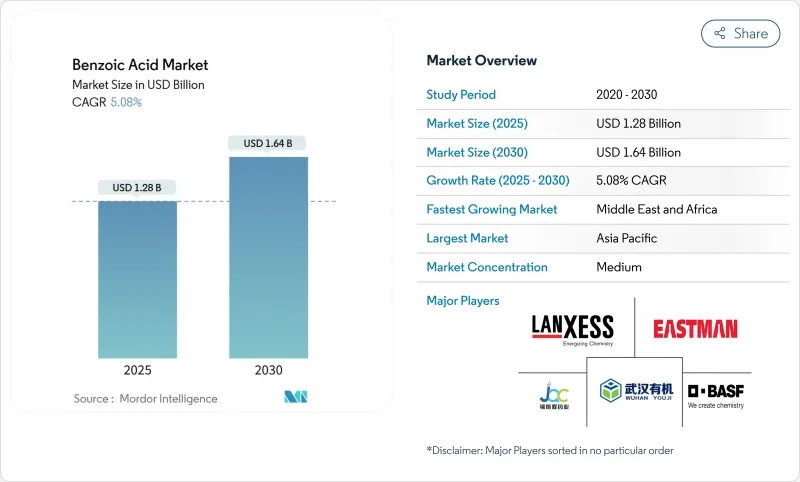

Benzoic Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The benzoic acid market size is expected to reach USD 1.28 billion in 2025 and is expected to grow to USD 1.64 billion by 2030, growing at a CAGR of 5.08%.

The market growth is driven by regulations that focus on extended shelf-life requirements, phthalate replacement, and high-purity manufacturing processes. The European Union's stricter food-contact regulations and the United States Food and Drug Administration's removal of 25 ortho-phthalate plasticizers create new opportunities in food, pharmaceutical, and plasticizer applications. The Asia-Pacific region maintains its production dominance, while the Middle East and Africa show the highest growth rate due to food processing industrialization. The market sees increasing adoption of liquid formulations, ultra-high purity grades, and benzoate plasticizers, driven by ease of handling, pharmaceutical quality requirements, and regulatory support. The competitive landscape remains moderate, with global companies and regional suppliers sharing market presence, leading to advancements in green chemistry and continuous processing.

Global Benzoic Acid Market Trends and Insights

Regulatory push for longer shelf-life pharmaceuticals in emerging economies

Pharmaceutical regulators in emerging markets are implementing stricter shelf-life requirements, increasing the demand for benzoic acid. The focus on extended product stability is significant in liquid formulations, where benzoic acid prevents microbial growth and extends shelf life by inhibiting bacterial and fungal contamination. This regulatory trend drives consistent demand growth in the pharmaceutical sector, particularly in countries like China, India, and Brazil, where healthcare regulations are becoming more stringent. The alignment of regulations across Asia-Pacific markets positions benzoic acid as a key preservative, particularly in oral and parenteral formulations that require compatibility with active pharmaceutical ingredients. These formulations include oral solutions, suspensions, injectable medications, and other liquid pharmaceutical products. The safety requirements for neonatal applications are increasing demand for higher purity grades, with specifications of purity, supporting growth in ultra-high purity segments. This demand is further driven by the growing focus on pediatric medications, the need for contamination-free preservatives in sensitive pharmaceutical applications, and the increasing adoption of benzoic acid in novel drug delivery systems. The pharmaceutical industry's emphasis on quality control and regulatory compliance has led to increased investment in advanced purification technologies and testing methods to ensure benzoic acid meets these stringent requirements.

Expansion of benzoyl chloride usage in agrochemical synthesis

Benzoyl chloride, a benzoic acid derivative, is a key component in manufacturing herbicides and fungicides, particularly chloramben analogs that control resistant weeds and improve crop yields. The compound's properties allow manufacturers to develop specific formulations that address pest resistance while maintaining crop safety. Indian formulators and Chinese contract manufacturers are expanding their production capabilities by implementing improved process controls and quality systems to meet global agrochemical companies' requirements for products with specific impurity profiles. These manufacturing enhancements include better filtration systems, automated monitoring, and comprehensive quality testing protocols. Research into amide-bearing sulfonate derivatives has increased due to the agricultural sector's sustainability focus. Laboratory studies show these derivatives achieve higher lethal-concentration effectiveness against target organisms compared to conventional active ingredients, potentially reducing application rates while maintaining pest control efficiency. The market growth depends on achieving cost-effectiveness while meeting environmental regulations and safety requirements, and maintaining consistent demand for benzoic acid in the agricultural chemical supply chain. The industry continues to invest in benzoyl chloride-based solutions for developing new crop protection products.

Shift towards clean-label preservatives limiting synthetic benzoate adoption

The growing consumer preference for natural ingredients is compelling food manufacturers to seek alternatives to synthetic preservatives, including sodium benzoate. European market data indicates rising demand for clean-label products that offer transparency in ingredient sourcing and manufacturing processes, with consumers increasingly scrutinizing product labels and demanding natural alternatives. Natural antimicrobial compounds, including plant extracts, essential oils, and microbial metabolites, have emerged as potential replacements for synthetic preservatives. These natural compounds demonstrate effectiveness in controlling foodborne pathogens while aligning with consumer preferences for clean-label products. The meat industry has shown significant interest in natural preservatives, extensively exploring options such as bacteriophages, bacteriocins, and antimicrobial peptides as substitutes for synthetic chemicals. These alternatives have demonstrated promising results in laboratory and commercial settings. However, the widespread adoption of natural alternatives faces limitations due to standardization challenges, higher production costs, and varying antimicrobial efficacy across different food applications. The regulatory environment, particularly in the EU, is shifting toward favoring natural ingredients through stricter guidelines and approval processes for synthetic preservatives, which presents both opportunities and challenges for benzoic acid manufacturers in terms of market adaptation and product development.

Other drivers and restraints analyzed in the detailed report include:

- Substitution of phthalate plasticizers with benzoate-based alternatives

- Growing demand for high-purity benzoic acid for specialty coatings

- Price volatility of raw materials

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The benzoic acid market for anhydrous grades held a dominant 53.21% market share in 2024, supported by its extensive applications across industries. Anhydrous powders serve as the preferred choice for dry-mix foods, polymer catalysts, and granular animal-feed blends, owing to their low moisture absorption and efficient bulk storage properties. These characteristics help maintain product stability and quality during storage periods. The liquid forms segment is growing at a 6.34% CAGR, driven by processing efficiency and operational benefits. Pharmaceutical syrup manufacturers use liquid benzoic acid solutions to streamline production processes by eliminating on-site dissolution steps and maintaining precise assay tolerances, which reduces batch variations and improves product consistency. Industrial coating manufacturers achieve faster homogenization by using liquids in high-shear reactors, reducing production time and improving efficiency.

Process intensification has significantly improved liquid uptake capabilities in manufacturing processes. Comprehensive laboratory tests indicate that liquid benzoic acid functions more effectively as a chain-stop agent in alkyd resins, resulting in enhanced gloss retention and surface finish quality. These substantial performance improvements, combined with reduced dust emissions during handling and processing, support the segment's stronger growth trajectory compared to the overall benzoic acid market. The improved efficiency in liquid form has also led to reduced processing times and better integration in various industrial applications, further strengthening its market position.

The 99.5-99.9% purity segment dominates with 62.78% market share in 2024, primarily due to its widespread use in critical manufacturing processes. Ultra-high purity grades above 99.9% are growing at 7.22% CAGR through 2030, driven by increasing demand from specialty coating and pharmaceutical applications requiring stringent quality specifications. The pharmaceutical industry requires higher purity grades, especially for parenteral formulations that must meet strict pharmacopeial standards for patient safety and regulatory compliance. Research into bio-based production methods is developing innovative processes for ultra-high purity levels while maintaining cost efficiency, supported by advanced purification technologies including membrane separation and chromatographic techniques.

The 99.0-99.5% purity grade meets essential requirements for food preservation and basic industrial applications, offering reliable performance at competitive price points. This grade finds extensive use in general manufacturing processes where ultra-high purity is not critical. Manufacturers are implementing sophisticated analytical methods and comprehensive quality control systems to achieve higher purity specifications consistently, supporting premium segment growth while optimizing operational efficiency and production yields.

The Benzoic Acid Market Report is Segmented by Form (Liquid, Anhydrous, and More), Purity Grade (99. 0-99. 5%, 99. 5-99. 9%, and More), Derivative (Sodium Benzoate, Potassium Benzoate, and More), Application (Food and Beverage, Pharmaceuticals, Chemicals, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 42.19% of the global market in 2024, with China's large-scale aromatic complexes, including Zhejiang Petroleum & Chemical's 11.8 million-ton facility, providing substantial toluene feedstock supply. The region's processors utilize export-oriented regulations and integrated logistics networks to optimize distribution channels and reduce operational costs. India's expanding pharmaceutical and food-processing sectors increase demand through multiple applications, including preservatives and intermediates, while Japan's technological capabilities enable the production of high-quality grades for electronic coatings and specialized industrial applications. ASEAN countries utilize duty-free trade agreements to establish distribution centers for exports to Europe and North America, integrating the benzoic acid market into regional supply chains and creating value-added opportunities for local manufacturers.

The Middle East and Africa region exhibits the highest growth rate at 6.83% CAGR, supported by increasing urbanization driving demand for preserved food products, beverages, and personal care items, alongside government initiatives attracting polymer manufacturers through tax incentives and infrastructure development. Saudi Arabia's test facilities assess benzoate plasticizers for PVC cable insulation production, supporting domestic manufacturing requirements and reducing import dependency.

North America benefits from FDA regulatory framework and manufacturer preferences for phthalate-free packaging solutions across food, beverage, and consumer goods sectors. Europe's market adapts to Regulation (EU) 2024/3190 on bisphenol limitations, encouraging packaging manufacturers to adopt benzoate alternatives in food contact materials and consumer packaging, while recycling requirements affect cost considerations and material selection processes.

- Lanxess AG

- Eastman Chemical Company

- Wuhan Youji Industry Co., Ltd.

- JQC(Huayin) Pharmaceutical Co., Ltd.

- BASF SE

- I G Petrochemicals Ltd.

- Chemcrux Enterprises Ltd.

- Ganesh Benzoplast Ltd.

- FUSHIMI Pharmaceutical Co., Ltd.

- Jiangsu Sanmu Group Co., Ltd.

- Thermo Fisher Scientific Inc.

- The Merck Group

- Smart Chemicals Group Co., Ltd.

- San Fu Chemical Co., Ltd.

- Mitsui Bussan Chemicals Co., Ltd.

- Spectrum Laboratory Products, Inc.

- Tokyo Chemical Industry Co., Ltd

- Sisco Research Laboratories Pvt Ltd

- Central Drug House (P) Ltd

- Otto Chemie Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for longer shelf-life pharmaceuticals in emerging economies

- 4.2.2 Expansion of benzoyl chloride usage in agrochemical synthesis

- 4.2.3 Substitution of phthalate plasticizers with benzoate-based alternatives

- 4.2.4 Growing demand for high-purity benzoic acid for specialty coatings

- 4.2.5 Rise in demand for packaged and convenience foods

- 4.2.6 Technological advancements in production

- 4.3 Market Restraints

- 4.3.1 Shift towards clean-label preservatives limiting synthetic benzoate adoption

- 4.3.2 Price volatality of raw materials

- 4.3.3 Healh and safetu concerns

- 4.3.4 Competition from natural preservatives

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Form

- 5.1.1 Liquid

- 5.1.2 Anhydrous

- 5.1.3 Powder/Crystal

- 5.2 By Purity Grade

- 5.2.1 99.0-99.5%

- 5.2.2 99.5-99.9%

- 5.2.3 Above 99.9%

- 5.3 By Derivative

- 5.3.1 Sodium Benzoate

- 5.3.2 Potassium Benzoate

- 5.3.3 Benzyl Benzoate

- 5.3.4 Benzoyl Chloride

- 5.3.5 Benzoate Plasticizers

- 5.3.6 Other Derivatives

- 5.4 By Application

- 5.4.1 Food and Beverage

- 5.4.1.1 Bakery

- 5.4.1.2 Confectionery

- 5.4.1.3 Dairy

- 5.4.1.4 Beverage

- 5.4.1.5 Sauces and Dressings

- 5.4.1.6 Others

- 5.4.2 Pharmaceuticals

- 5.4.3 Chemicals

- 5.4.4 Personal Care and Cosmetics

- 5.4.5 Animal Feed

- 5.4.6 Others

- 5.4.1 Food and Beverage

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Italy

- 5.5.2.6 Spain

- 5.5.2.7 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 India

- 5.5.3.2 China

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Lanxess AG

- 6.4.2 Eastman Chemical Company

- 6.4.3 Wuhan Youji Industry Co., Ltd.

- 6.4.4 JQC(Huayin) Pharmaceutical Co., Ltd.

- 6.4.5 BASF SE

- 6.4.6 I G Petrochemicals Ltd.

- 6.4.7 Chemcrux Enterprises Ltd.

- 6.4.8 Ganesh Benzoplast Ltd.

- 6.4.9 FUSHIMI Pharmaceutical Co., Ltd.

- 6.4.10 Jiangsu Sanmu Group Co., Ltd.

- 6.4.11 Thermo Fisher Scientific Inc.

- 6.4.12 The Merck Group

- 6.4.13 Smart Chemicals Group Co., Ltd.

- 6.4.14 San Fu Chemical Co., Ltd.

- 6.4.15 Mitsui Bussan Chemicals Co., Ltd.

- 6.4.16 Spectrum Laboratory Products, Inc.

- 6.4.17 Tokyo Chemical Industry Co., Ltd

- 6.4.18 Sisco Research Laboratories Pvt Ltd

- 6.4.19 Central Drug House (P) Ltd

- 6.4.20 Otto Chemie Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK