PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849852

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1849852

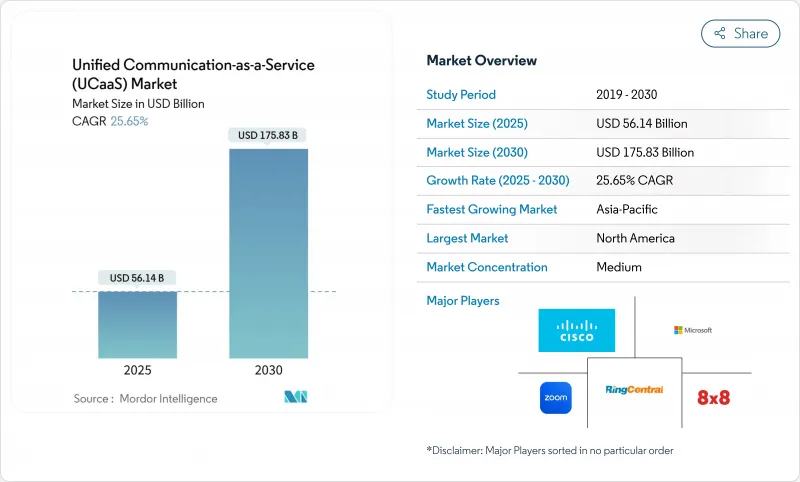

Unified Communication-as-a-Service (UCaaS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The UCaaS market is valued at USD 56.14 billion in 2025 and is projected to reach USD 175.83 billion in 2030, advancing at a 25.65% CAGR.

The rapid expansion is fueled by enterprise-wide consolidation of fragmented communication tools, measurable ROI from AI-powered productivity functions, and an inflection point in cloud telephony adoption that now extends well beyond basic voice replacement. North American enterprises still account for the largest regional share, yet Asia-Pacific is growing at double-digit rates as 5G networks and mobile-first strategies unlock frontline use cases. Large organizations remain the primary revenue contributors, but cost-sensitive SMEs are embracing pay-as-you-go models that free them from capital outlays while enhancing resilience. Providers that integrate UCaaS with CCaaS and CPaaS are expanding wallet share, and security-driven regional data residency frameworks are becoming a baseline requirement that shapes global roll-outs.

Global Unified Communication-as-a-Service (UCaaS) Market Trends and Insights

Pay-as-you-go OPEX Model Attracts Cost-Sensitive SMEs

Hosted UCaaS solutions let smaller businesses replace capital-heavy PBX systems with predictable monthly fees, yielding up to 55% cost savings over premises-based telephony. SMEs consequently represent the fastest-growing user cohort, posting a 27.8% CAGR from 2024 to 2030. Security matters just as much as cost: 51.3% of SMEs cite cyber protection as their top technology priority, viewing enterprise-grade cloud defenses as superior to in-house safeguards. Uptake is particularly strong in emerging Asia-Pacific and Latin America, where local connectivity partners bundle voice, video, and messaging with 5G mobile access to deliver a fully managed service.

Remote and Hybrid Work Policies Cement Work-from-Anywhere Demand

Hybrid schedules are now permanent, with 91% of employers offering flexible work and 98% of meetings featuring at least one remote participant. A unified platform that combines voice, video, chat, and file sharing has become mission-critical infrastructure, not a discretionary tool. Employees lose 36 minutes daily when forced to juggle multiple apps, prompting CIOs to consolidate overlapping services. North American enterprises are modernizing outdated meeting rooms with AI-assisted devices that auto-frame speakers and generate live captions, while European firms emphasize privacy-led data handling in compliance with GDPR.

Skills Gap in Multi-Vendor UC Stacks Prolongs Migration Cycles

Enterprises cite a lack of cloud-native voice engineers and API integration specialists as the main impediment to migration, with 62% of IT leaders reporting delays. Larger organizations struggle to mesh legacy PBX, SIP trunking, and new AI services without downtime, forcing reliance on costly systems integrators. This bottleneck is particularly visible in banking and healthcare, where security scrutiny extends project timelines.

Other drivers and restraints analyzed in the detailed report include:

- Integration of UCaaS with CCaaS and CPaaS Broadens Wallet Share

- AI-Powered Productivity Features Lift ROI

- Rising Toll-Fraud and SIP-Trunk Security Breaches Inflate TCO

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Telephony accounted for 38.3% of UCaaS market share in 2024, yet collaboration platforms are growing at a 28.3% CAGR, echoing the pivot from stand-alone voice to integrated video, chat, and content sharing. Unified messaging and multi-party conferencing tools secure ongoing budget priority as CIOs seek productivity gains. Investments flow toward AI-enhanced features such as live translation, real-time whiteboarding, and automated action tracking that convert meetings into corporate knowledge.

The UCaaS market size for collaboration platforms is forecast to reach USD 82 billion by 2030, reflecting adoption across all verticals. Telephony remains essential for regulated call recording and emergency services, but commoditization pressures persist. Vendors differentiate via embedded analytics, guaranteed quality-of-service, and regional data residency that satisfy public-sector requirements.

Unified Communication-As-A-Service (UCaaS) Market is Segmented by by Component (Telephony, Unified Messaging and More), End-User Enterprise Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Vertical (BFSI, Retail and E-Commerce, Education and More) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the UCaaS market with 43.4% revenue share in 2024 thanks to widespread cloud maturity, robust broadband infrastructure, and entrenched Microsoft Teams deployments. The United States further benefits from FedRAMP-certified offerings that unlock public-sector contracts. Growth is slowing to low-double digits as penetration nears saturation, yet AI integration, contact-center convergence, and frontline worker solutions keep spending momentum intact.

Europe follows with steady uptake in the United Kingdom, Germany, and France. GDPR, the Digital Markets Act, and impending national cloud regulations prompt enterprises to favor providers with local data centers and cross-platform interoperability. Independent service providers gain share by tailoring solutions to linguistic requirements and vertical compliance rules, especially in health and public administration.

Asia-Pacific delivers the strongest trajectory at a 30.4% CAGR through 2030. National 5G coverage, mobile-only workforces, and government-sponsored digital agendas propel adoption in Japan, South Korea, Singapore, and Australia. Southeast Asian nations are leapfrogging fixed-line limitations, with cloud-native UCaaS meeting multilingual needs and price points for SMEs. The UCaaS market size in Asia-Pacific is forecast to match North America by 2030 if current momentum continues. Latin America and the Middle East and Africa trail but show rising opportunity through fiber and 4G/5G roll-outs that lower access costs for cloud communications.

- Microsoft Corp.

- Cisco Systems Inc.

- Zoom Video Communications Inc.

- RingCentral Inc.

- 8x8 Inc.

- Mitel Networks Corp.

- Verizon Communications Inc.

- BT Group plc

- Vodafone Group plc

- NTT Communications Corp.

- Telstra Corp. Ltd.

- Deutsche Telekom AG (T-Systems)

- Orange Business Services

- ATandT Inc.

- Nextiva Inc.

- Gamma Communications plc

- KPN N.V.

- Telia Co. AB

- PCCW Global

- Maxis Bhd.

- PLDT Enterprise

- Wildix

- Avaya LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pay-as-you-go OPEX model attracts cost-sensitive SMEs

- 4.2.2 Remote and hybrid work policies cement work-from-anywhere demand

- 4.2.3 Integration of UCaaS with CCaaS and CPaaS broadens wallet-share

- 4.2.4 AI-powered productivity (meeting summaries, voice bots) lifts ROI

- 4.2.5 5G-enabled mobile-first UCaaS in frontline/field operations

- 4.2.6 FedRAMP-grade secure-UCaaS unlocks regulated-industry adoption

- 4.3 Market Restraints

- 4.3.1 Skills gap in multi-vendor UC stacks prolongs migration cycles

- 4.3.2 Rising toll-fraud and SIP-trunk security breaches inflate TCO

- 4.3.3 Voice-quality variance on over-the-top public internet links

- 4.3.4 National data-sovereignty laws constrain global seat roll-outs

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Telephony

- 5.1.2 Unified Messaging

- 5.1.3 Audio / Video Conferencing

- 5.1.4 Collaboration Platforms

- 5.2 By End-user Enterprise Size

- 5.2.1 Small and medium enterprises

- 5.2.2 Large Enterprises

- 5.3 By End-user Vertical

- 5.3.1 BFSI

- 5.3.2 Retail and e-Commerce

- 5.3.3 Healthcare and Life Sciences

- 5.3.4 Government and Public Sector

- 5.3.5 IT and Telecom

- 5.3.6 Education

- 5.3.7 Others (Manufacturing, Hospitality, etc.)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Russia

- 5.4.3.6 Spain

- 5.4.3.7 Switzerland

- 5.4.3.8 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 South Korea

- 5.4.4.5 Malaysia

- 5.4.4.6 Singapore

- 5.4.4.7 Vietnam

- 5.4.4.8 Indonesia

- 5.4.4.9 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 Nigeria

- 5.4.5.2.2 South Africa

- 5.4.5.2.3 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Microsoft Corp.

- 6.4.2 Cisco Systems Inc.

- 6.4.3 Zoom Video Communications Inc.

- 6.4.4 RingCentral Inc.

- 6.4.5 8x8 Inc.

- 6.4.6 Mitel Networks Corp.

- 6.4.7 Verizon Communications Inc.

- 6.4.8 BT Group plc

- 6.4.9 Vodafone Group plc

- 6.4.10 NTT Communications Corp.

- 6.4.11 Telstra Corp. Ltd.

- 6.4.12 Deutsche Telekom AG (T-Systems)

- 6.4.13 Orange Business Services

- 6.4.14 ATandT Inc.

- 6.4.15 Nextiva Inc.

- 6.4.16 Gamma Communications plc

- 6.4.17 KPN N.V.

- 6.4.18 Telia Co. AB

- 6.4.19 PCCW Global

- 6.4.20 Maxis Bhd.

- 6.4.21 PLDT Enterprise

- 6.4.22 Wildix

- 6.4.23 Avaya LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment