PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844605

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844605

Automotive All-wheel-drive - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

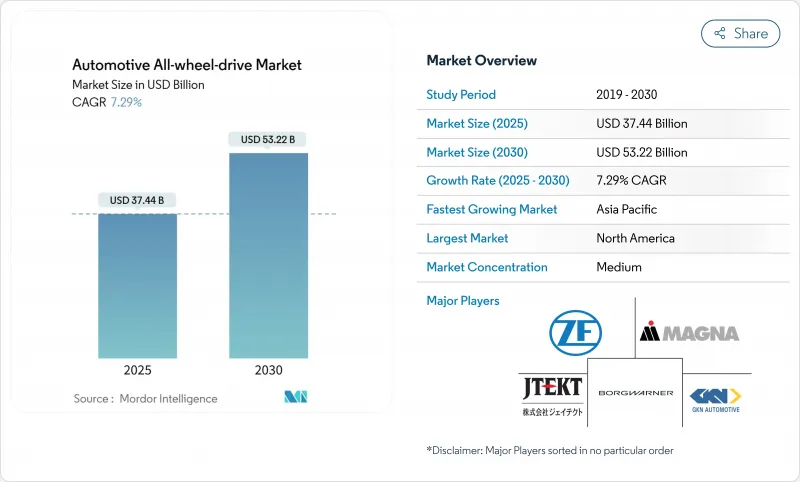

The automotive all-wheel drive market size reached USD 37.44 billion in 2025 and is expected to reach USD 53.22 billion by 2030, reflecting a steady 7.29% CAGR.

Strengthening safety mandates, rapid SUV and crossover uptake, and the maturing economics of dual-motor electrified drivelines together underpin this expansion. OEMs now prioritize traction management integration from the earliest platform stages because advanced driver-assistance systems depend on predictable torque delivery for optimal crash-avoidance performance. Electrification also removes long-standing mechanical cost penalties by replacing transfer cases and shafts with software-controlled e-motors. Supply-chain re-engineering around rare-earth magnets and power semiconductors is becoming pivotal as AWD content per vehicle rises. Competitive dynamics increasingly reward vertically integrated suppliers that fuse driveline hardware with over-the-air software services, transforming AWD from a one-time hardware feature into a recurring revenue channel for data-driven performance upgrades.

Global Automotive All-wheel-drive Market Trends and Insights

Soaring SUV and CUV Demand Worldwide

Global SUV and crossover output is forecast to hit 28 million units by 2030, and the share fitted with AWD is expected to climb from 45% in 2025 to 65% as traction systems shift from optional to default packaging. Buyers increasingly view AWD as a psychological safety premium even when driving predominantly on paved roads. Chinese brands now bundle AWD with competitive base pricing, lowering the historical cost barrier in emerging markets. OEMs frequently pair AWD with bundled ADAS suites, reinforcing safety credentials and boosting net margins. The utility mindset of consumers sustains year-round demand, making the automotive all-wheel drive market less dependent on winter seasonality.

Electrification-Driven Adoption of Dual-Motor e-AWD

Dual-motor BEVs achieve 9% better energy efficiency than single-motor layouts using add-on mechanical AWD according to SAE testing . Eliminating shafts and transfer cases cuts weight and unlocks precise torque control. Commercial operators benefit from lower maintenance and regenerative braking on all axles. Hyundai's new hybrid platform illustrates how e-AWD bridges ICE and full BEV architecture while containing costs.

Higher BOM Cost and Fuel/Energy Penalty vs 2WD

Traditional AWD adds USD 1,500-3,000 to build cost and reduces ICE fuel economy by roughly 1-2 mpg according to Argonne simulations . BEV range drops 10-15% in dual-motor versions, as demonstrated by the Hyundai Ioniq 5 data sheet. Manufacturers often convert AWD into standard equipment to dilute cost, yet this raises entry prices in value-focused segments. Battery prices continue to fall, but the near-term penalty remains a sales hurdle in emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Crash-Avoidance and Traction Safety Mandates

- Consumer Shift to Performance Handling in Premium Segments

- Magnet and Semiconductor Supply Bottlenecks for e-Actuators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Passenger cars captured 65.77% of the automotive all-wheel drive market share in 2024, illustrating how SUVs, crossovers, and increasingly AWD-equipped sedans have moved traction management from niche option to mainstream expectation. OEMs pair AWD with bundled safety and infotainment packages, boosting transaction prices while satisfying regulatory test cycles that reward predictable torque delivery. Consumers value the year-round confidence AWD offers on wet or icy roads, and insurers often reflect that benefit in lower premiums, reinforcing adoption even in temperate regions. Premium marques also use software-defined torque vectoring to differentiate ride dynamics across trim levels, turning AWD capability into an experiential selling point that supports higher residual values.

Commercial vehicles post the fastest expansion at a 7.96% CAGR through 2030 as parcel, utility, and emergency fleets adopt AWD to ensure mission-critical uptime under varied payloads and weather conditions. Electrified axles simplify installations by eliminating transfer cases, lowering maintenance downtime, and meeting zero-emission mandates spreading across large urban centers. Fleet telematics confirm that electric AWD reduces wheel-spin-related tire wear and enhances regenerative braking efficiency, improving total cost of ownership despite higher upfront prices. Government incentives for low-emission commercial transport and stricter safety audits further accelerate specification rates, positioning AWD as a core requirement for future fleet procurement cycles.

Internal combustion engines still represented 84.25% of the automotive all-wheel drive market size in 2024, but battery-electric powertrains are rising at a 10.11% CAGR as dual-motor layouts erase transfer-case costs and sharpen torque accuracy. ICE-centric platforms increasingly embed electric front or rear modules to offer hybrid AWD, future-proofing investments against tightening emissions rules. Reduced battery prices and government incentives jointly narrow the total-cost-of-ownership gap, prompting OEMs to launch AWD-equipped BEVs across mainstream price bands.

Fuel-cell initiatives indicate fresh commercial potential: BMW's collaboration with Toyota on a 2028 hydrogen SUV aims to pair long-range capability with electric AWD for heavy-duty or cold-weather routes. Dual-motor architectures also open software monetization paths, letting automakers sell performance upgrades over the air. In markets where carbon penalties inflate ICE running costs, these electrified systems gain further momentum, positioning e-AWD as the new baseline for traction, efficiency, and compliance.

The Automotive All-Wheel Drive Market Report is Segmented by Vehicle Type (Passenger Cars and Commercial Vehicles), Propulsion Type (Internal-Combustion Engine (ICE), Hybrid Electric Vehicle (HEV), and More), System Type (Part-Time/Manual AWD, Full-Time/Automatic AWD, and More), Component (Transfer Case, and More), Sales Channel, and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 43.17% of the automotive all-wheel drive market in 2024 with robust demand from pickups, SUVs, and fleet segments that confront snow, mixed terrain, and insurance rating incentives. U.S. regulators coupling AWD with mandated safety technologies reinforce uptake. Canada exhibits the highest AWD penetration among light vehicles because winter traction is a baseline expectation.

Asia Pacific is the fastest-growing region at an 8.55% CAGR. Chinese OEMs embed AWD into mainstream exports that undercut traditional two-wheel-drive competitors on price, reshaping global perceptions of cost-effective traction. India's introduction of the Maruti Suzuki e-Vitara, the country's first mass-market AWD EV, highlights the democratization of advanced driveline capability. South Korea continues to scale e-AWD across Hyundai and Kia portfolios, while Japan leverages hybrid AWD heritage for global deployments.

Europe shows steady but less dramatic growth, with electrified AWD as a favored route to meet Euro 7 emission goals while preserving performance. The continent's premium marques differentiate through fine-grained torque vectoring, integrated with ADAS aligned to General Safety Regulation II. South America and Africa remain smaller today yet illustrate rising adoption on the back of infrastructure upgrades and import duty reductions that lower retail prices for AWD crossovers.

- BorgWarner Inc.

- GKN Automotive (Melrose)

- ZF Friedrichshafen AG

- Magna International Inc.

- JTEKT Corporation

- Toyota Motor Corporation

- Nissan Motor Co. Ltd

- Continental AG

- Eaton Corporation PLC

- American Axle & Manufacturing

- Dana Inc.

- Haldex AB

- Hyundai Motor Company

- Audi AG

- BMW Group

- Mercedes-Benz Group AG

- Schaeffler AG

- Mahle GmbH

- Stellantis N.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Soaring SUV and CUV demand worldwide

- 4.2.2 Electrification-driven adoption of dual-motor e-AWD

- 4.2.3 Tightening crash-avoidance and traction safety mandates

- 4.2.4 Consumer shift to performance handling in premium segments

- 4.2.5 Climate-volatility prompting OEM AWD standardisation

- 4.2.6 OTA-enabled software torque-vectoring architectures

- 4.3 Market Restraints

- 4.3.1 Higher BOM cost and fuel/energy penalty vs 2WD

- 4.3.2 Magnet and semiconductor supply bottlenecks for e-actuators

- 4.3.3 Range-loss concern in battery-EVs

- 4.3.4 Autonomous-driving shift toward efficiency-optimised drivelines

- 4.4 Value / Supply-Chain Analysis

- 4.5 Technological Outlook

- 4.6 Regulatory Landscape

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 Market Size & Growth Forecasts (Value (USD))

- 5.1 By Vehicle Type

- 5.1.1 Passenger Cars

- 5.1.1.1 Hatchbacks and Sedans

- 5.1.1.2 SUVs and Crossovers

- 5.1.2 Commercial Vehicles

- 5.1.2.1 Light Commercial Vehicles

- 5.1.2.2 Heavy Trucks and Buses

- 5.1.1 Passenger Cars

- 5.2 By Propulsion Type

- 5.2.1 Internal-Combustion Engine (ICE)

- 5.2.2 Hybrid Electric Vehicle (HEV)

- 5.2.3 Battery Electric Vehicle (BEV)

- 5.2.4 Fuel-Cell Electric Vehicle (FCEV)

- 5.3 By System Type

- 5.3.1 Part-Time/Manual AWD

- 5.3.2 Full-Time/Automatic AWD

- 5.3.3 Electric/e-AWD (Dual-Motor, Quad-Motor)

- 5.3.4 Active Torque-Vectoring AWD

- 5.4 By Component

- 5.4.1 Transfer Case

- 5.4.2 Differential (Center, Front, Rear)

- 5.4.3 Coupling and Clutch Pack

- 5.4.4 Prop-Shaft and Drive Shaft

- 5.4.5 Control Unit and Software

- 5.5 By Sales Channel

- 5.5.1 OEM-Installed

- 5.5.2 Aftermarket Retrofit

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 South Africa

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 BorgWarner Inc.

- 6.4.2 GKN Automotive (Melrose)

- 6.4.3 ZF Friedrichshafen AG

- 6.4.4 Magna International Inc.

- 6.4.5 JTEKT Corporation

- 6.4.6 Toyota Motor Corporation

- 6.4.7 Nissan Motor Co. Ltd

- 6.4.8 Continental AG

- 6.4.9 Eaton Corporation PLC

- 6.4.10 American Axle & Manufacturing

- 6.4.11 Dana Inc.

- 6.4.12 Haldex AB

- 6.4.13 Hyundai Motor Company

- 6.4.14 Audi AG

- 6.4.15 BMW Group

- 6.4.16 Mercedes-Benz Group AG

- 6.4.17 Schaeffler AG

- 6.4.18 Mahle GmbH

- 6.4.19 Stellantis N.V.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment