PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910466

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1910466

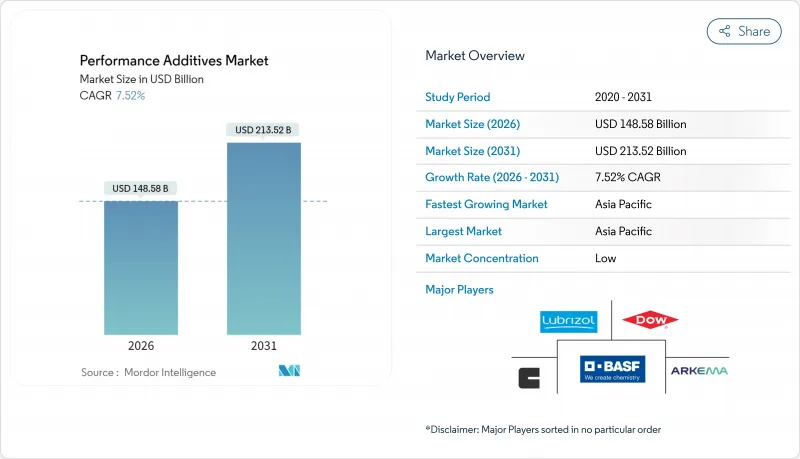

Performance Additives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Performance Additives market is expected to grow from USD 138.19 billion in 2025 to USD 148.58 billion in 2026 and is forecast to reach USD 213.52 billion by 2031 at 7.52% CAGR over 2026-2031.

Strong demand for specialty chemicals that boost durability, sustainability, and processing efficiency across plastics, lubricants, and coatings keeps the performance additives market on an expansion track. Growth tailwinds include accelerating automotive electrification, the global pivot toward waterborne low-VOC coatings, and intensified circular-economy policies that elevate additive-enabled chemical recycling solutions. Producers are also capitalizing on infrastructure programs in Asia-Pacific, where rapid industrialization supports both volume and value growth despite short-term cost pressure from volatile crude-derived feedstocks. Heightened requirements for flammability resistance, UV stability, and enhanced barrier properties further anchor the performance additives market as an essential enabler of modern materials solutions.

Global Performance Additives Market Trends and Insights

Replacement of Conventional Materials by Plastics Across End-Use Sectors

Demand for light, corrosion-resistant, and easily formable plastics displaces metals, wood, and glass across automotive, construction, and consumer-goods manufacturing. Each substitution requires thermal stabilizers, UV absorbers, and flame retardants that preserve performance under harsher operating envelopes. BASF's flame-retardant Ultramid polyphthalamide for high-voltage electric-vehicle components illustrates how advanced additives permit plastics to withstand temperature swings from -40 °C to 150 °C while meeting stringent dielectric thresholds. As plastics penetrate under-the-hood parts, exterior body panels, and modular building components, volume requirements for multi-functional additive packages climb in tandem, anchoring a long-run growth vector for the performance additives market.

Rapid Plastics Demand Growth in Emerging Economies

Urbanization, rising disposable incomes, and pervasive infrastructure programs are accelerating plastics consumption in Asia-Pacific and parts of Africa. Large-scale highway, rail, and housing projects demand geosynthetics, pipes, and insulation that rely on antioxidants, processing aids, and impact modifiers. In India, specialty-chemical producers are adding capacity to meet surging demand for construction additives that align with national cement output growing 6 to 8% annually. Similar momentum in Southeast Asia's consumer-packaging sector is stimulating imports of high-performance dispersants and slip agents. These dynamics solidify emerging regions as the principal volume engine of the performance additives market through 2030.

Stringent Restrictions on Single-Use Plastics and Hazardous Substances

Regulatory bans on selected additives in food contact and packaging push formulators toward costlier reformulations and eco-labels. California's 2027 prohibition on four legacy plastic additives in food packaging establishes a template for other jurisdictions. The European Union's 2025 update to food-contact regulations imposes tighter migration limits that force comprehensive portfolio audits. Companies like Clariant completed a phased elimination of PFAS from stabilizer ranges by December 2023. While these moves enhance environmental compliance, they introduce short-term cost spikes and qualification delays that shave growth points from the performance additives market.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Global Fuel-Economy and Emissions Norms

- Shift Toward Water-Borne and Low-VOC Coatings

- Volatile Crude-Derived Feedstock Prices

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Plastic additives commanded 42.62% of the performance additives market share in 2025, contributing the lion's share of revenue to the overall performance additives market. Their 9.18% CAGR through 2031 is propelled by dual imperatives: tighter flammability rules in electronics and the need for UV-stable lightweight parts in electric vehicles. Cutting-edge dispersants, antioxidants, and halogen-free flame retardants capture premium pricing as processors target weight savings without compromising strength.

Rubber additives uphold steady volumes in tire and conveyor-belt manufacturing, but growth lags plastics as mobility shifts to EV platforms that favor lightweight polymer composites. Paints and coatings additives enjoy a lift from waterborne migration, especially for biocide and rheology-control packages.

The Performance Additives Report is Segmented by Additive Category (Plastic Additives, Rubber Additives, Paints and Coatings Additives, Fuel Additives, and More), Form (Solid/Powder, Liquid, Masterbatch/Pellet, and Micro-Encapsulated), End-User Industry (Packaging, Automotive and Transportation, Building and Construction, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific retained a commanding 46.55% share of the performance additives market in 2025 and is forecast to lift revenues at an 8.31% CAGR to 2031. High public spending on rail, highways, and digital infrastructure multiplies demand for construction-grade dispersants, superplasticizers, and protective coatings.

North America exhibits moderate yet durable expansion underpinned by stringent fuel-economy standards and a growing preference for locally sourced specialty chemicals. Auto OEMs and aerospace primes leverage close collaboration with additive suppliers to meet lifecycle-carbon targets, sustaining premium margins for advanced dispersants and lubricity modifiers.

Europe navigates mixed macro conditions: energy-cost pressures curtailed chemical output in 2024, but policy leadership on climate and circularity nurtures new additive demand. Companies fast-track PFAS-free flame retardants and low-migration stabilizers to comply with the EU Chemicals Strategy for Sustainability.

Middle East and Africa, while still representing a smaller slice of the performance additives market size, register above-average growth in additives for infrastructure coatings, pipe resins, and lubricant basestocks. Hydrocarbon feedstock availability positions Gulf Cooperation Council members to expand backward-integrated additive lines, while sub-Saharan Africa's urbanization lifts demand for weather-resistant paints and packaging.

- Afton Chemical

- Akzo Nobel N.V.

- Albemarle Corporation

- Arkema

- Ashland

- Baerlocher GmbH

- BASF

- Chevron Oronite Company LLC

- Clariant

- Dow

- Eastman Chemical Company

- Evonik Industries AG

- Exxon Mobil Corporation

- Honeywell International Inc.

- Huntsman International LLC

- Lanxess

- Mitsui & Co. (Asia Pacific) Pte. Ltd.

- Performance Additives

- Songwon

- The Lubrizol Corporation

- Univar Solutions LLC

- W. R. Grace & Co

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Replacement of Conventional Materials by Plastics Across End-Use Sectors

- 4.2.2 Rapid Plastics Demand Growth in Emerging Economies

- 4.2.3 Tightening Global Fuel-Economy and Emissions Norms Driving High-Performance Lubricant and Fuel Additives

- 4.2.4 Shift Toward Water-Borne and Low-VOC Coatings Boosts Specialty Additive Uptake

- 4.2.5 Additive-Enabled Chemical-Recycling and Circular-Polymer Initiatives Gain Traction

- 4.3 Market Restraints

- 4.3.1 Stringent Restrictions on Single-Use Plastics and Hazardous Substances

- 4.3.2 Volatile Crude-Derived Feedstock Prices

- 4.3.3 Pending Micro-Plastics Legislation Targeting Functional Additives in Packaging

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Additive Category

- 5.1.1 Plastic Additives

- 5.1.1.1 Lubricants

- 5.1.1.2 Processing Aids (Fluoropolymer-based)

- 5.1.1.3 Flow Improvers

- 5.1.1.4 Slip Additives

- 5.1.1.5 Antistatic Additives

- 5.1.1.6 Pigment Wetting Agents

- 5.1.1.7 Filler Dispersants

- 5.1.1.8 Antifog Additives

- 5.1.1.9 Plasticizers

- 5.1.1.10 Stabilizers

- 5.1.1.11 Flame Retardants

- 5.1.1.12 Impact Modifiers

- 5.1.2 Rubber Additives

- 5.1.2.1 Accelerators

- 5.1.2.2 Antidegradants

- 5.1.2.3 Blowing and Adhesive Agents

- 5.1.3 Paints and Coatings Additives

- 5.1.3.1 Biocides

- 5.1.3.2 Dispersants and Wetting Agents

- 5.1.3.3 Defoamers and De-aerators

- 5.1.3.4 Rheology Modifiers

- 5.1.3.5 Surface Modifiers

- 5.1.3.6 Stabilizers

- 5.1.3.7 Flow and Leveling Additives

- 5.1.3.8 Other Paint and Coating Additives

- 5.1.4 Fuel Additives

- 5.1.4.1 Deposit Control

- 5.1.4.2 Cetane Improvers

- 5.1.4.3 Lubricity Improvers

- 5.1.4.4 Antioxidants

- 5.1.4.5 Anticorrosion

- 5.1.4.6 Fuel Dyes

- 5.1.4.7 Cold-Flow Improvers

- 5.1.4.8 Antiknock Agents

- 5.1.4.9 Other Fuel Additives

- 5.1.5 Ink Additives

- 5.1.5.1 Rheology Modifiers

- 5.1.5.2 Slip / Rub Agents

- 5.1.5.3 Defoamers

- 5.1.5.4 Dispersants

- 5.1.5.5 Antioxidants

- 5.1.5.6 Chelating Agents

- 5.1.5.7 Other Ink Additives

- 5.1.6 Leather Additives

- 5.1.6.1 Finishing Agents

- 5.1.6.2 Fat Liquors

- 5.1.6.3 Syntans

- 5.1.6.4 Other Leather Additives

- 5.1.7 Lubricant Additives

- 5.1.7.1 Dispersants and Emulsifiers

- 5.1.7.2 Viscosity-Index Improvers

- 5.1.7.3 Detergents

- 5.1.7.4 Corrosion Inhibitors

- 5.1.7.5 Oxidation Inhibitors

- 5.1.7.6 Extreme-Pressure Additives

- 5.1.7.7 Friction Modifiers

- 5.1.7.8 Other Lubricant Additives

- 5.1.8 Adhesives and Sealants Additives

- 5.1.8.1 Antioxidants

- 5.1.8.2 Light Stabilizers

- 5.1.8.3 Tackifiers

- 5.1.8.4 Other Additives

- 5.1.1 Plastic Additives

- 5.2 By Form

- 5.2.1 Solid / Powder

- 5.2.2 Liquid

- 5.2.3 Masterbatch / Pellet

- 5.2.4 Micro-encapsulated

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Automotive and Transportation

- 5.3.3 Building and Construction

- 5.3.4 Electrical and Electronics

- 5.3.5 Industrial Machinery

- 5.3.6 Consumer Goods

- 5.3.7 Energy and Power (incl. Oil and Gas)

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 Japan

- 5.4.1.3 India

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Afton Chemical

- 6.4.2 Akzo Nobel N.V.

- 6.4.3 Albemarle Corporation

- 6.4.4 Arkema

- 6.4.5 Ashland

- 6.4.6 Baerlocher GmbH

- 6.4.7 BASF

- 6.4.8 Chevron Oronite Company LLC

- 6.4.9 Clariant

- 6.4.10 Dow

- 6.4.11 Eastman Chemical Company

- 6.4.12 Evonik Industries AG

- 6.4.13 Exxon Mobil Corporation

- 6.4.14 Honeywell International Inc.

- 6.4.15 Huntsman International LLC

- 6.4.16 Lanxess

- 6.4.17 Mitsui & Co. (Asia Pacific) Pte. Ltd.

- 6.4.18 Performance Additives

- 6.4.19 Songwon

- 6.4.20 The Lubrizol Corporation

- 6.4.21 Univar Solutions LLC

- 6.4.22 W. R. Grace & Co

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment