PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844502

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844502

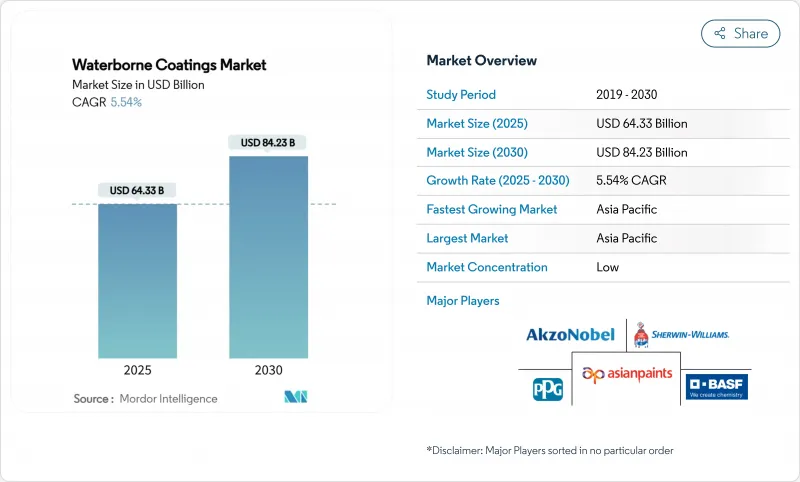

Waterborne Coatings - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Waterborne Coatings Market size is estimated at USD 64.33 billion in 2025, and is expected to reach USD 84.23 billion by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Robust demand is anchored in tighter volatile-organic-compound caps, large-scale infrastructure programs, and accelerating OEM conversions that together steer spending toward low-emission chemistries. The Environmental Protection Agency's January 2027 compliance date extension under the National Aerosol Coatings Rule illustrates the regulatory tightrope producers must walk as they shift portfolios toward greener formulations. Asian construction booms, automotive refinishing upgrades, and bio-based resin breakthroughs further reinforce the long-term trajectory of the waterborne coatings market. Competitive strategies increasingly revolve around supply-secure rheology packages, PFAS-free durability improvements, and digital color platforms, creating fresh avenues for value capture despite raw-material cost volatility.

Global Waterborne Coatings Market Trends and Insights

Stricter VOC and Decarbonization Mandates

California's Air Resources Board restricts industrial-maintenance VOCs to 50 g/L, nearly a ten-fold tightening against federal thresholds, forcing formulators to engineer ultra-low emission blends that still pass adhesion, gloss, and durability tests. Similar tightening unfolds across Canada, where national limits on 130 product classes took effect in January 2024 and extend compliance risk for multinationals with globally harmonized SKUs. In Europe, the updated REACH Restrictions Roadmap targets PVC additives and ortho-phthalates, compressing the adoption window for PFAS-free polyols. As jurisdictions converge on ambitious decarbonization metrics, companies able to harmonize one waterborne specification across continents will lower compliance overhead and speed market entry, leaving laggards boxed into fragmented legacy lines.

Rapid Infrastructure Buildouts in Asia and Africa

China's stimulus-driven industrial revival and India's highway and metro expansions underpin the largest share of incremental liters for the waterborne coatings market. GCC construction pipelines add a climatic angle: quick-drying, low-odor waterborne primers now coat more than 45% of new residential stock in Bahrain and Oman, a share expected to widen as regional contractors chase LEED and Estidama credentials. The Asian Development Bank's 2024 Key Indicators emphasize that USD 1.7 trillion annual infrastructure spending must integrate climate resilience, thrusting waterborne chemistries with minimal indoor-air pollutants to the top of procurement lists. Conference dialogues from Indonesia to Kenya indicate that technical consultants increasingly recommend water-based epoxies for hospitals and schools, confirming an entrenched preference that raises the floor for long-run demand growth.

Scarcity and Price Volatility of Specialty Rheology Additives

Rheology packages, barely 4% by weight yet 13% of raw-material spend, swing overall production margins when supply tightens. Producer consolidation around complex ASE and HASE chemistries magnifies price shocks; a single outage can inflate global quarti-ton costs by double digits. Ribbon polysilicates promise pH-stable flow at lower dosages but need extensive compatibility trials, stretching innovation timelines to one year or more. Interim stock buffers remain the only hedge, locking capital that could fund new research and development.

Other drivers and restraints analyzed in the detailed report include:

- OEM One-Component Conversion from Solvent to Water Systems

- Bio-Based Resin Breakthroughs

- PFAS-Free Performance Gap for Extreme Anticorrosion

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylic formulations anchored 81.20% of the waterborne coatings market in 2024, reflecting a time-tested blend of UV resistance, color retention, and cost efficiency that builders and DIY consumers favor worldwide. The waterborne coatings market size for acrylic resins is projected to expand steadily, supported by municipal repaint programs and widening do-it-yourself channels.

Polyurethane, though a smaller base, is accelerating at 5.88% CAGR to 2030 as vehicle makers and industrial-maintenance engineers shift to one-component waterborne chemistries that cut booth times and raise chemical resistance. Epoxies retain their foothold in heavy anticorrosive service, though PFAS exit paths demand parallel innovation to sustain barrier metrics. Alkyds, squeezed by VOC levies, find reprieve in bio-sourced variants that swap azelaic acid for petroleum feedstocks, easing regulatory scrutiny while keeping familiar workability.

The Waterborne Coatings Report is Segmented by Resin Type (Acrylic, Alkyd, Epoxy, Polyurethane, Polyester, Polyvinylidene Chloride, and More), End-User Industry (Building and Construction, Automotive, Industrial, Wood, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 42.61% of global revenue in 2024 and is on track for a market-leading 6.01% CAGR to 2030, cementing its position as the growth engine for the waterborne coatings market. China's stimulus packages revive industrial output, expanding baseline demand for general-industrial enamels, while India's concrete-intensive smart-city corridors open long-haul orders for elastomeric roof and bridge membranes.

North America reflects regulatory maturity mixed with technology leadership. California's 50 g/L cap forces nationwide SKUs to align at the lowest permissible VOC, rippling through distribution chains and spurring rapid reformulation. Canada's national VOC rulebook harmonizes provincial limits, smoothing market access for compliant waterborne lines from Quebec to British Columbia.

Europe remains a sustainability trend-setter through the Chemicals Strategy for Sustainability, accelerating waterborne adoption across architectural, industrial, and DIY shelves. AkzoNobel's BASF-enabled Dulux Easycare relaunch in the UK advances its pledge to cut product carbon by 5% minimum, strengthening brand pull among eco-conscious shoppers. Eastern-European urbanization also drives incremental liters, especially in municipal road and rail renovations funded by EU recovery programs.

- Akzo Nobel N.V.

- Arkema

- Asian Paints Ltd.

- Axalta Coating Systems, LLC

- BASF

- Benjamin Moore & Co.

- Berger Paints India

- Chokwang Paint

- Dow

- Hempel A/S

- Jotun

- Kansai Paint Co., Ltd.

- KCC Corporation

- Masco Corporation

- Nippon Paint Holdings Co., Ltd.

- PPG Industries, Inc.

- RPM International Inc.

- Sika AG

- Teknos Group

- Tenaris

- The Sherwin-Williams Company

- Tikkurila

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stricter VOC and Decarbonization Mandates

- 4.2.2 Rapid Infrastructure Buildouts in Asia and Africa

- 4.2.3 OEM One-Component Conversion from Solvent to Water Systems

- 4.2.4 Bio-Based Resin Breakthroughs (eg, Lignin, Algae)

- 4.2.5 Smart Factory Demand for Low-Temperature Cure Lines

- 4.3 Market Restraints

- 4.3.1 Scarcity and Price Volatility of Specialty Rheology Additives

- 4.3.2 Humidity-Related Drying Defects in Tropical Regions

- 4.3.3 PFAS-Free Performance Gap for Extreme Anticorrosion

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Alkyd

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Polyester

- 5.1.6 Polyvinylidene Chloride (PVDC)

- 5.1.7 Polyvinylidene Fluoride (PVDF)

- 5.1.8 Other Resin Types

- 5.2 By End-user Industry

- 5.2.1 Building and Construction

- 5.2.2 Automotive

- 5.2.3 Industrial

- 5.2.4 Wood

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 Southeast Asia

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Russia

- 5.3.3.6 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 United Arab Emirates

- 5.3.5.3 South Africa

- 5.3.5.4 Egypt

- 5.3.5.5 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Akzo Nobel N.V.

- 6.4.2 Arkema

- 6.4.3 Asian Paints Ltd.

- 6.4.4 Axalta Coating Systems, LLC

- 6.4.5 BASF

- 6.4.6 Benjamin Moore & Co.

- 6.4.7 Berger Paints India

- 6.4.8 Chokwang Paint

- 6.4.9 Dow

- 6.4.10 Hempel A/S

- 6.4.11 Jotun

- 6.4.12 Kansai Paint Co., Ltd.

- 6.4.13 KCC Corporation

- 6.4.14 Masco Corporation

- 6.4.15 Nippon Paint Holdings Co., Ltd.

- 6.4.16 PPG Industries, Inc.

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Teknos Group

- 6.4.20 Tenaris

- 6.4.21 The Sherwin-Williams Company

- 6.4.22 Tikkurila

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment