PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849831

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849831

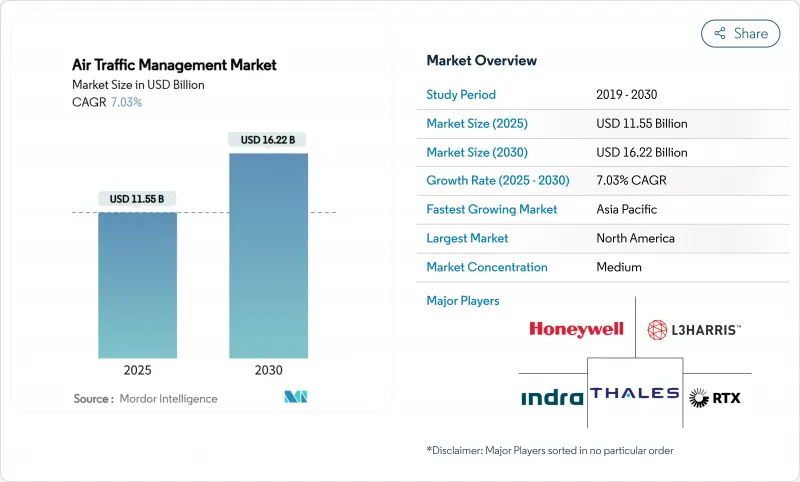

Air Traffic Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The global air traffic management market size is estimated at USD 11.55 billion in 2025, and is projected to reach USD 16.22 billion by 2030, translating into a steady 7.03% CAGR over the forecast period.

Robust demand stems from the aviation sector's need to replace legacy infrastructure, integrate satellite-based surveillance, and handle unprecedented traffic volumes. The Federal Aviation Administration (FAA) confirms that 285 of its 313 air traffic facilities remain understaffed, highlighting urgent capacity bottlenecks that accelerate technology procurement. Expansion of multi-billion-dollar airport programs in Asia, widespread mandates for Automatic Dependent Surveillance-Broadcast (ADS-B), and increasing unmanned aircraft operations collectively reinforce the positive growth outlook for the air traffic management market. Government-funded modernization efforts such as the United States' NextGen program, Europe's SESAR Digital Sky initiative, and similar investments across emerging hubs provide a stable revenue pipeline for system suppliers. Meanwhile, the shift toward AI-enabled flow management and cloud-native architectures illustrates how software-centric innovation now drives a larger share of customer spending within the air traffic management market.

Global Air Traffic Management Market Trends and Insights

Expansion of Airport Infrastructure to Support Increasing Air Traffic

Airport development programs valued at USD 1 trillion across the Middle East, Africa, and South Asia are redefining capacity needs and boosting the air traffic management market. Ethiopia's planned mega-airport city will handle 110 million passengers annually-more than quadrupling the nation's current capacity-and drive demand for scalable conflict-resolution software. The USD 35 billion Al Maktoum International Airport redevelopment in the UAE embeds next-generation ATM capability from day one, avoiding costly retrofits. India's target of over 220 new airports by 2035 further elevates the requirement for interoperable surveillance, navigation, and communication systems within the air traffic management market. These large-scale expansions amplify the complexity of flow management, spurring accelerated deployment of AI-enabled automation platforms.

Regulatory Mandates for ADS-B and Performance-Based Navigation (PBN)

Mandatory ADS-B equipage continues to spread beyond early adopters. NAV CANADA enforced ADS-B Out in domestic Class B airspace in May 2024, illustrating how regulators compress compliance timelines. Twelve nations now impose ADS-B rules for designated corridors, while ICAO's PBN framework provides collaborative benchmarks to harmonize implementation. Europe's updated Regulation 2023/1770 sustains retrofit momentum despite the repeal of the earlier 2011 rule, ensuring continued hardware and software upgrades for the air traffic management market. The variability of regional mandates still challenges fleet operators, but it guarantees sustained demand for surveillance avionics and ground infrastructure through the decade.

Cybersecurity Risks in Virtualized and Network-Centric ATM Systems

A 131% rise in aviation-related cyberattacks between 2022 and 2023 underscores vulnerabilities created by cloud adoption and interconnected networks. EASA's forthcoming Part-IS regulation will integrate cyber-risk oversight into air traffic safety rules by 2025, but maturity gaps across regions remain significant. Ransomware campaigns against airlines and aerospace OEMs, including a six-fold increase reported by Resecurity, indicate the potential for cascade effects on operational air traffic management market infrastructure. While ANSPs invest in zero-trust architectures and segmentation, the cost and complexity of full compliance dampen short-term modernization budgets.

Other drivers and restraints analyzed in the detailed report include:

- Rising Commercial Drone Operations Necessitating U-Space/UTM Integration

- Major Investments in NextGen and SESAR Digital Sky Programs

- High Capital Requirements for Transitioning from Radar to Satellite-Based CNS/ATM

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Air Traffic Control (ATC) retained 50.04% of the air traffic management market share in 2024, underscoring its foundational role in keeping manned aviation safe and efficient. Unmanned Traffic Management (UTM) is expanding at a 9.45% CAGR as regulators clear beyond-visual-line-of-sight drone flights, making integration software essential for future capacity. The Air Traffic Management market size allocated to ATC continues to grow in absolute terms, but its share will moderate as UTM platforms gain funding priority in national budgets.

Air Traffic Flow and Capacity Management (ATFCM) and Aeronautical Information Management (AIM) platforms increasingly blur with core ATC functions, driven by demand for unified situational awareness dashboards. Integrated suites like Thales's TopSky provide consolidated manned-and-unmanned oversight, reinforcing vendor lock-in opportunities in the air traffic management market.

Hardware contributed 67.21% of the air traffic management market size in 2024, reflecting mandated radar upgrades, digital radios, and surveillance sensors. Software, however, is the fastest-growing component at 8.21% CAGR, benefiting from AI decision-support, cloud hosting, and data analytics modules that add post-deployment value. Services revenue scales alongside ANSPs as they outsource lifecycle support to manage complexity.

Software-defined architectures allow rapid feature deployment without extensive site visits, shortening payback periods and catalyzing a shift from CapEx to OpEx. This model incentivizes incumbents and new entrants to prioritize open APIs and continuous delivery pipelines, reshaping competition in the broader air traffic management market.

The Air Traffic Management Market Report is Segmented by Domain (Air Traffic Control, Air Traffic Flow and Capacity Management, Aeronautical Information Management, and More), Component (Hardware, Software, and Services), Application (Communication, Navigation, Surveillance, and More), End-Use (Commercial Aviation, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained 30.20% of the air traffic management market share in 2024 as the FAA's NextGen program continued to generate measurable capacity and fuel-saving benefits. However, controller shortages highlighted by 285 understaffed facilities restrain near-term throughput despite rising capital allocations from federal budgets. Canada's collaborative contracts with Indra for trajectory-based operations and ongoing UTM trials reinforce regional commitment to next-generation services.

Asia-Pacific is the fastest-growing region at an 8.45% CAGR to 2030, propelled by airport capacity expansions such as Narita's slot increase from 300,000 to 500,000 flights annually. India's rollout of more than 220 airports by 2035 and emerging drone logistics corridors unlock a sizeable addressable Air Traffic Management market. Thales innovation labs across Melbourne and Singapore, and L3Harris's FTI India gateway position global suppliers close to high-growth demand centers.

Europe benefits from policy coordination under the Single European Sky 2+ framework and a refreshed SESAR investment plan emphasizing digitization and sustainability. COOPANS' TopSky-ATC One migration, covering 14% of continental traffic, showcases how cooperative procurement helps smaller ANSPs access best-in-class solutions. Environmental priorities, including mandated sustainable fuel blending, incentivize flight-path optimization applications that align with EU-wide decarbonization goals, driving incremental spending within the air traffic management market.

- Thales Group

- RTX Corporation

- L3Harris Technologies, Inc.

- Indra Sistemas, S.A.

- Honeywell International Inc.

- Leonardo S.p.A

- Frequentis AG

- Saab AB

- Adacel Technologies Limited

- Advanced Navigation and Positioning Corporation

- SITA N.V.

- Northrop Grumman Corporation

- NATS

- NAV CANADA

- Aena SME, S.A.

- Kongsberg Gruppen ASA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of airport infrastructure to support increasing air traffic

- 4.2.2 Regulatory mandates for ADS-B and performance-based navigation (PBN)

- 4.2.3 Rising commercial drone operations necessitating U-space/UTM integration

- 4.2.4 Major investments in NextGen and SESAR digital sky programs

- 4.2.5 Adoption of AI-based air traffic flow management solutions

- 4.2.6 Incentives for sustainable flight paths and SAF-compatible ATM systems

- 4.3 Market Restraints

- 4.3.1 Cybersecurity risks in virtualized and network-centric ATM systems

- 4.3.2 High capital requirements for transitioning from radar to satellite-based CNS/ATM

- 4.3.3 Air navigation service provider (ANSP) workforce gaps and controller fatigue

- 4.3.4 Lack of regulatory alignment for cross-border UTM implementation

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers/Consumers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Domain

- 5.1.1 Air Traffic Control (ATC)

- 5.1.2 Air Traffic Flow and Capacity Management (ATFCM)

- 5.1.3 Aeronautical Information Management (AIM)

- 5.1.4 Unmanned Traffic Management (UTM)

- 5.2 By Component

- 5.2.1 Hardware

- 5.2.2 Software

- 5.2.3 Services

- 5.3 By Application

- 5.3.1 Communication

- 5.3.2 Navigation

- 5.3.3 Surveillance

- 5.3.4 Automation and Decision-Support

- 5.4 By End-use

- 5.4.1 Commercial Aviation

- 5.4.2 Military and Government

- 5.4.3 Urban Air Mobility/Drone Operations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Thales Group

- 6.4.2 RTX Corporation

- 6.4.3 L3Harris Technologies, Inc.

- 6.4.4 Indra Sistemas, S.A.

- 6.4.5 Honeywell International Inc.

- 6.4.6 Leonardo S.p.A

- 6.4.7 Frequentis AG

- 6.4.8 Saab AB

- 6.4.9 Adacel Technologies Limited

- 6.4.10 Advanced Navigation and Positioning Corporation

- 6.4.11 SITA N.V.

- 6.4.12 Northrop Grumman Corporation

- 6.4.13 NATS

- 6.4.14 NAV CANADA

- 6.4.15 Aena SME, S.A.

- 6.4.16 Kongsberg Gruppen ASA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment