PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844532

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844532

Functional Food Ingredient - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

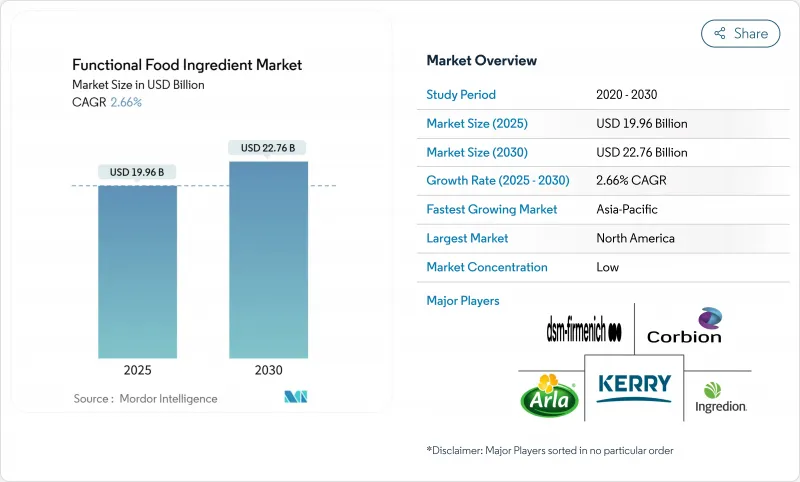

The functional food ingredient market size is estimated at USD 19.96 billion in 2025, and is expected to reach USD 22.76 billion by 2030, at a CAGR of 2.66% during the forecast period (2025-2030).

This measured growth trajectory reflects the sector's maturation as consumer awareness of health benefits drives sustained demand for fortified and enhanced food products. Functional food ingredients in functional food are targeted to offer specific functions that are more than just basic nutrition. These ingredients play a vital role in protecting against acute and chronic diseases. Functional foods contain natural or synthetic ingredients that promote optimal health and provide energy-boosting benefits. Prebiotics are one such ingredient that promotes the growth of bacteria in the large intestine that are beneficial to intestinal health while inhibiting the growth of bacteria that are potentially harmful to intestinal health.

Global Functional Food Ingredient Market Trends and Insights

Rising demand for nutritious, convenient, and fortified food products

Changes in consumer behavior drive market growth as health-conscious consumers prioritize functional benefits over taste and convenience. The increasing focus on health and wellness has led to a significant transformation in purchasing patterns, with consumers actively seeking products that offer specific nutritional advantages. This shift reflects increased nutritional awareness in mainstream food choices and creates sustained demand for fortified products that address specific health needs, from cognitive enhancement to immune support. DSM-Firmenich's launch of dry vitamin A palmitate in June 2024 for flour fortification, targeting 800 million people, demonstrates how ingredient innovation addresses global malnutrition challenges. The combination of convenience and nutritional requirements creates market opportunities for ingredients that deliver health benefits while maintaining product appeal and manufacturing efficiency. This trend has encouraged manufacturers to develop innovative solutions that balance nutritional content with practical considerations, leading to the emergence of new product categories and formulation techniques.

Botanical fortification of functional beverage to enhance health benefits

Plant-based fortification has become important as consumers increasingly prefer natural compounds over synthetic additives in their food and beverages. This shift reflects a broader trend toward healthier, more natural dietary choices and growing awareness of ingredient sourcing. Beverages are particularly well-suited for botanical fortification since liquid forms allow easier ingredient incorporation while maintaining optimal taste, texture, and nutritional properties. The integration process in beverages also enables better bioavailability and absorption of functional compounds. The growing preference for plant-derived functional ingredients supports environmental sustainability goals and clean-label demands, creating opportunities for companies that develop innovative botanical extraction and processing methods. The rising consumption of functional beverages continues to drive ingredient demand across global markets, with consumers seeking products that offer both refreshment and health benefits. According to UNESDA data from 2023, the United Kingdom's annual beverage consumption reached 15,095.2 million liters, demonstrating significant market potential for functional ingredients and highlighting the scale of opportunity for manufacturers in this segment.

High cost associated with functional ingredients products limiting widespread adoption

High prices of functional ingredients create significant barriers to market entry, especially in price-sensitive segments and emerging economies where consumers prioritize cost over health benefits. The substantial gap between price and perceived value restricts market growth as consumers carefully evaluate product benefits against costs. The complex manufacturing processes required for incorporating functional ingredients, including specialized equipment, rigorous quality control measures, and advanced processing techniques, increase production costs that manufacturers must often transfer to consumers. This challenge intensifies as new ingredient technologies demand substantial research and development investments, specialized expertise, and continuous innovation efforts while companies strive to maintain competitive pricing in an increasingly cost-conscious market.

Other drivers and restraints analyzed in the detailed report include:

- Technological advancement in encapsulation and delivery system

- Regulatory harmonization and GRAS pathway reforms

- Rising cases of food allergies and ingredient intolerances

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vitamins held a dominant 47.61% market share in 2024, supported by widespread consumer acceptance and established regulatory frameworks across global markets. Probiotics recorded the highest growth rate at 3.43% CAGR through 2030, supported by increasing scientific evidence of gut-brain axis benefits and the International Probiotics Association's efforts to improve FDA post-market assessment processes. Minerals and proteins maintained stable demand in their mature market segments, while omega-3 ingredients benefited from technical innovations, as demonstrated by Infusd Nutrition's water-soluble formulations that doubled the bioavailability compared to conventional emulsions.

Prebiotics demonstrated growth potential due to advances in microbiome research, despite having less regulatory framework compared to probiotics. The market segments reflect an industry shift toward functional ingredients with proven health benefits. Companies developing innovative delivery systems and evidence-based health claims gain competitive advantages, while traditional vitamin manufacturers experience margin pressure from generic competition.

The Functional Food Ingredients Market Report is Segmented by Product Type (Vitamins, Minerals, Proteins and Amino Acids, and More), Form (Powder, Liquid, and Others), Application (Bakery, Dairy and Dairy Alternatives, Meat and Seafood, and More). And Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America holds the dominant market position with a 33.55% share in 2024, supported by robust regulatory frameworks, high consumer awareness, and well-developed functional food infrastructure. Asia-Pacific is experiencing the highest growth rate at 3.99% CAGR through 2030, driven by increasing disposable incomes, growing health consciousness, and regulatory improvements in China, India, and Japan.

Europe maintains a significant market presence through strict quality standards and consumer demand for natural, scientifically validated functional ingredients, though complex regulations limit growth. China's recent approval of 24 nutrient supplements and 10 functional raw materials under new health food regulations highlights the regulatory advancement in Asia-Pacific. South America and the Middle East and Africa show growth potential due to expanding middle-class populations and increasing functional food awareness, but face constraints from infrastructure gaps and regulatory uncertainties.

Regional market dynamics vary based on consumer preferences, regulatory environments, and economic development stages. Japan's established functional food regulations, including FOSHU and FFC frameworks, serve as benchmarks for other Asia-Pacific markets balancing innovation and consumer protection. Market expansion success depends on companies' ability to understand regulatory requirements and cultural nuances while maintaining operational efficiency across regions.

- DSM-Firmenich AG

- Kerry Group plc

- Arla Foods amba

- Corbion N.V.

- Ingredion Incorporated

- Tate & Lyle PLC

- Glanbia PLC

- Lonza Group

- Cargill, Incoporated

- Novozymes A/S

- Taiyo Kagaku Co., Ltd.

- Wilmar International

- BASF SE

- Givaudan SA

- International Flavors and Fragrances Inc.

- Sabinsa Corp.

- Beneo GmbH

- Foodchem International

- Roquette Freres

- Archer Daniels Midland Company

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for nutritious, convenient, and fortified food products

- 4.2.2 Botanical fortification of functional beverage to enhance health benefits

- 4.2.3 Technological advancement in encapsulation and delivery system

- 4.2.4 Premiumization of functional products in developed markets

- 4.2.5 Growing prevalence of chronic diseases fueling demand for healthy food products

- 4.2.6 Regulatory harmonization and GRAS pathway reforms

- 4.3 Market Restraints

- 4.3.1 High cost associated with functional ingredients products limiting widespread adoption

- 4.3.2 Rising cases of food allergies and ingredient intolerances

- 4.3.3 Integration and quality control challenges in functional food production

- 4.3.4 Limited consumer awareness and misconceptions

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Vitamins

- 5.1.2 Minerals

- 5.1.3 Proteins and Amino Acids

- 5.1.4 Omega-3 Ingredients

- 5.1.5 Prebiotics

- 5.1.6 Probiotic

- 5.1.7 Other Functional Food Ingredients

- 5.2 By Form

- 5.2.1 Powder

- 5.2.2 Liquid

- 5.2.3 Others

- 5.3 By Application

- 5.3.1 Bakery

- 5.3.2 Dairy and Dairy Alternative Products

- 5.3.3 Meat and Seafood

- 5.3.4 Confectionary

- 5.3.5 Beverage

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Spain

- 5.4.2.4 France

- 5.4.2.5 Italy

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Company Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 DSM-Firmenich AG

- 6.4.2 Kerry Group plc

- 6.4.3 Arla Foods amba

- 6.4.4 Corbion N.V.

- 6.4.5 Ingredion Incorporated

- 6.4.6 Tate & Lyle PLC

- 6.4.7 Glanbia PLC

- 6.4.8 Lonza Group

- 6.4.9 Cargill, Incoporated

- 6.4.10 Novozymes A/S

- 6.4.11 Taiyo Kagaku Co., Ltd.

- 6.4.12 Wilmar International

- 6.4.13 BASF SE

- 6.4.14 Givaudan SA

- 6.4.15 International Flavors and Fragrances Inc.

- 6.4.16 Sabinsa Corp.

- 6.4.17 Beneo GmbH

- 6.4.18 Foodchem International

- 6.4.19 Roquette Freres

- 6.4.20 Archer Daniels Midland Company

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK