PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849809

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849809

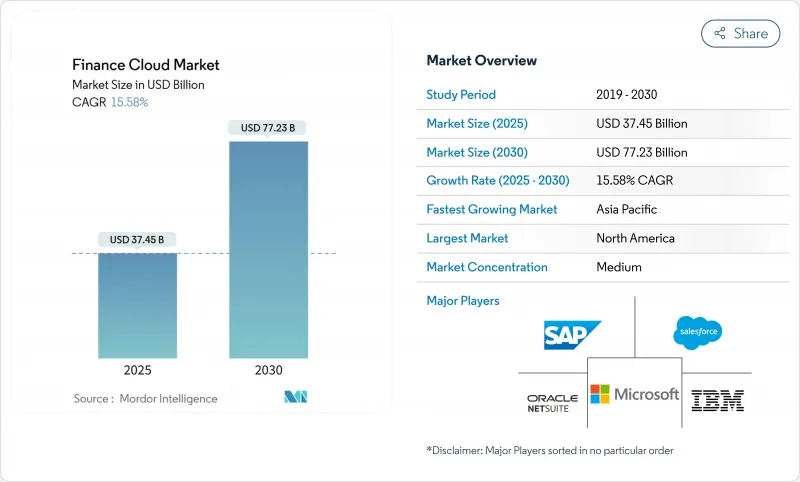

Finance Cloud - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The finance cloud market size is valued at USD 37.45 billion in 2025 and is set to reach USD 77.23 billion by 2030, advancing at a 15.6% CAGR.

Rising digital-first consumer expectations, tighter regulatory oversight, and the maturation of cloud security frameworks are driving widespread migration of core finance workloads to public and hybrid clouds. The European Union's Digital Operational Resilience Act (DORA) alone mandates upgraded ICT risk controls for about 22,000 financial entities and their technology partners, accelerating platform modernization across the region. At the same time, 98% of financial institutions globally already use at least one cloud service, up from 91% in 2020, confirming that the finance cloud market has reached critical mass. Generative AI roll-outs on cloud infrastructure now underpin everything from automated reconciliation to predictive cash-flow modelling, turning cloud providers into strategic partners for competitive differentiation. North American banks fund multibillion-dollar tech budgets to migrate thousands of applications, while Asia-Pacific institutions scale cloud-native cores to serve massive digital customer bases-all of which keeps the finance cloud market on a steep growth trajectory.

Global Finance Cloud Market Trends and Insights

Need for Improved Customer Relationship Management

Cloud-based CRM suites give financial institutions real-time insight into behavioural patterns, enabling hyper-personalised offers that improve retention in crowded markets. Asia-Pacific banks run cloud platforms capable of supporting tens of millions of concurrent sessions, as illustrated by AIBank's micro-services core that serves more than 100 million customers. In parallel, North American lenders integrate cloud analytics with loyalty engines to cut churn that still affects over 60% of legacy institutions. Because finance data is highly regulated, vendors differentiate through in-platform encryption, audit trails, and data-residency controls that satisfy regulators while still allowing cross-channel orchestration. As customer lifetime value becomes a pivotal KPI, the finance cloud market gains further momentum from banks' willingness to replace ageing CRM tools with elastic, AI-ready alternatives.

Demand for Operational Efficiency in Financial Sector

Moving finance workloads to consumption-based clouds converts capital expenditure into variable operating cost, releasing cash for product innovation. Institutions that completed full cloud migrations report 20-30% reductions in month-end close cycles and similar gains in regulatory reporting speed. Automation natively embedded in cloud ERPs eliminates manual journals, while serverless compute handles unpredictable spikes in payment volumes without performance degradation. Discover Financial Services, for example, relies on a hybrid estate to flex resources during seasonal spending peaks. As margins tighten, cost-to-income ratios now appear on board dashboards alongside revenue, reinforcing the efficiency narrative that will continue to propel the finance cloud market.

Rise of Cloud-based Cyber Threats

Financial services remain the top target for sophisticated attacks, and cloud environments enlarge the threat surface. US regulators report escalating ransom incidents that disrupt critical payment infrastructures, prompting banks to double investments in zero-trust architectures and extended detection platforms. Migrating sensitive data without commensurate security uplift exposes institutions to regulatory fines that can exceed annual IT budgets. Cloud providers answer with confidential computing, hardware-rooted encryption, and sovereign-cloud blueprints, yet implementing these controls adds cost and complexity, muting short-term acceleration in the finance cloud market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Push for Real-Time Transparency and Reporting

- GenAI-enabled Self-service Finance Analytics

- Legacy-core Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The Financial Forecasting and Planning segment retained 38.3% revenue in 2024, reflecting the universal need for scenario modelling when economic volatility remains high. Cloud-based EPM suites let finance teams generate rolling forecasts across thousands of cost centres, elevating data-driven decision-making. Integrated driver-based models update profit outlooks instantly after rate or FX shocks, reinforcing migration urgency. Concurrently, Risk, Compliance, and RegTech is the fastest-growing solution line, advancing at 15.9% CAGR through 2030 on the back of DORA and comparable regimes. Vendors embed API-ready regulatory libraries so institutions can push granular transaction data to supervisors with one-click reporting. Continuous control monitoring features lower audit-prep workloads, translating compliance budgets directly into demand for the finance cloud market.

Core Accounting and General Ledger platforms remain indispensable, acting as system-of-record anchors for all other cloud finance modules. Treasury and Cash-Management tools gain new momentum as volatile funding markets prioritise real-time liquidity insight. Citigroup, for instance, expanded its cloud treasury workspace to aggregate global cash positions minute-by-minute. Payroll and Workforce Finance applications benefit from tight finance-HR convergence; Workday's latest release bundles headcount planning with spend analytics, underscoring how integrated suites improve enterprise alignment. As vendors package these capabilities under unified data fabrics, upsell pipelines expand, driving sustainable revenue streams within the finance cloud market.

Public clouds controlled 57.6% of 2024 revenue due to hyperscalers' global footprints, advanced security certifications, and continuous innovation roadmaps. Banks routinely adopt managed PaaS databases to accelerate new product rollouts without provisioning hardware. Yet dependence on a single provider raises resilience concerns, propelling Hybrid and Multi-Cloud uptake at 17.0% CAGR. European lenders, mindful of concentration risk outlined by regulators, increasingly split workloads across at least two vendors, while retaining ultra-low-latency trading engines on private clouds. Form3's payment platform exemplifies this strategy, abstracting routing logic so banks can toggle endpoints among clouds during outages.

Private clouds remain vital for use cases with stringent performance or data-sovereignty requirements. JPMorgan Chase is spending USD 2 billion on four new private cloud data centres that anchor latency-sensitive risk computations. Unified observability stacks and policy-as-code reduce operational friction across mixed estates, making hybrid truly seamless. Because regulatory discourse now explicitly references "exit plans," institutions favour containerised workloads and open APIs to avoid lock-in, a development that further broadens addressable opportunity for the finance cloud market.

The Finance Cloud Market Report is Segmented by Solution (Core Accounting and GL, Financial Forecasting and Planning, and More), Deployment Model (Public Cloud, Private Cloud, and Hybrid / Multi-Cloud), End-User (Banking, Insurance, Capital Markets, and More), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 41.0% of 2024 revenue thanks to deep technology budgets and regulatory clarity that fosters accelerated migration. The United States anchors the region, with JPMorgan Chase alone allocating USD 17 billion annually to tech and moving 6,000 applications to cloud platforms. Canada follows with open-banking guidelines that encourage secure API ecosystems, while Mexican banks adopt cloud to meet cross-border reporting standards. Public-private collaboration on cybersecurity and digital-identity frameworks further de-risks adoption, strengthening the finance cloud market in the region. Providers leverage dense data-centre footprints to meet sub-10-millisecond latency thresholds demanded by high-frequency traders.

Asia-Pacific is the fastest-growing territory at 16.2% CAGR through 2030. Government-backed digital-economy blueprints place cloud at the centre of financial-inclusion agendas, underpinning a regional digital-economy value expected to reach USD 1 trillion by 2030. China's AIBank demonstrates cloud scalability by serving over 100 million customers on a containerised platform. India's public-cloud policy now allows regulated entities to host core data offshore under strict encryption keys, unlocking broader hyperscaler adoption. Japan and Australia endorse Industry-Cloud models that deliver pre-certified compliance artefacts for local supervisory bodies. Coupled with rising fee-based revenue targets-APAC banks expect digital adjacencies to supply 40% of profit pools by 2030-these trends ensure sustained upside for the finance cloud market.

Europe accelerates cloud modernisation under DORA's operational-resilience mandate, affecting roughly 22,000 financial organisations. Germany, France, and the United Kingdom roll out shared testing frameworks for cyber-incident simulations, incentivising the adoption of platforms that automate evidence collection. Sovereign-cloud regions operated by large providers satisfy data-sovereignty clauses, while multi-vendor strategies mitigate systemic risk. South America charts high growth, powered by Brazil's branchless challenger banks such as Nubank, which posted USD 2 billion profit in 2024 while operating entirely on cloud infrastructure. Middle East and Africa adoption climbs swiftly; 83% of MENA financial firms now run cloud workloads and expect USD 21.14 million in annual savings within two years. Gulf Cooperation Council banks align national cloud mandates with ambitious digital transformation roadmaps, solidifying new demand pockets for the finance cloud market.

- Oracle Corporation(Netsuite)

- SAP

- Microsoft

- Salesforce

- IBM

- Workday

- Sage Intacct

- Unit4 / FinancialForce

- Intuit

- Anaplan

- Workiva

- BlackLine

- Coupa

- Xero

- FIS

- Fiserv

- Temenos

- Finastra

- Acumatica

- AWS

- Google Cloud

- Huawei

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Need for improved customer relationship management

- 4.2.2 Demand for operational efficiency in financial sector

- 4.2.3 Regulatory push for real-time transparency and reporting

- 4.2.4 GenAI-enabled self-service finance analytics

- 4.2.5 FinOps adoption to optimise cloud spending

- 4.2.6 Industry-cloud platforms for BFSI verticals

- 4.3 Market Restraints

- 4.3.1 Rise of cloud-based cyber threats

- 4.3.2 Legacy-core integration complexity

- 4.3.3 Talent gap in cloud-FinOps and data engineering

- 4.3.4 Vendor lock-in and GenAI cost overruns

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Solution

- 5.1.1 Core Accounting and GL

- 5.1.2 Financial Forecasting and Planning

- 5.1.3 Risk, Compliance and Reg-Tech

- 5.1.4 Treasury and Cash-Management

- 5.1.5 Payroll and Workforce Finance

- 5.2 By Deployment Model

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid / Multi-Cloud

- 5.3 By End-User

- 5.3.1 Banking

- 5.3.2 Insurance

- 5.3.3 Capital Markets

- 5.3.4 FinTech / Neo-banks

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Oracle Corporation(Netsuite)

- 6.4.2 SAP

- 6.4.3 Microsoft

- 6.4.4 Salesforce

- 6.4.5 IBM

- 6.4.6 Workday

- 6.4.7 Sage Intacct

- 6.4.8 Unit4 / FinancialForce

- 6.4.9 Intuit

- 6.4.10 Anaplan

- 6.4.11 Workiva

- 6.4.12 BlackLine

- 6.4.13 Coupa

- 6.4.14 Xero

- 6.4.15 FIS

- 6.4.16 Fiserv

- 6.4.17 Temenos

- 6.4.18 Finastra

- 6.4.19 Acumatica

- 6.4.20 AWS

- 6.4.21 Google Cloud

- 6.4.22 Huawei

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment