PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846260

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1846260

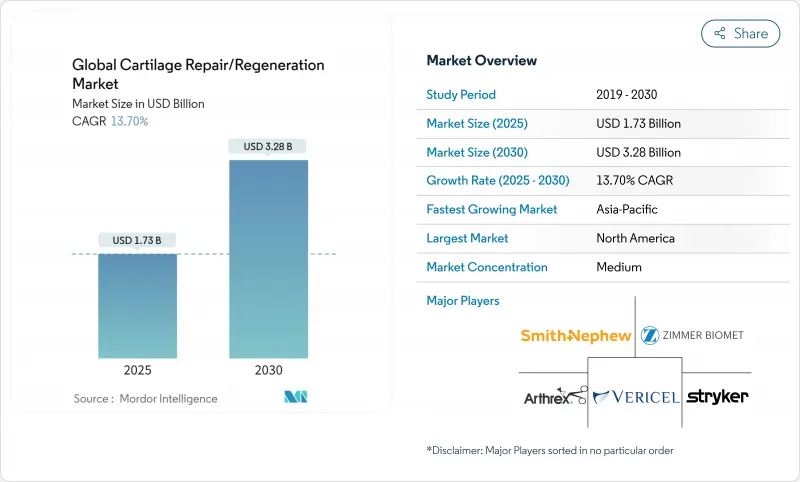

Global Cartilage Repair/Regeneration - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The cartilage repair market is valued at USD 1.73 billion in 2025 and is on course to reach USD 3.28 billion by 2030, translating into a 13.7% CAGR.

Demographic aging, rising obesity, and sports injury volumes expand the patient pool, while technological advances in cell-based implants and tissue-engineered scaffolds improve clinical outcomes. Outpatient arthroscopic procedures shorten recovery times and lower costs, reinforcing payer and provider adoption. North America leads revenue generation, but Asia-Pacific posts the fastest expansion as healthcare infrastructure and disposable incomes climb. Competitive activity is steady, with large device firms acquiring niche innovators to secure next-generation technologies.

Global Cartilage Repair/Regeneration Market Trends and Insights

Escalating Global Incidence of Osteoarthritis and Traumatic Cartilage Lesions

Surging osteoarthritis prevalence, which climbed 132.2% between 1990 and 2022, now affects 7.96% of the global population and drives sustained demand for restorative surgery. Adult cases aged 30-44 exceeded 32.97 million in 2022, underscoring a shift toward younger patients seeking durable repair solutions. Chondral defects afflict 36% of athletes' knees, creating a sizable cohort that prefers definitive intervention over symptom management . The widening patient base ensures that the cartilage repair market remains on an expanding trajectory through the decade.

Surge in Outpatient Minimally Invasive Orthopedic Procedures

Same-day discharge for joint surgeries in the United States rose from less than 1% in 2017 to 30.5% in 2023, demonstrating payer and provider confidence in ambulatory pathways. FDA clearance of MACI Arthro in August 2024 validated arthroscopic delivery of autologous chondrocyte implants, further normalizing outpatient treatment. Ambulatory surgical centers benefit most, displaying a 15.07% CAGR through 2030 as they combine cost savings with better patient convenience. This procedural migration underpins broader adoption across the cartilage repair market.

High Procedure and Implant Costs Limiting Uptake

Stem-cell knee therapy costs range between USD 5,000 and USD 15,000 in South Korea, restricting adoption beyond affluent or insured patients. China's volume-based procurement cut total hip arthroplasty prices by 50.1%, highlighting intense cost pressure that could spill over to cartilage technologies. Blue Cross payers in the United States mandate stringent criteria for autologous chondrocyte implantation, illustrating reimbursement hurdles. These economic constraints slow penetration in price-sensitive regions, tempering cartilage repair market growth.

Other drivers and restraints analyzed in the detailed report include:

- Breakthroughs in Tissue-Engineered Scaffolds and Cell-Based Implants

- Increasing Participation in High-Impact and Recreational Sports

- Lengthy and Complex Regulatory Approval Pathways

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hyaline tissue held 66.14% of revenue in 2024, confirming its central role in load-bearing joints most vulnerable to degeneration. Bilayer atelocollagen scaffolds now replicate hyaline morphology more reliably, improving long-term outlook for patients. Fibrocartilage, driven by meniscal repair needs, is projected to expand at 14.45% CAGR, supported by advances in collagen-based hydrogels that recruit endogenous stem cells.

The cartilage repair market size for hyaline applications is projected to widen further as surgeons prioritize tissue-specific products that enhance integration. Meanwhile, niche elastic-cartilage reconstruction for ear and nasal defects creates incremental volume, diversifying revenue streams across smaller sub-segments.

Cell-based solutions captured 62.39% revenue in 2024 through clinical superiority in pain reduction and tissue restoration, as evidenced by meta-analysis reporting standardized mean differences of -1.27 in pain scores . However, cell-free implants should post 14.69% CAGR through 2030 on the strength of off-the-shelf availability and lower cost.

Premium products such as MACI generated USD 46.3 million in Q1 2025 sales, reflecting commercial traction in the United States. Conversely, CARTIHEAL Agili-C offers a cell-free scaffold that reduced total knee arthroplasty risk by 87% at four years. Healthy rivalry between personalized and ready-to-use solutions ensures a balanced growth outlook across the cartilage repair market.

