PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846160

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846160

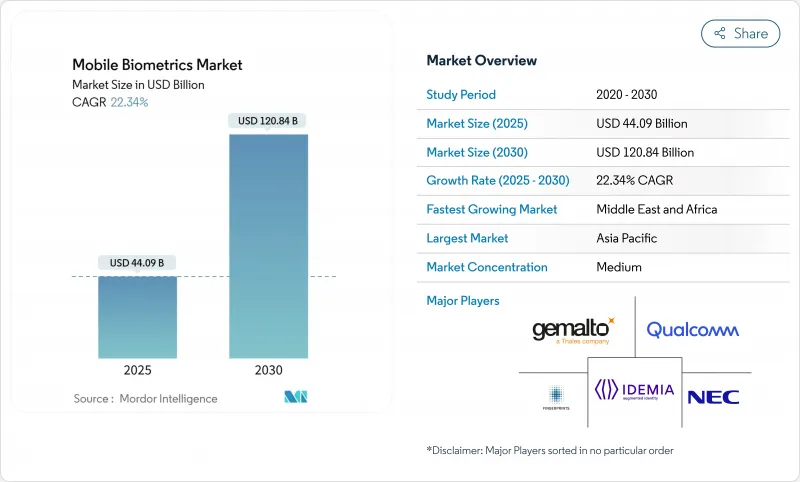

Mobile Biometrics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The mobile biometric market size is valued at USD 44.09 billion in 2025 and is forecast to expand to USD 120.84 billion by 2030, translating into a robust 22.34% CAGR.

Momentum stems from the convergence of 5G connectivity, on-device AI processing, and tighter digital-identity mandates across emerging economies. Continuous behavioral monitoring is gaining favor over static checks as presentation-attack attempts on entry-level Android phones escalate. Component trends is giving way to services that are advancing as organizations migrate toward cloud-based biometric platforms. Fingerprint sensors illustrating a maturing core and an innovation frontier in new modalities. Device demand is dominated by smartphones, but smart wearables are setting the pace, signaling a pivot toward ambient, always-on authentication environments.

Global Mobile Biometrics Market Trends and Insights

Bi-modal authentication surge in India's UPI ecosystem

India's Unified Payments Interface is enabling fingerprint or facial recognition in lieu of PINs, cutting fraud and speeding micro-transactions. The model is already influencing wallet providers across Southeast Asia and could lift mobile biometric market adoption among unbanked consumers. Banks benefit from reduced chargeback costs, yet privacy regulators continue to scrutinize Aadhaar-linked storage practices.

5G-enabled on-device AI improving spoof detection in Chinese OEM smartphones

Chinese handset makers have embedded AI models that detect deep-fake attempts locally, a timely response after a 40% jump in biometric fraud in 2024. The hardware-software bundle raises the bar for global competitors and underpins premium positioning while preserving battery life.

High presentation-attack rates on low-cost Android devices

Budget phones often lack robust liveness checks, allowing deep-fake audio or masks to bypass sensors 99% of the time in six attempts. The gap erodes user trust and forces banks in Africa to add physical ID reviews, dampening scale in price-sensitive segments.

Other drivers and restraints analyzed in the detailed report include:

- e-KYC mandates for mobile banking in Nigeria and Brazil

- European Digital Identity Wallet regulation accelerating biometric passports on phones

- Restrictive data-sovereignty laws limiting cloud voice biometrics in the EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The mobile biometric market size for hardware stood at USD 26.53 billion in 2024, equal to 60.2% revenue share. Sensor makers invested in under-display ultrasonic modules to defend margins as commoditization sets. AI-optimized chips compress latency, ensuring usability in low-light and wet-finger scenarios. Services, though smaller, are compounding at 23.3% CAGR on the back of identity-as-a-service subscriptions purchased by banks and hospitals. Providers bundle orchestration dashboards, fraud-risk analytics, and compliance reporting, shifting capital expense to operating outlays.

Demand for managed services is most pronounced in healthcare, where hospitals outsource biometric patient enrollment to avoid running data centers. Leading IaaS players co-market biometric APIs, broadening reach. Meanwhile, software platforms that unify fingerprint, voice, and behavioral signals hold strategic ground as integrators of record for multicloud deployments. Collectively, these forces reinforce a services flywheel that drives stickier annual recurring revenue across the mobile biometric market.

Single-factor techniques generated USD 31.47 billion in 2024, underscoring user preference for one-touch unlock flows embedded natively in iOS and Android. However, regulators and insurers now pressure banks to shrink residual fraud, steering new budget line items toward multi-factor deployments that mix biometrics with device-based cryptographic keys.

Android 15's passkey integration proves critical; by caching FIDO credentials in the hardware enclave, Google enables face or fingerprint to act as a second factor invisibly to users. Enterprises gain defense-in-depth without abandonment mobile checkout flows. Expect board-level risk committees to prioritize such layered controls as phishing kits that weaponize generative AI.

The Mobile Biometric Market Report is Segmented by Component (Hardware, Software Platforms, Services), Authentication Mode (Single-Factor Authentication, and More), Technology/Modality (Fingerprint Recognition, Facial Recognition, and More), Device Type (Smartphones, Tablets, and More), Industry Vertical (BFSI, Government and Public Sector, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated USD 19.79 billion in 2024, equating to 44.8% of global revenue. Rapid smartphone penetration, proliferating fintech apps, and government-backed digital ID programs sustain region-leading scale. Chinese OEMs' embrace of ultrasonic in-display sensors has rippled across supply chains, lowering BOM costs and seeding mass adoption. India continues to iterate on Aadhaar-linked rails, with bi-modal UPI transactions expanding merchant acceptance beyond metro centers.

The Middle East, at USD 2.85 billion in 2024, is the fastest-growing pocket with a 24.2% CAGR. UAE's replacement of physical Emirates IDs with mobile credentials exemplifies a top-down policy play that accelerates nationwide interoperability. Kuwait's Vision 2035 ties biometric enrollment to e-government service access, lifting demand for multimodal kits. Dubai's infrastructure boom, including transit megaprojects, compels contractors to adopt biometric access control, further lifting regional outlays.

North America maintains steady but slower growth as enterprises modernize IAM stacks and consumer banking shifts toward password-free sign-in. JPMorgan Chase's biometric checkout pilots hint at a coming inflection in card-less retail payments. Europe remains structurally attractive but navigates stringent GDPR and AI Act requirements. The EU Digital Identity Wallet harmonizes standards across 10 nations, catalyzing vendor certification pipelines. Sub-Saharan Africa, while smaller in dollar terms, drives volume in mobile voter-registration kits, underscoring latent demand for portable enrollment hardware.

- Apple Inc.

- Samsung Electronics Co. Ltd.

- Qualcomm Technologies Inc.

- IDEMIA (Safran Identity and Security)

- NEC Corporation

- Thales Group (Gemalto)

- Fingerprint Cards AB

- Goodix Technology Co. Ltd.

- Synaptics Incorporated

- Precise Biometrics AB

- Nuance Communications Inc.

- Aware Inc.

- Daon Inc.

- M2SYS Technology

- Veridium Ltd.

- FaceTec Inc.

- Mobbeel Solutions SLL

- VoiceVault Inc.

- ValidSoft Ltd.

- Tech5 SA

- HYPR Corp.

- Suprema Inc.

- ID RandD Inc.

- ImageWare Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Bi-modal authentication surge in India's Unified Payments Interface (UPI) ecosystem

- 4.2.2 5G-enabled on-device AI improving spoof detection in Chinese OEM smartphones

- 4.2.3 e-KYC mandates for mobile banking in Nigeria, Brazil and Indonesia

- 4.2.4 Deployment of mobile biometric voter enrolment kits across Sub-Saharan Africa

- 4.2.5 European Digital Identity Wallet regulation accelerating biometric passport use on phones

- 4.2.6 OEM shift toward under-display ultrasonic sensors in premium segment

- 4.3 Market Restraints

- 4.3.1 High presentation-attack rates on low-cost Android devices

- 4.3.2 Restrictive data-sovereignty laws limiting cloud-based voice biometrics in EU

- 4.3.3 Battery-drain concerns for continuous behavioral authentication

- 4.3.4 Absence of universal mobile biometric performance benchmarks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software Platforms

- 5.1.3 Services

- 5.2 By Authentication Mode

- 5.2.1 Single-Factor Authentication

- 5.2.2 Multi-Factor Authentication

- 5.3 By Technology / Modality

- 5.3.1 Fingerprint Recognition

- 5.3.2 Facial Recognition

- 5.3.3 Voice Recognition

- 5.3.4 Iris Recognition

- 5.3.5 Vein and Vascular Pattern Recognition

- 5.3.6 Behavioral Biometrics (Gait, Keystroke)

- 5.3.7 Other Modalities

- 5.4 By Device Type

- 5.4.1 Smartphones

- 5.4.2 Tablets

- 5.4.3 Smart Wearables

- 5.4.4 IoT / Edge Devices

- 5.4.5 Rugged Handhelds and Scanners

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Government and Public Sector

- 5.5.3 Healthcare

- 5.5.4 Retail and E-commerce

- 5.5.5 IT and Telecom

- 5.5.6 Defense and Security

- 5.5.7 Education

- 5.5.8 Other Verticals

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 South Korea

- 5.6.4.4 India

- 5.6.4.5 Australia

- 5.6.4.6 New Zealand

- 5.6.4.7 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Kenya

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Apple Inc.

- 6.4.2 Samsung Electronics Co. Ltd.

- 6.4.3 Qualcomm Technologies Inc.

- 6.4.4 IDEMIA (Safran Identity and Security)

- 6.4.5 NEC Corporation

- 6.4.6 Thales Group (Gemalto)

- 6.4.7 Fingerprint Cards AB

- 6.4.8 Goodix Technology Co. Ltd.

- 6.4.9 Synaptics Incorporated

- 6.4.10 Precise Biometrics AB

- 6.4.11 Nuance Communications Inc.

- 6.4.12 Aware Inc.

- 6.4.13 Daon Inc.

- 6.4.14 M2SYS Technology

- 6.4.15 Veridium Ltd.

- 6.4.16 FaceTec Inc.

- 6.4.17 Mobbeel Solutions SLL

- 6.4.18 VoiceVault Inc.

- 6.4.19 ValidSoft Ltd.

- 6.4.20 Tech5 SA

- 6.4.21 HYPR Corp.

- 6.4.22 Suprema Inc.

- 6.4.23 ID RandD Inc.

- 6.4.24 ImageWare Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment