PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849818

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849818

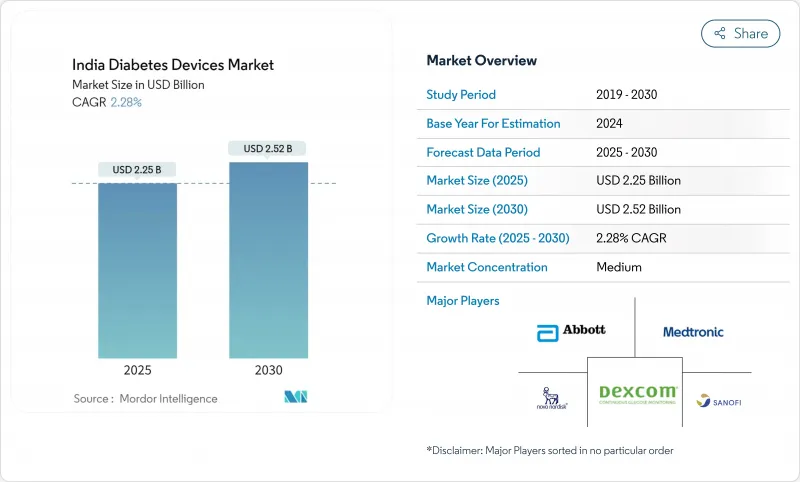

India Diabetes Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The India diabetes devices market is valued at USD 2.25 billion in 2025 and is forecast to reach USD 2.52 billion by 2030, expanding at a 2.28% CAGR.

Structural shifts shaping the India diabetes devices market include the government's Production Linked Incentive (PLI) scheme that has cleared 19 green-field projects covering 44 formerly imported device categories. Adoption of digital health is rising, with more than 400,000 patients using platforms such as Apollo Sugar for remote monitoring. Continuous glucose monitoring (CGM) reimbursement pilots under public schemes, expanding pharmacy-led programs, and employer-funded digital benefits are broadening access, even as high GST on consumables and patchy cold-chain logistics restrain growth. Multinational and domestic firms are racing to localize manufacturing, integrate connected solutions, and secure distribution footprints that reach tier-2/3 cities.

India Diabetes Devices Market Trends and Insights

Rising Prevalence of Obesity Among Youth Increasing Earlier Onset Diabetes

Government surveys show 24% of women and 23% of men ages 15-49 are overweight or obese, accelerating diabetes onset and shifting device demand toward technology-centric monitoring. Younger patients adopt CGMs more readily than finger-stick glucometers, driving rapid uptake in urban metros. Digital platforms report high engagement from users under 35, and clinicians increasingly recommend continuous monitoring earlier in the disease course. Growing urban lifestyles that foster metabolic syndrome are widening the addressable market for advanced devices and stimulating manufacturers to launch youth-oriented product lines.

Expanding Public Reimbursement for CGM Sensors

Pilot programs under the Central Government Health Scheme and Employee State Insurance Corporation now reimburse CGM sensors for Type-1 and insulin-dependent Type-2 patients. Private insurers such as ICICI Lombard have released diabetes plans bundling device coverage, yet reimbursement ceilings remain below retail prices, limiting mass adoption. Over time, broader coverage is expected to spur volume growth and encourage manufacturers to localize production to meet price points aligned with public budgets.

High GST Slab (12%) on Testing Consumables

The 12% GST on glucometer strips inflates recurring costs for frequent testers, impeding adherence among low-income patients. Advocates urge re-classification as essential devices to achieve tax exemption comparable to life-saving drugs. Price pressure favors bundled strip-subscription models from online platforms that spread payments over time, yet overall uptake in semi-urban zones remains constrained

Other drivers and restraints analyzed in the detailed report include:

- Rising Prevalence & Earlier Onset of Type-2 Diabetes

- Pharmacy-led Diabetes Management Programs

- Government PLI Scheme for Local Device Production

- Patchy Cold-chain for Insulin Cartridges in Tier-3 Cities

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Monitoring devices held 58.12% of 2024 revenue, underscoring their foundational role for India's 77 million diabetics. The India diabetes devices market size for monitoring products is projected to expand at 2.1% CAGR as commoditization drives price competition. Continuous glucose monitoring outpaces legacy glucometers inside the monitoring portfolio, aided by sensor accuracy gains and mobile app integration. Meanwhile, management devices-comprising insulin pumps, smart pens, and delivery accessories-register a 3.54% CAGR. Hospitals implementing closed-loop systems and employer health plans covering pumps propel segment growth. The India diabetes devices market share of management devices may therefore edge upward as affordability improves and bundled reimbursement widens.

Price disparities remain stark: Abbott's discontinued INR 2,000 Libre Pro formerly lowered barriers, whereas current alternatives exceed INR 5,000. Domestic entrants exploring reusable transmitters and low-cost sensors aim to restore affordability. Studies from tertiary centers reveal HbA1c drops of 1.1 percentage points among CGM users versus finger-stick cohorts. Evidence supports clinician advocacy for continuous monitoring, expanding long-run penetration beyond affluent urban niches.

Type-2 patients account for 92.14% revenue and represent the fastest-growing pool owing to lifestyle risk factors. The India diabetes devices market size linked to Type-2 users is forecast to rise steadily at 3.89% CAGR through 2030. Early-onset diagnosis shifts purchasing behavior-young professionals demand connected devices that sync with fitness apps while retirees stay with basic glucometers. Digital twin interventions delivered over smartphone platforms help 89% of Type-2 users achieve HbA1c below 7% in controlled studies.

Type-1 patients, though fewer, remain heavy per-capita consumers of pumps, CGMs, and patch pens. Continuous innovation in closed-loop algorithms first targets this cohort, with cost reductions over time filtering into Type-2 indications. Gestational and other specific diabetes categories form a high-acuity niche addressed by hospital-based CGM rental models during pregnancy.

The Indian Diabetes Device Market is Segmented by Device Type (Monitoring Devices and Management Devices), Patient Type (Type-1 Diabetes, Type-2 Diabetes, and Gestational & Other Specific Types), End User (Home-Care Settings, and Hospitals & Specialty Clinics), Sales Channel (Pharmacy Retail and Pharmacy Retail). The Report Offers the Value (in USD) and Volume (in Units) for the Above Segments.

List of Companies Covered in this Report:

- Abbott Laboratories

- Medtronic

- Roche

- Becton Dickinson (BD)

- Novo Nordisk

- Sanofi

- Eli Lilly and Company

- Dexcom

- Insulet

- Tandem Diabetes Care

- Ypsomed

- LifeScan (J&J)

- Ascensia

- Terumo

- Nipro

- HTL-Strefa

- AgVa Healthcare

- Beckton Dickinson

- Senseonics

- Sugarmate

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Prevalence of Obesity Among Youth Increasing Earlier Onset Diabetes

- 4.2.2 Expanding public reimbursement for CGM sensors

- 4.2.3 Rising prevalence & earlier onset of Type-2 diabetes

- 4.2.4 Pharmacy-led diabetes management programs

- 4.2.5 Government PLI scheme for local device production

- 4.2.6 Employer-funded health-tech benefit platforms

- 4.3 Market Restraints

- 4.3.1 High GST slab (12%) on testing consumables

- 4.3.2 Patchy cold-chain for insulin cartridges in tier-3 cities

- 4.3.3 Low CGM prescription awareness among primary physicians

- 4.3.4 Data-privacy concerns around connected pumps

- 4.4 Value-/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Device Type (Value)

- 5.1.1 Monitoring Devices

- 5.1.1.1 Self-Monitoring Blood Glucose (SMBG)

- 5.1.1.1.1 Glucometers

- 5.1.1.1.2 Test Strips

- 5.1.1.1.3 Lancets

- 5.1.1.2 Continuous Glucose Monitoring (CGM)

- 5.1.1.2.1 Sensors

- 5.1.1.2.2 Durables (Transmitters/Receivers)

- 5.1.2 Management Devices

- 5.1.2.1 Insulin Pumps

- 5.1.2.1.1 Pump Device

- 5.1.2.1.2 Pump Reservoir

- 5.1.2.1.3 Infusion Set

- 5.1.2.2 Insulin Syringes

- 5.1.2.3 Insulin Cartridges

- 5.1.2.4 Disposable Pens

- 5.1.1 Monitoring Devices

- 5.2 By Patient Type

- 5.2.1 Type-1 Diabetes

- 5.2.2 Type-2 Diabetes

- 5.2.3 Gestational & Other Specific Types

- 5.3 By End User

- 5.3.1 Hospitals & Specialty Clinics

- 5.3.2 Home-Care Settings

- 5.4 By Sales Channel

- 5.4.1 Pharmacy Retail

- 5.4.2 E-commerce & D-to-C

6 Market Indicators

- 6.1 Type-1 Diabetes Population

- 6.2 Type-2 Diabetes Population

7 Competitive Landscape

- 7.1 Market Concentration

- 7.2 Market Share Analysis

- 7.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 7.3.1 Abbott

- 7.3.2 Medtronic

- 7.3.3 Roche

- 7.3.4 Becton Dickinson (BD)

- 7.3.5 Novo Nordisk

- 7.3.6 Sanofi

- 7.3.7 Eli Lilly

- 7.3.8 Dexcom

- 7.3.9 Insulet

- 7.3.10 Tandem Diabetes Care

- 7.3.11 Ypsomed

- 7.3.12 LifeScan (J&J)

- 7.3.13 Ascensia Diabetes Care

- 7.3.14 Terumo

- 7.3.15 Nipro

- 7.3.16 HTL-Strefa

- 7.3.17 AgVa Healthcare

- 7.3.18 BeatO

- 7.3.19 Senseonics

- 7.3.20 Sugarmate

8 Market Opportunities & Future Outlook

- 8.1 White-space & Unmet-Need Assessment