The Cartilage Repair Market Report is Segmented by Types of Cartilage (Hyaline, and More), Treatment Modality (Cell-Based, Non-cell-based/Cell-free), Treatment Type (Palliative, and More), Surgical Technique (ACI, and More), Application Site (Knee, Hip, and More), End User (Hospitals & Clinics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America produced 45.15% of 2024 revenue, underpinned by FDA clearances and consistent private-payer reimbursement. Vericel, Arthrex, and Stryker dominate surgeon preference, while Johnson & Johnson's VELYS unicompartmental knee robot received clearance in June 2024, spotlighting ongoing innovation. Growth remains steady as baby-boomer activity levels sustain procedure volumes.

Asia-Pacific is projected to deliver a 15.64% CAGR, buoyed by infrastructure investment and rising disposable incomes. China's procurement reforms, which halved implant prices, improve affordability even as regulatory pathways tighten. Japan leverages universal coverage for advanced therapies, whereas South Korea attracts inbound medical tourists for stem-cell knee repairs priced at USD 5,000-15,000. India's expanding middle class gradually lifts procedure counts despite reimbursement gaps.

Europe sustains innovation momentum through EMA's advanced therapy framework and EUR 11.3 million ENCANTO funding. Middle East & Africa and South America remain nascent yet compelling as economic development enlarges insured populations, positioning them as long-range demand reservoirs for the cartilage repair market.

List of Companies Covered in this Report:

- Arthrex

- Stryker

- Zimmer Biomet

- Smiths Group

- Johnson & Johnson

- Vericel

- Anika Therapeutics

- B. Braun

- Geistlich Pharma

- CYFUSE Biomedical K.K.

- Conmed

- MEDIPOST

- CartiHeal Ltd.

- Askel Healthcare Oy

- BioTissue

- Collagen Solutions

- Matricel

- Orthocell Ltd.

- Osiris Therapeutics

- Autocart Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Escalating Global Incidence Of Osteoarthritis And Traumatic Cartilage Lesions

- 4.2.2 Surge In Outpatient Minimally Invasive Orthopedic Procedures

- 4.2.3 Breakthroughs In Tissue-Engineered Scaffolds And Cell-Based Implants

- 4.2.4 Increasing Participation In High-Impact And Recreational Sports, Elevating Injury Volumes That Require Cartilage Repair

- 4.2.5 Increasing Reimbursement Coverage For Biologic Knee Restoration Across Major Markets

- 4.2.6 Expanding Participation In High-Impact Sports Raising Injury Volumes

- 4.3 Market Restraints

- 4.3.1 High Procedure And Implant Costs Limiting Uptake In Price-Sensitive Regions

- 4.3.2 Lengthy And Complex Regulatory Approval Pathways For Advanced Therapies

- 4.3.3 Limited Long-Term Clinical Durability Data Curbing Surgeon Confidence

- 4.3.4 Supply Constraints Of Qualified Donor Tissue And Gmp Manufacturing Capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory & Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Types of Cartilage

- 5.1.1 Hyaline Cartilage

- 5.1.2 Fibrocartilage

- 5.1.3 Elastic / Other Cartilage

- 5.2 By Treatment Modality

- 5.2.1 Cell-based Therapies

- 5.2.2 Non-cell-based / Cell-free Therapies

- 5.3 By Treatment Type

- 5.3.1 Palliative (Debridement, Viscosupplementation)

- 5.3.2 Intrinsic Repair Stimulus (ACI, MACI, Micro-fracture)

- 5.4 By Surgical Technique

- 5.4.1 Chondroplasty & Micro-fracture

- 5.4.2 Autologous Chondrocyte Implantation (ACI)

- 5.4.3 Matrix-induced ACI (MACI)

- 5.4.4 Osteochondral Allograft / Juvenile Allograft

- 5.5 By Application Site

- 5.5.1 Knee

- 5.5.2 Hip

- 5.5.3 Ankle

- 5.5.4 Spine

- 5.5.5 Other Joints (Shoulder, Elbow, Wrist)

- 5.6 By End User

- 5.6.1 Hospitals & Clinics

- 5.6.2 Ambulatory Surgical Centers

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East & Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East & Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Arthrex Inc.

- 6.3.2 Stryker

- 6.3.3 Zimmer Biomet

- 6.3.4 Smith + Nephew

- 6.3.5 Johnson & Johnson (DePuy Synthes)

- 6.3.6 Vericel Corporation

- 6.3.7 Anika Therapeutics Inc.

- 6.3.8 B. Braun SE

- 6.3.9 Geistlich Pharma AG

- 6.3.10 CYFUSE Biomedical K.K.

- 6.3.11 Conmed Corporation

- 6.3.12 MEDIPOST

- 6.3.13 CartiHeal Ltd.

- 6.3.14 Askel Healthcare Oy

- 6.3.15 BioTissue

- 6.3.16 Collagen Solutions PLC

- 6.3.17 Matricel GmbH

- 6.3.18 Orthocell Ltd.

- 6.3.19 Osiris Therapeutics

- 6.3.20 Autocart Inc.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment