PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846148

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846148

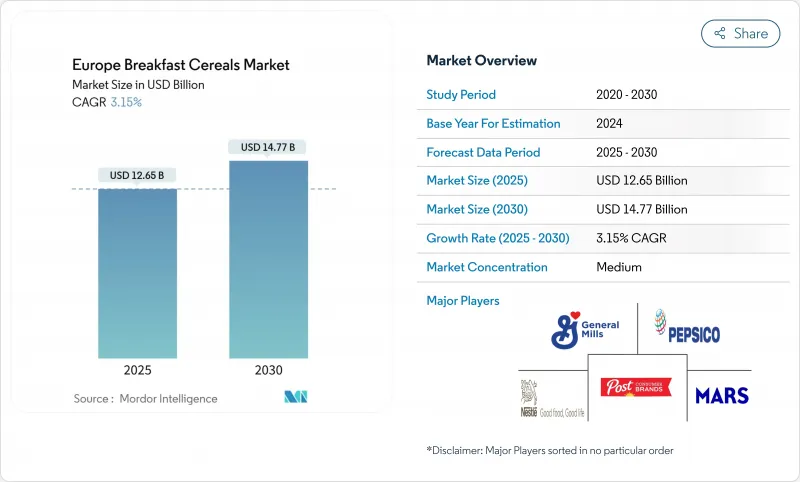

Europe Breakfast Cereals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Europe Breakfast Cereals market size, valued at USD 12.65 billion market size in 2025, is expected to reach USD 14.77 billion by 2030, growing at a CAGR of 3.15% during the forecast period (2025-2030).

The market expansion is primarily driven by increasing consumer preference for convenient and nutritious breakfast options, supported by busy lifestyles and the growing trend of on-the-go breakfast consumption. Ready-to-eat cereals dominate the market share, while hot cereals maintain steady demand, particularly in colder regions. Manufacturers are adapting to significant market shifts by focusing on health-oriented formulations and addressing supply chain challenges. Regulatory scrutiny of sugar content and acrylamide levels has prompted established players to reformulate products, creating opportunities for competitors offering products with improved nutritional profiles. Major manufacturers are introducing organic, gluten-free, and high-fiber variants to meet evolving consumer preferences. The market also experiences increased demand for private-label products, particularly in Western European countries. Additionally, the rising adoption of premium breakfast cereals and growing consumer interest in ancient grains and superfoods are creating new market opportunities.

Europe Breakfast Cereals Market Trends and Insights

Rising Demand for High-Protein Cereal Variants Among Consumers

Consumer preference for protein-enriched breakfast cereals is driving significant trans-formation in the European market. The trend has expanded beyond fitness enthusiasts to include mainstream consumers seeking sustained energy and satiety. The rising health consciousness among European consumers, combined with growing awareness of pro-tein's role in maintaining a balanced diet, has prompted manufacturers to develop pro-tein-enriched breakfast cereals. Consumers are increasingly selecting cereals fortified with protein sources such as quinoa, chia seeds, and various grains to support their fit-ness goals and maintain energy levels throughout the day. In response, major manufac-turers like Kellanova and Crispy Fantasy have expanded their product portfolios to include protein-rich options, incorporating ingredients such as nuts, seeds, and plant-based pro-teins. This shift aligns with the broader movement toward functional foods in the European market. The increasing focus on protein enrichment has intensified competition for quali-ty protein sources, driving manufacturers to invest in ingredient innovation and supply chain optimization.

Growing Penetration of Gluten-Free Grains Expanding Multi-Grain Cereals

The gluten-free breakfast cereals market has evolved beyond its initial focus on celiac disease patients. Consumer demand is driven by both medical requirements and lifestyle preferences, with a growing perception of gluten-free products as healthier options. Companies such as General Mills and Surreal are incorporating alternative grains like quinoa, amaranth, buckwheat, and millets into their products. For instance, General Mills offers Strawberry Vanilla Chex which is a gluten-free breakfast cereal. These cereals offer gluten-free content while maintaing unique textures and flavors. European dietitians recommend gluten-free oats and quinoa for their nutritional value and accessibility, though many alternative cereals remain unexplored despite their health benefits. The multi-grain breakfast cereals market is growing as consumers seek varied nutritional benefits from combined grain sources. The European Food Safety Authority reported in 2023 that celiac disease affects approximately 0.7% of the EU population. Manufacturers are focusing on research and development to enhance product quality while streamlining production processes to reduce costs, as gluten-free products currently sell at twice the price of traditional alternatives.

Volatile Oat and Corn Commodity Prices Compressing Margins

Price volatility in key cereal ingredients, particularly corn and oats, presents significant challenges. The interconnected nature of agricultural commodities means price fluctuations in one crop rapidly affect others, creating systemic pricing challenges. This volatility has intensified due to multiple factors, including geopolitical tensions, US (United States) tariffs on grains and oilseeds, and currency fluctuations, especially the dollar-euro exchange rate. Manufacturers face difficult decisions between absorbing additional costs or implementing price increases, which can affect consumer purchasing behavior. These challenges are particularly acute for premium and health-focused cereal producers, where maintaining high ingredient quality is essential. Supply chain disruptions and weather-related events, such as poor harvests and reduced crop yields in key European agricultural regions, further compound these issues, creating uncertainty in production planning and inventory management. Additionally, manufacturers struggle to maintain long-term contracts with suppliers at fixed prices during periods of high price volatility, directly impacting their production expenses and profit margins.

Other drivers and restraints analyzed in the detailed report include:

- Working Professionals Seeking Convenient and Quick Breakfast Options

- Rise of Online Grocery Platforms Enhances Accessibility and Fuels Demand

- Regulatory Sugar Scrutiny Increasing Reformulation Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Ready-to-Eat (RTE) cereals maintain a 79.05% market share in Europe in 2024, driven by established consumer preferences and convenience. Ready-to-Cook (RTC) cereals demonstrate significant growth potential, with a projected CAGR of 5.12% through 2030, surpassing the market average by more than double. This expansion reflects consumers' increasing preference for hot breakfast options, which they perceive as less processed and more nutritious. Hot oatmeal dominates the RTC segment due to its recognized heart-health benefits and versatility with various toppings, including nuts, seeds, and fruits. Studies show that oat-based hot cereals provide sustained energy and improved satiety compared to RTE alternatives.

Muesli and porridge mixes show growth through premium variants and functional ingredients, while flakes constitute the largest RTE sub-segment due to production efficiency and established brand recognition. Puffed cereals and granola clusters expand their market presence through unique textures and versatile consumption occasions beyond breakfast. Manufacturers incorporate fruits and vegetables into cereal formulations to enhance nutritional content and taste profiles, addressing consumer demands for lower sugar content and improved nutritional value. This development highlights market opportunities for products that combine traditional cereal formats with enhanced nutritional benefits.

Oat-based cereals dominate with a 34.55% market share in 2024, supported by their health benefits and versatility in ready-to-eat (RTE) and ready-to-cook (RTC) formats. The ingredient's benefits for heart health, energy provision, and digestive wellness match European consumer preferences. Rice-based cereals show the strongest growth trajectory, with a projected CAGR of 4.35% through 2030, driven by their gluten-free nature and neutral taste that accommodates diverse flavors and functional additives. Manufacturers are increasingly investing in oat and rice processing facilities to meet the rising demand and ensure consistent supply.

Wheat remains a core ingredient despite gluten concerns, while corn usage faces headwinds from price volatility and processed food perceptions. Barley's presence is growing due to its nutritional value and environmental benefits, though primarily in premium muesli and granola segments. Minor cereals, including quinoa, amaranth, and teff, are increasingly incorporated into multi-grain products. This ingredient diversification reflects both consumer interest in varied nutrition sources and manufacturers' efforts to strengthen supply chain resilience. The market is witnessing a surge in research and development activities focused on improving the nutritional profile and processing efficiency of alternative grains.

The Europe Breakfast Cereals Market is Segmented by Type (Ready-To-Eat Cereals and Ready-To-Cook Cereals), Ingredient Source (Wheat, Corn, Oats, Rice, Barley, and Others), Packaging Type (Boxes, Stand-Up Pouches, and More), Distribution Channel (Supermarkets/Hypermarkets, Convenience/Grocery Stores, and More), Age Group (Adults and Children), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Mars, Incorporated

- Nestle S.A.

- General Mills, Inc.

- Post Consumer Brands LLC

- PepsiCo Inc,

- Associated British Foods plc

- Barilla Group

- Sanitarium(The Health Food Company)

- Alnatura Production and Trading GmbH

- Oddlygood (Rude Health)

- Katjesgreenfood GmbH & Co. KG(MyMuseli Gmbh)

- Verival Bio GmbH

- The Oetker Group

- Oy Karl Fazer Ab.(Fazer Group)

- H&J Bruggen KG

- Raiso Group

- Bio-Familia AG

- Hero Group

- Almaverde Bio Italia

- Eco United (Vita Bella)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for High-Protein Cereal Variants Among Consumers

- 4.2.2 Surge in Single-Serve Breakfast Habits Fueling On-the-Go Cereal Cups

- 4.2.3 Growing Penetration of Gluten-Free Grains Expanding Multi-Grain Cereals

- 4.2.4 Rise of Online Grocery Platforms Enhances Accessibility and Fuels Demand

- 4.2.5 Working Professionals Seeking Convenient and Quick Breakfast Options

- 4.2.6 Product Innovation and Variety Cater to Diverse Dietary Needs

- 4.3 Market Restraints

- 4.3.1 Volatile Oat and Corn Commodity Prices Compressing Margins

- 4.3.2 Regulatory sugar scrutiny increasing reformulation costs

- 4.3.3 Consumer Perception of Processed Foods

- 4.3.4 Competition From Protein Bars and RTD (Ready-To-Drink) Breakfast Beverages

- 4.4 Consumer Behaviour Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Ready-to-Eat Cereals

- 5.1.1.1 Flakes

- 5.1.1.2 Puffed Cereals

- 5.1.1.3 Granola and Clusters

- 5.1.1.4 Others

- 5.1.2 Ready-to-Cook Cereals

- 5.1.2.1 Hot Oatmeal

- 5.1.2.2 Muesli and Porridge Mixes

- 5.1.2.3 Other Ready-to-Cook Cereals

- 5.1.1 Ready-to-Eat Cereals

- 5.2 By Ingredient Source

- 5.2.1 Wheat

- 5.2.2 Corn

- 5.2.3 Oats

- 5.2.4 Rice

- 5.2.5 Barley

- 5.2.6 Others

- 5.3 By Packaging Type

- 5.3.1 Boxes

- 5.3.2 Stand-Up Pouches

- 5.3.3 Cups and Bowls

- 5.3.4 Others

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Convenience/Grocery Stores

- 5.4.3 Specialty Stores

- 5.4.4 Online Retailers

- 5.4.5 Other Distribution Channels

- 5.5 By Age Group

- 5.5.1 Adults

- 5.5.2 Children

- 5.6 By Geography

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Russia

- 5.6.7 Sweden

- 5.6.8 Norway

- 5.6.9 Denmark

- 5.6.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Mars, Incorporated

- 6.4.2 Nestle S.A.

- 6.4.3 General Mills, Inc.

- 6.4.4 Post Consumer Brands LLC

- 6.4.5 PepsiCo Inc,

- 6.4.6 Associated British Foods plc

- 6.4.7 Barilla Group

- 6.4.8 Sanitarium(The Health Food Company)

- 6.4.9 Alnatura Production and Trading GmbH

- 6.4.10 Oddlygood (Rude Health)

- 6.4.11 Katjesgreenfood GmbH & Co. KG(MyMuseli Gmbh)

- 6.4.12 Verival Bio GmbH

- 6.4.13 The Oetker Group

- 6.4.14 Oy Karl Fazer Ab.(Fazer Group)

- 6.4.15 H&J Bruggen KG

- 6.4.16 Raiso Group

- 6.4.17 Bio-Familia AG

- 6.4.18 Hero Group

- 6.4.19 Almaverde Bio Italia

- 6.4.20 Eco United (Vita Bella)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK