PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844710

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1844710

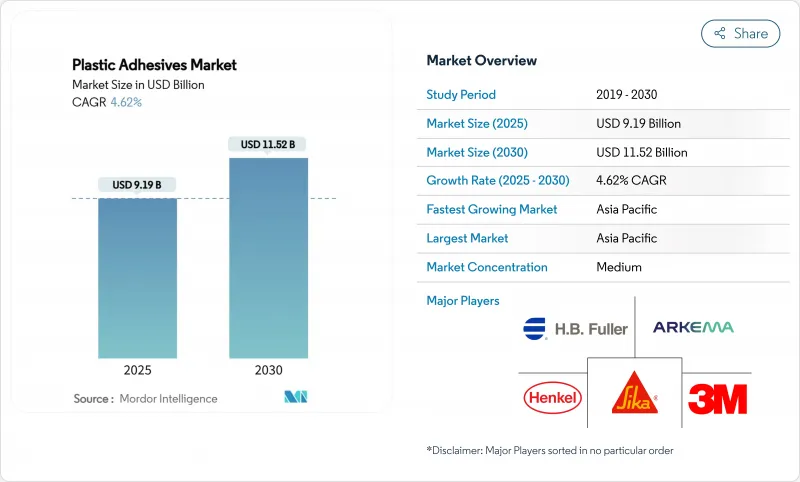

Plastic Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Plastic Adhesives Market size is estimated at USD 9.19 Billion in 2025, and is expected to reach USD 11.52 Billion by 2030, at a CAGR of 4.62% during the forecast period (2025-2030).

The plastic adhesives market is transitioning from general-purpose bonding agents toward specialized chemistries that address electric-vehicle battery packs, medical wearables, and next-generation construction panels. Rising demand for lightweight vehicles, the shift to bio-based polyurethane films in healthcare, and stricter VOC legislation are widening application scopes across automotive, medical, and building sectors. Producers are releasing water-based and bio-derived grades that comply with evolving emission ceilings in China, the European Union, and the United States, enabling the plastic adhesives market to capture opportunities created by sustainability mandates. Competitive dynamics remain fluid as manufacturers adopt targeted M&A and joint-development agreements to close technology gaps, balance feedstock cost risks, and reach new geographic pockets.

Global Plastic Adhesives Market Trends and Insights

Lightweight-vehicle push in automotive industry

Automakers are replacing mechanical fasteners with structural adhesives to eliminate excessive weight and strengthen mixed-material designs. A typical 2025 electric SUV now integrates more than 400 linear feet of adhesive compared with fewer than 30 feet two decades ago, illustrating the structural role adhesives play in joining aluminum, carbon fiber, and engineering plastics. Impact-toughened elastomer-epoxy hybrids developed at Nagoya University deliver 22-times higher impact strength than legacy epoxies, which allows thinner panels and energy-absorbing crash structures while maintaining crashworthiness. With most OEMs committing to lighter bodies for range extension, the plastic adhesives market expects automotive consumption to climb at double-digit annual rates through 2030.

Construction shift to high-performance plastics

Facade and glazing systems are moving toward lightweight composite panels that demand long-life, high-modulus bonding agents. Sika's protective glazing adhesive family can absorb seismic loads yet retain rigidity for hurricane-rated curtain walls. High-rise retrofits in developed economies and green-field megaprojects in Asia require plastic adhesives that balance fire resistance, UV durability, and fast installation. Fast-cure PVC TrimWelder products reach 80% handling strength in 30 minutes, enabling contractors to accelerate project cycles without sacrificing code compliance.

Petro-feedstock price volatility

Epoxy and polyurethane base-resin costs fluctuate with crude oil and propylene trends. German liquid epoxy prices rose 1.73% in January 2025 amid thin inventories, while Asian contracts slipped 1.4% later that month as sellers cleared surplus ahead of the Spring Festival. Polyethylene spikes of 5 ¢/lb in the United States further lifted packaging-grade adhesive inputs. Covestro signed a certified mass-balance supply agreement with H.B. Fuller to mitigate fossil feedstock swings through ISCC-PLUS-accredited bio-naphtha streams.

Other drivers and restraints analyzed in the detailed report include:

- Increasing demand from packaging and e-commerce industry

- Bio-based polyurethane films for medical wearables

- Tightening global VOC and hazard regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Epoxy grades accounted for 32.45% of the plastic adhesives market size in 2024, underpinning structural joints in automotive body-in-white assemblies and steel-reinforced concrete panels. The high glass-transition temperature and chemical resistance keep epoxies relevant where shear loads and temperature spikes converge. Specialty cyanoacrylates, acrylics, and hybrid urethanes, however, exhibit the fastest 5.18% CAGR, as OEMs pursue rapid bonding in miniature electronics and need cold-cure alternatives for heat-sensitive substrates. The plastic adhesives market therefore balances epoxy's entrenched share with emergent niche chemistries that emphasize speed and flexibility. Cyanoacrylate packages such as H.B. Fuller's Cyberbond line allow viscosity tailoring for medical device micro-dosing while meeting ISO 10993 cytotoxicity requirements. Non-isocyanate polyurethanes made from bio-derived cyclic carbonates are scaling pilot lines, signalling a broader pivot toward sustainable resins inside the plastic adhesives market.

Manufacturers layer R&D to optimise adhesion promoters that interface with low-surface-energy polyolefins, aiming to unlock higher peel strengths without primers. Silicone-epoxy hybrids maintain hermetic seals in high-temperature electronics modules, giving formulators another route to differentiate. As environmental bans curb bisphenol-A derivatives, epoxy suppliers accelerate the launch of bis-F and novolac alternatives, guarding their sizeable plastic adhesives market share while aligning with upcoming endocrine-disruptor reviews in the EU.

The Plastic Adhesives Market Report is Segmented by Resin Type (Epoxy, Cyanoacrylate, Urethane, Silicones, Other Resin Types), Technology (Solvent-Based, Water-Based), End-User Industry (Automotive, Building and Construction, Electrical and Electronics, Medical, Packaging, Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific remains the principal manufacturing hub for engineering plastics, electronics, and footwear, positioning the region as the largest revenue contributor to the plastic adhesives market. China's EV output, India's highway and housing programs, and ASEAN's packaging plants collectively amplify consumption. Government initiatives such as India's Smart City Mission continue to stimulate public-works spending that relies on polymer-bonded panels and pipes.

North America, while mature, registers steady gains through stringent fuel-economy and building-energy codes that promote lightweight composites and air-tight building envelopes. The United States Environmental Protection Agency's push toward low-GWP construction materials accelerates demand for low-smog adhesives in roofing and insulation boards. The plastic adhesives market also benefits from the United States-Mexico-Canada Agreement, which incentivises regional sourcing of automotive adhesives to qualify for tariff exemptions.

Europe leverages its Green Deal framework to catalyse recyclable adhesive innovation. Producers adapt formulas to disassemble end-of-life consumer goods and enable closed-loop plastic flows. Stricter EN 16603-20-01 outgassing criteria in aerospace applications pressurise suppliers to certify space-grade adhesives, opening a niche yet valuable tier within the plastic adhesives market.

The Middle East and Africa host expansion projects in desalination, solar infrastructure, and high-rise hospitality. Premium hotel builds specify silicone weather-seals rated for desert temperatures, supporting incremental growth. Latin America's construction rebound and on-shore electronics assembly in Mexico and Brazil add diverse demand layers, albeit from a smaller base than the three dominant regions.

- 3M

- Arkema

- Avery Dennison Corporation

- BASF

- Dow

- Dymax

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- Huntsman International LLC

- INTERTRONICS

- Master Bond Inc.

- Panacol-Elosol GmbH

- Permabond LLC

- Pidilite Industries Ltd.

- Sika AG

- Toyochem Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Lightweight-vehicle push in automotive industry

- 4.2.2 Construction shift to high-performance plastics

- 4.2.3 Increasing demand from packaging and e-commerce industry

- 4.2.4 Bio-based polyurethane films for medical wearables

- 4.2.5 Thermal-management adhesives for modular electric vehicle battery packs

- 4.3 Market Restraints

- 4.3.1 Petro-feedstock price volatility

- 4.3.2 Tightening global VOC and hazard regulations

- 4.3.3 Fire-safety code upgrades for facade panels

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 Resin Type

- 5.1.1 Epoxy

- 5.1.2 Cyanoacrylate

- 5.1.3 Urethane

- 5.1.4 Silicones

- 5.1.5 Other Resin Types (Acrylic, Hot-Melt EVA, etc.)

- 5.2 Technology

- 5.2.1 Solvent-based

- 5.2.2 Water-based

- 5.3 End-user Industry

- 5.3.1 Automotive

- 5.3.2 Building and Construction

- 5.3.3 Electrical and Electronics

- 5.3.4 Medical

- 5.3.5 Packaging

- 5.3.6 Other End-user Industries (Renewable Energy, Consumer Goods, etc.)

- 5.4 Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corporation

- 6.4.4 BASF

- 6.4.5 Dow

- 6.4.6 Dymax

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG and Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 INTERTRONICS

- 6.4.11 Master Bond Inc.

- 6.4.12 Panacol-Elosol GmbH

- 6.4.13 Permabond LLC

- 6.4.14 Pidilite Industries Ltd.

- 6.4.15 Sika AG

- 6.4.16 Toyochem Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment