PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846218

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846218

Infrared Detector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

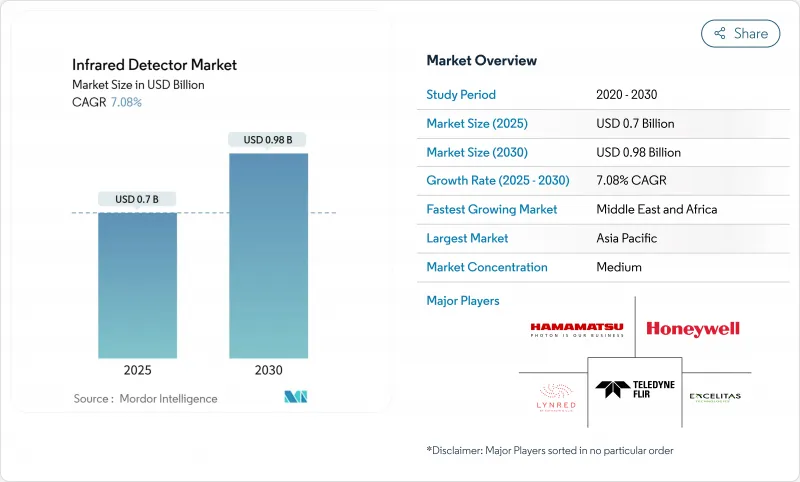

The infrared detector market size is currently valued at USD 0.70 billion and is projected to reach USD 0.98 billion by 2030, advancing at a 7.08% CAGR.

Miniaturized uncooled microbolometer arrays, LiDAR-grade near-infrared sensors for autonomous vehicles, and mandatory predictive-maintenance thermography in the European Union underpin near-term momentum. Wider deployment of infrared gas-leak detection systems in green-hydrogen plants, expanding semiconductor inspection demand in East Asia, and defense-driven appetite for higher-sensitivity cooled arrays further reinforce the growth trajectory. Supply-chain realignment away from restricted gallium and germanium sources is accelerating substitutions in detector materials while acquisition-led consolidation is shaping competitive strategies across value-chain tiers. The interplay of these dynamics positions the infrared detector market for sustained expansion and technology diversification.

Global Infrared Detector Market Trends and Insights

Miniaturisation of Uncooled Micro-bolometer Arrays Empowering IoT Motion Sensors in Asia

Aalto University's germanium-based photodiodes raised responsivity by 35% at 1.55 μm, enabling cost-effective CMOS-compatible fabrication that tackles thermal drift while sustaining sub-milliwatt power envelopes.MEMS convergence with lightweight signal-processing logic is pushing continuous thermal monitoring into smart-building endpoints, and Asian component makers are bundling wireless connectivity to monetise value-added services across consumer electronics portfolios.

Mandatory Predictive-Maintenance Thermography in EU Process Industries

The 2024 EU machinery regulation codifies risk-assessment protocols that make thermal imaging integral to compliance validation. Condition-based monitoring reduces downtime that can exceed USD 100,000 per hour in energy-intensive plants, and AI-enabled analytics now automate anomaly detection, easing skills constraints and strengthening investment cases.

Export-Control Limits on High-Spec Cooled Detectors

ITAR and Wassenaar regimes constrain 60% of camera exports that contain US-origin subsystems, forcing dual product lines that elevate fixed costs. European manufacturers are localising supply chains, yet geopolitical tensions around gallium and germanium amplify timeline risks.

Other drivers and restraints analyzed in the detailed report include:

- Surge in LiDAR-grade Near-Infrared Detectors for Autonomous & EV Platforms in China

- IR Gas-Leak Detection Mandates for Green-Hydrogen Plants across Middle East

- Price Erosion in Passive PIR Components

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, thermal detectors captured 65% of the infrared detector market. Photo- or quantum-based devices are, however, expanding at an 8.5% CAGR as defense and scientific use cases favor higher sensitivity. The infrared detector market size for quantum detectors is forecast to widen as organic semiconductor photodetectors demonstrated specific detectivity of 5.55X1012 Jones without pixel-level patterning, signaling lower fabrication overheads.

Thermal detectors still dominate consumer and building-automation applications due to uncooled operation and lower upfront costs. AI-enabled on-chip processing inside quantum arrays is now providing real-time threat classification for military inventories, a shift likely to recalibrate procurement strategies. KAIST's room-temperature mid-infrared photodetector removes cryogenic barriers, positioning quantum architectures for handheld and battery-operated platforms.

Uncooled arrays delivered 78% of 2024 revenue as designers prized low power and simple integration. Yet cooled architectures are advancing at 8.2% CAGR tied to defense programs that demand extreme range. Lynred's ATI320 underscores the push to elevate uncooled sensitivity, blurring historical performance lines.

The military segment, nearly 60% of the total infrared detector market size, still specifies cooled formats for anti-ship and long-range targeting optics. Size, weight, and power optimisation is making Stirling-cooler packages suitable for drones and portable launchers. Hybrid payloads that combine cooled and uncooled modules are emerging, allowing unit commanders to balance cost and mission profiles.

The Infrared Detector Market is Segmented by Detector Type (Thermal Detector, Photo Detector), Cooling Technology (Uncooled, Cooled), Material (Microbolometer, Ingaas, and More), Spectral Range (NIR, SWIR, and More), Application (Motion Sensing, Thermography, Process Monitoring, and More), End-Use Industry (Aerospace and Defense, Industrial, and More), and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific commanded 42% of 2024 spending as Chinese EV makers scaled LiDAR rollouts and foundries in Taiwan and South Korea ramped SWIR inspection lines. Patent leadership by local LiDAR firms emphasises regional innovation depth, and proximity to end-use clusters shortens supply chains. Japan's mature electronics sector supplies advanced packaging services, and India's border-security investments boost high-sensitivity cooled demand.

North America leverages strong defense budgets and proprietary sensor IP, with Teledyne recording USD 1,502.3 million Q4 2024 sales that underline sustained procurement cycles. ITAR provisions shield domestic vendors yet complicate exports, prompting regional diversification strategies among international buyers. Canada and Mexico support the automotive and extractive verticals where thermal cameras enhance operational resilience.

Europe grows steadily under machinery-safety regulations and environmental directives that embed thermography into compliance audits. Lynred's EUR 85 million (USD 91 million) facility expansion evidences capacity localisation aimed at de-risking supply lines. Nordic nations champion smart-building deployments, while the Middle East and Africa forecast 8.9% CAGR on the back of green-hydrogen megaprojects and security infrastructure upgrades that specify long-range imagers.

- Teledyne FLIR

- Lynred (ULIS + Sofradir)

- Hamamatsu Photonics

- Excelitas Technologies

- Honeywell International

- Murata Manufacturing

- Texas Instruments

- Omron Corporation

- Raytheon Technologies

- Leonardo DRS

- SCD - SemiConductor Devices

- BAE Systems plc

- L3Harris Technologies

- InfraTec GmbH

- iRay Technology

- Hikmicro (Hangzhou)

- Guide Sensmart (Wuhan Guide)

- DALI Technology

- InfraTec GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Deliverables

- 1.2 Study Assumptions

- 1.3 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Miniaturisation of Uncooled Micro-bolometer Arrays Empowering IoT Motion Sensors in Asia

- 4.2.2 Mandatory Predictive-Maintenance Thermography in EU Process Industries

- 4.2.3 Surge in LiDAR-grade Near-IR Detectors for Autonomous and EV Platforms in China

- 4.2.4 IR Gas-Leak Detection Mandates for Green-Hydrogen Plants across Middle East

- 4.2.5 Semiconductor Fab Inspection Demand for SWIR Cameras in Taiwan and South Korea

- 4.2.6 Border-Surveillance Modernisation Programs in US and India

- 4.3 Market Restraints

- 4.3.1 Export-control (ITAR-like) Limits on High-spec Cooled Detectors

- 4.3.2 Price Erosion in Passive PIR Components

- 4.3.3 Thermal Drift and Calibration Issues in Offshore Oil-and-Gas Deployment

- 4.3.4 Counterfeit Detector Channels in Emerging Markets

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Detector Type

- 5.1.1 Thermal Detector

- 5.1.2 Photo (Quantum) Detector

- 5.2 By Cooling Technology

- 5.2.1 Uncooled Infrared Detector

- 5.2.2 Cooled Infrared Detector

- 5.3 By Material

- 5.3.1 Microbolometer

- 5.3.2 InGaAs (Indium Gallium Arsenide)

- 5.3.3 MCT (Mercury Cadmium Telluride)

- 5.3.4 Pyroelectric

- 5.3.5 Thermopile

- 5.4 By Spectral Range

- 5.4.1 Near-Wave Infrared (NIR)

- 5.4.2 Short-Wave Infrared (SWIR)

- 5.4.3 Mid-Wave Infrared (MWIR)

- 5.4.4 Long-Wave Infrared (LWIR)

- 5.4.5 Far-Infrared (FIR)

- 5.5 By Application

- 5.5.1 People and Motion Sensing

- 5.5.2 Temperature Measurement / Thermography

- 5.5.3 Industrial Process Monitoring

- 5.5.4 Spectroscopy and Biomedical Imaging

- 5.5.5 Fire and Gas Detection

- 5.5.6 Automotive ADAS and LiDAR

- 5.5.7 Environmental and Agriculture Monitoring

- 5.5.8 Other Applications (Building and HVAC Automation, Smart Homes, Military and Defense, and others)

- 5.6 By End-Use Industry

- 5.6.1 Aerospace and Defense

- 5.6.2 Industrial Manufacturing

- 5.6.3 Automotive

- 5.6.4 Oil, Gas and Energy

- 5.6.5 Healthcare and Life Sciences

- 5.6.6 Consumer Electronics

- 5.6.7 Smart Infrastructure

- 5.6.8 Others

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Nordics

- 5.7.3.6 Rest of Europe

- 5.7.4 Asia Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 India

- 5.7.4.4 South Korea

- 5.7.4.5 Taiwan

- 5.7.4.6 Australia

- 5.7.4.7 New Zealand

- 5.7.4.8 Rest of Asia Pacific

- 5.7.5 Middle East and Africa

- 5.7.5.1 Middle East

- 5.7.5.1.1 Saudi Arabia

- 5.7.5.1.2 UAE

- 5.7.5.1.3 Turkey

- 5.7.5.1.4 Rest of Middle East

- 5.7.5.2 Africa

- 5.7.5.2.1 South Africa

- 5.7.5.2.2 Egypt

- 5.7.5.2.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Teledyne FLIR

- 6.4.2 Lynred (ULIS + Sofradir)

- 6.4.3 Hamamatsu Photonics

- 6.4.4 Excelitas Technologies

- 6.4.5 Honeywell International

- 6.4.6 Murata Manufacturing

- 6.4.7 Texas Instruments

- 6.4.8 Omron Corporation

- 6.4.9 Raytheon Technologies

- 6.4.10 Leonardo DRS

- 6.4.11 SCD - SemiConductor Devices

- 6.4.12 BAE Systems plc

- 6.4.13 L3Harris Technologies

- 6.4.14 InfraTec GmbH

- 6.4.15 iRay Technology

- 6.4.16 Hikmicro (Hangzhou)

- 6.4.17 Guide Sensmart (Wuhan Guide)

- 6.4.18 DALI Technology

- 6.4.19 InfraTec GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment