PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844542

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844542

Proximity Sensor - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

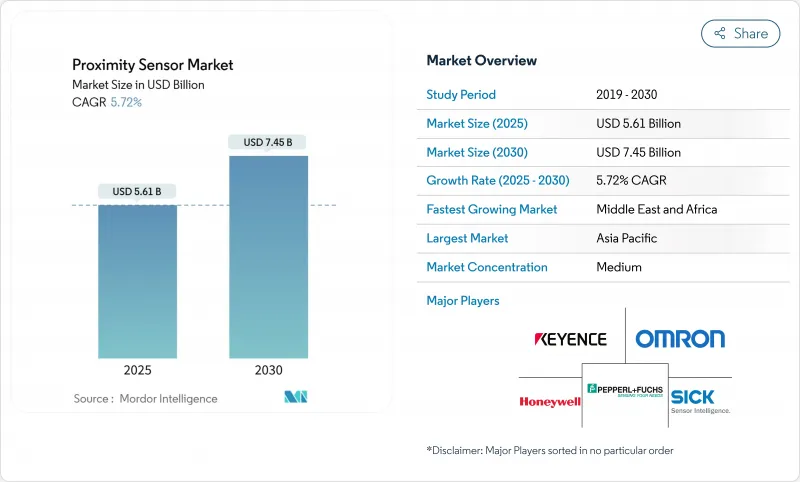

The proximity sensors market size is valued at USD 5.61 billion in 2025 and is forecast to grow at a 5.72% CAGR, reaching USD 7.45 billion by 2030.

The 2025 market value of USD 5.61 billion is supported by the intersection of electrified powertrains, aerospace safety directives, and Industry 4.0 retro-fit programs that demand precise, rugged, and cost-efficient detection devices. Growth momentum intensifies as IO-Link-enabled sensors feed real-time diagnostics to edge controllers, trimming factory downtime, while automotive OEM mandates for ISO 26262-certified devices accelerate supplier investments in functional-safety portfolios. Intensifying price pressure on copper coils and the need for electromagnetic compatibility (EMC) in high-power EV inverters temper near-term gains, yet regulatory shifts toward solid-state aviation sensors and the rapid uptake of hybrid Hall-effect, MEMS, and bulk-acoustic-wave devices reinforce a positive long-term outlook for the proximity sensors market.

Global Proximity Sensor Market Trends and Insights

Industry 4.0-led Retro-Fit Demand in Brownfield Asian Factories

Manufacturers across China, Vietnam, and Indonesia prefer upgrading existing lines with IO-Link-ready proximity sensors rather than building new plants, unlocking 15-20% efficiency gains and 30% cost cuts through 5G-enabled monitoring [gsma.com]. Suppliers offering drop-in cylindrical devices with PLC-friendly pinouts yet cloud-ready diagnostics dominate retro-fit tenders. Compatibility with legacy controls shields buyers from lengthy downtime, keeping the proximity sensors market buoyant until at least 2028.

Automotive OEM Mandates for ISO 26262-Certified Contactless Positioning

European and U.S. vehicle programs now specify inductive linear and rotary sensors qualified to ASIL C/D, displacing Hall-effect devices sensitive to stray fields. Dual-die architectures introduced by Melexis achieve +-0.85% accuracy over 12 mm strokes and offer built-in redundancy for brake, pedal, and steering modules [melexis.com]. Certification costs create a two-tier supply landscape, pushing smaller firms to license IP or exit, and further consolidating the proximity sensors market.

Coil-Copper Cost Volatility Impacting Inductive BOM in Europe

Three-year highs in copper spot prices raise coil costs by up to 25%, squeezing margins for German and Italian sensor producers already burdened by elevated electricity tariffs. Larger vendors hedge or vertically integrate copper supply, but smaller firms confront price-list resets quarterly, hampering competitiveness.

Other drivers and restraints analyzed in the detailed report include:

- Mini-LED/µLED Back-Light Integration in Smartphones (APAC)

- FAA & EASA Transition to Solid-State Landing-Gear Proximity Sensors

- EMC Compliance Failures in High-Power EV Inverters (US)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Inductive units delivered 35% of 2024 revenue, validating their status as the de-facto choice for metal detection on press lines and CNC machines embedded across the proximity sensors market. Rugged ferrite-core coils endure oil, chips, and vibration, ideal for retro-fits in APAC factories. Capacitive devices, advancing at 9.80% CAGR, now sense plastic housings and fluid levels in pharmaceutical clean rooms where inductive devices fail. The hybridization trend-combining Hall-effect for angle and capacitive for presence-pushes suppliers toward multi-physics ASICs that simplify installation and reduce SKU count.

Capacitive adoption accelerates because one sensor can cover glass, resin, or grain level without mechanical contact, aligning with food-safety mandates. Photoelectric SKUs retain niches requiring 10 m targeting over dusty conveyors, while ultrasonic variants serve chemical vats impervious to optical methods. Magnetic xMR sensors gain share within EV traction motors needing millidegree precision for field-oriented control. Collectively, these transitions keep the proximity sensors market varied and resilient.

Skewing to cost efficiency, fixed-distance cylinders amassed 60% of 2024 shipments. Automotive stamping plants, running identical door panels year-round, favor fixed thresholds to avoid accidental recalibration. However, short batch runs in electronics assembly spark an 8.50% CAGR for adjustable-distance models equipped with IO-Link parameterization. Production engineers tweak on-board firmware rather than swapping hardware, slashing changeover times. In plants moving toward lights-out operation, smart adjustable devices feed EQ timestamps and cycle counts to MES dashboards, deepening digital twins and elevating the proximity sensors market profile.

Maintenance teams cite reduced spares when one adjustable sensor covers multiple jig distances, offsetting its higher list price. Suppliers compete on LED-guided teach modes and NFC smartphone setup, reinforcing ease of use. Long term, firmware-driven range tuning is expected to become the default in flexible factories.

Smartphone pick-and-place stages, electric-motor commutation, and snap-fit quality checks keep 0-20 mm sensors at 45% of proximity sensors market size in 2024. Their solid-state ruggedness beats mechanical limit switches and reduces false rejects. Yet warehouse automation, AMRs, and pallet-shuttle systems require line-of-sight safety at two-meter plus distances, lifting>40 mm devices at a 7.20% CAGR. Suppliers respond with amplified transceivers and beam-forming optics capable of 4 m detection even in fog, complementing LiDAR and radar for 360° robot perception.

In intralogistics, longer-range proximity avoids blind-spot collisions without the cost of high-resolution vision. Hybrid ultrasonic-photoelectric stacks enter this space, integrating distance and presence into one SKU, reducing points of failure and wiring labor in high-bay racking.

The Proximity Sensors Market Report is Segmented by Technology (Inductive, Capacitive, and More), Product Type (Fixed-Distance, Adjustable-Distance), Sensing Range (0-20mm, 20-40m, M, Greater Than 40mm), Housing (Cylindrical, and More), Output Type (Digital, Analog, IO-Link), Channel Wiring (2-Wire, and More), End-User Industry (Automotive, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific retained 36% proximity sensors market share in 2024, buoyed by China's factory digitalization grants, Japan's robotics export leadership, and South Korea's semiconductor investments. Retro-fitting brownfield lines with IO-Link sensors boosts output without new buildings, aligning with local CapEx restrictions. Component makers co-locate sensor assembly near smartphone clusters, shrinking lead times amid tight product cycles. Governments subsidize 5G private networks, anchoring sensor data backbones that support real-time quality loops.

Europe remains a premium buyer base. German Tier-1s demand ASIL-D inductive encoders for steer-by-wire, while French aerospace integrators specify ELDEC sensors for harsh turbine bays. Continual copper price waves and high electricity tariffs raise European BOMs, nudging some coil-winding to Central Europe yet retaining R&D centers near OEMs. The continent's push for net-zero factories incentivizes IO-Link diagnostics that trim scrap and energy waste, reinforcing advanced use-case uptake across the proximity sensors market.

North America records steady but mature consumption, concentrated in aerospace, energy, and a burgeoning EV supply chain. U.S. energy grid modernization programs open niches for proximity sensors monitoring breaker position and valve status. Schneider Electric's USD 700 million cap-ex illustrates domestic appetite for digitized switchgear and panelboards that embed factory-calibrated sensors. Canada's mining automation and Mexico's auto assembly exports deepen regional demand.

The Middle East delivers the quickest 7.50% CAGR, with Saudi Arabia's petrochemical and utility plants installing predictive-maintenance suites featuring hundreds of IO-Link proximity nodes per site. Africa and South America, while early in automation adoption, lay groundwork through logistics and food-processing plants, offering long-tail upside to the global proximity sensors market.

- Keyence Corporation

- Omron Corporation

- Pepperl+Fuchs GmbH

- Sick AG

- Panasonic Holdings Corp.

- Honeywell International Inc.

- STMicroelectronics N.V.

- Schneider Electric SE

- Rockwell Automation Inc.

- IFM Electronic GmbH

- Turck Holding GmbH

- Datalogic SpA

- Delta Electronics Inc.

- Autonics Corporation

- Balluff GmbH

- Banner Engineering Corp.

- Texas Instruments Inc.

- Broadcom Inc.

- Littelfuse Inc.

- Baumer Group

- Vishay Intertechnology

- BorgWarner Inc.

- Allegro MicroSystems

- Leuze electronic GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0-led Retro-Fit Demand in Brownfield Asian Factories

- 4.2.2 Automotive OEM Mandates for ISO 26262-Certified Contactless Positioning

- 4.2.3 Mini-LED/LED Back-Light Integration in Smartphones (Asia-Pacific)

- 4.2.4 FAA and EASA Transition to Solid-State Landing-Gear Proximity Sensors

- 4.2.5 Building Automation and Smart Infrastructure IoT Integration

- 4.2.6 IO-Link Adoption in European Discrete Manufacturing Lines

- 4.3 Market Restraints

- 4.3.1 Coil-Copper Cost Volatility Impacting Inductive BOM in Europe

- 4.3.2 EMC Compliance Failures in High-Power EV Inverters (US)

- 4.3.3 Condensation-Driven False Trips in Food-Grade Photoelectric Sensors

- 4.3.4 ATEX-Zone Certification Lead-Times Delaying Middle-East Projects

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook (IEC 60947-5-2, ISO 13849)

- 4.6 Technological Outlook (Chip-level Hall, BAW, MEMS Hybrids)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment and Funding Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Inductive

- 5.1.2 Capacitive

- 5.1.3 Photoelectric

- 5.1.4 Magnetic (Hall-Effect and Reed)

- 5.1.5 Ultrasonic

- 5.1.6 Infra-Red and Others

- 5.2 By Product Type

- 5.2.1 Fixed-Distance Sensors

- 5.2.2 Adjustable-Distance Sensors

- 5.3 By Sensing Range

- 5.3.1 0 - 20 mm

- 5.3.2 20 - 40 mm

- 5.3.3 Greater than 40 mm

- 5.4 By Housing / Form Factor

- 5.4.1 Cylindrical

- 5.4.2 Rectangular

- 5.4.3 Slot / Channel

- 5.4.4 Miniature / PCB-Mount

- 5.4.5 Ring and Through-Beam

- 5.5 By Output Type

- 5.5.1 Digital (NPN / PNP)

- 5.5.2 Analog (0-10 V / 4-20 mA)

- 5.5.3 IO-Link and Other Smart Interfaces

- 5.6 By Channel Wiring

- 5.6.1 2-Wire AC/DC

- 5.6.2 3-Wire DC

- 5.6.3 4-Wire Complementary

- 5.7 By End-user Industry

- 5.7.1 Aerospace and Defense

- 5.7.2 Automotive

- 5.7.3 Industrial Automation and Robotics

- 5.7.4 Consumer Electronics and Wearables

- 5.7.5 Food and Beverage Processing

- 5.7.6 Healthcare and Medical Devices

- 5.7.7 Building Automation and Smart Infrastructure

- 5.7.8 Other Industries (Mining, Agriculture, Marine)

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 Europe

- 5.8.2.1 United Kingdom

- 5.8.2.2 Germany

- 5.8.2.3 France

- 5.8.2.4 Italy

- 5.8.2.5 Rest of Europe

- 5.8.3 Asia-Pacific

- 5.8.3.1 China

- 5.8.3.2 Japan

- 5.8.3.3 India

- 5.8.3.4 South Korea

- 5.8.3.5 Rest of Asia-Pacific

- 5.8.4 Middle East

- 5.8.4.1 Israel

- 5.8.4.2 Saudi Arabia

- 5.8.4.3 United Arab Emirates

- 5.8.4.4 Turkey

- 5.8.4.5 Rest of Middle East

- 5.8.5 Africa

- 5.8.5.1 South Africa

- 5.8.5.2 Egypt

- 5.8.5.3 Rest of Africa

- 5.8.6 South America

- 5.8.6.1 Brazil

- 5.8.6.2 Argentina

- 5.8.6.3 Rest of South America

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Keyence Corporation

- 6.4.2 Omron Corporation

- 6.4.3 Pepperl+Fuchs GmbH

- 6.4.4 Sick AG

- 6.4.5 Panasonic Holdings Corp.

- 6.4.6 Honeywell International Inc.

- 6.4.7 STMicroelectronics N.V.

- 6.4.8 Schneider Electric SE

- 6.4.9 Rockwell Automation Inc.

- 6.4.10 IFM Electronic GmbH

- 6.4.11 Turck Holding GmbH

- 6.4.12 Datalogic SpA

- 6.4.13 Delta Electronics Inc.

- 6.4.14 Autonics Corporation

- 6.4.15 Balluff GmbH

- 6.4.16 Banner Engineering Corp.

- 6.4.17 Texas Instruments Inc.

- 6.4.18 Broadcom Inc.

- 6.4.19 Littelfuse Inc.

- 6.4.20 Baumer Group

- 6.4.21 Vishay Intertechnology

- 6.4.22 BorgWarner Inc.

- 6.4.23 Allegro MicroSystems

- 6.4.24 Leuze electronic GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment