PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850025

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850025

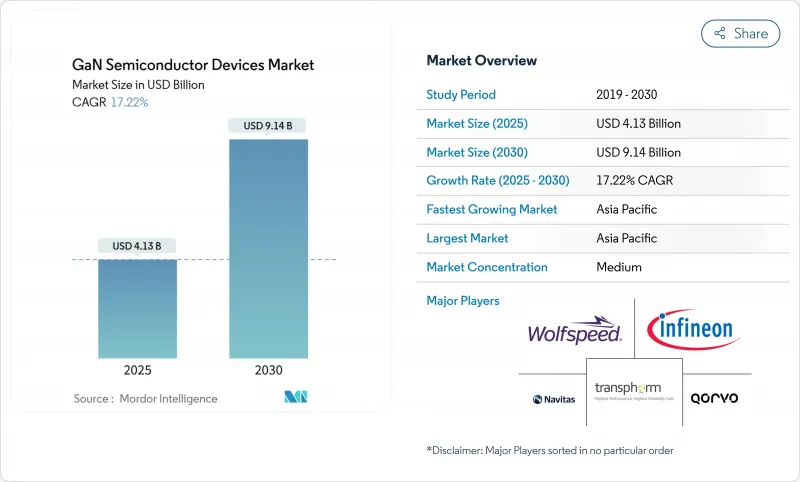

GaN Semiconductor Devices - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The gallium nitride semiconductor devices market size stood at USD 4.13 billion in 2025 and is forecast to touch USD 9.14 billion by 2030, reflecting a robust 17.22% CAGR.

The surge mirrors GaN's intrinsic ability to deliver higher efficiency, faster switching, and superior thermal performance when compared with legacy silicon. Market momentum was reinforced in 2024 and early 2025 by three concurrent shifts: 800 V electric-vehicle powertrains, large-scale 5G rollouts that require high-power radio-frequency amplifiers, and consumer demand for ultra-compact USB-C chargers exceeding 100 W. At the same time, global energy-efficiency regulations tightened, pushing data-center operators and industrial OEMs toward GaN-based conversion stages that cut losses and shrink cooling overhead. Corporate investment underscored the trend as Infineon, Renesas, and other incumbents expanded GaN capacity through acquisitions, while regional incentives in Japan and the European Union accelerated green-field fabs geared to 6-inch and 8-inch wafers.

Global GaN Semiconductor Devices Market Trends and Insights

Proliferation of 65-240 W USB-C PD GaN Chargers Led by Chinese OEM Road-maps

Chinese consumer-electronics brands propelled a rapid shift toward ultra-compact universal serial bus power-delivery chargers. Models released in 2024 delivered up to 240 W while shrinking volume by 40% relative to silicon equivalents and lowering retail prices by 35%. Anker's GaN Prime line exceeded 1.8 W/cm3 power density, enabling multiprotocol charging for laptops and phones within pocket-sized enclosures. Cost-downs stimulated mainstream uptake across Asia-Pacific and North America, lifting unit volumes that ripple across the gallium nitride semiconductor devices market.

5G Massive-MIMO Macro-Cell Roll-outs Requiring >200 W GaN-on-SiC PAs in Asia and India

Mobile network operators in China, India, and Japan deployed more than 15,000 macro base stations in 2024 using GaN-on-SiC power amplifiers above 3.5 GHz. The switch trimmed power consumption by 25% and stretched coverage by 18%, translating into USD 18 million annual operating expense savings for one leading Japanese carrier. Such economics cement GaN PA design wins and expand addressable revenue across the gallium nitride semiconductor devices market.

Limited 200 mm GaN-on-Si Epi Wafer Supply Chain Bottlenecks

Fewer than 10 qualified suppliers produced 200 mm GaN epitaxial wafers in 2024. Yields sat 15-20% below silicon benchmarks, constraining throughput and sustaining premium pricing. A European Tier-1 automotive supplier recorded a six-month production delay that forced strategic inventory buffers worth EUR 28 million (USD 30.2 million). Bottlenecks weigh on near-term volumes within the gallium nitride semiconductor devices market.

Other drivers and restraints analyzed in the detailed report include:

- Shift to 800 V EV Platforms Driving Bidirectional GaN OBC and DC-DC Adoption

- Weight-Critical More-Electric Aircraft and eVTOL Powertrains Selecting GaN Converters

- Gate Reliability Challenges >175 °C for Automotive Grade-0 Qualification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The power-semiconductor slice of the gallium nitride semiconductor devices market held 55.2% share in 2024 and is projected to compound at 19.1% to 2030. Data-center operators saved USD 2.3 million per facility by upgrading to GaN server power supplies that reached 98.2% efficiency. RF devices followed as 5G massive-MIMO infrastructure and defense radar sustained premium demand.

Maturity signaled a strategic fork. Silicon incumbents such as Infineon expanded automotive-grade GaN MOSFET lines, while RF specialists like Wolfspeed leveraged GaN-on-SiC thermal headroom for >3.5 GHz macro cells. Integrated power-stage providers captured a higher margin by moving beyond discrete sales. The gallium nitride semiconductor devices market, therefore, experiences both consolidation and vertical integration, reinforcing scale advantages.

High-electron-mobility transistors occupied 57.2% revenue in 2024, yet monolithic power ICs outpaced all other categories at 31.1% CAGR. A Chinese smartphone OEM cut the charger bill-of-materials by 18% by replacing discrete switches with a single GaN IC, shrinking part count by 45% and catalyzing volume ramps.

Integration improves electromagnetic compatibility and trims parasitics, benefits that explain why the gallium nitride semiconductor devices market is tilting toward system-in-package designs. Module suppliers address high-power installations, while diode sales remain steady in auxiliary rectification roles.

The 100-650 V corridor kept a 70.3% share in 2024 as it aligns with consumer, data-center, and 48 V industrial rails. Meanwhile, the >650 V band races ahead at 42.2% CAGR, fueled by 800 V propulsion architectures. One premium EV brand slashed 10-80% charge time to 28 minutes using 900 V GaN stages and cut charger mass by 3.2 kg versus SiC.

This transition prompts new isolation and test standards, challenging pure-play suppliers. Nevertheless, the gallium nitride semiconductor devices market rewards those able to validate reliability beyond 650 V, unlocking lucrative automotive value pools.

The GaN Semiconductor Devices Market is Segmented by Device Type (Power Semiconductors, and More), Component (Transistors, and More), Voltage Rating (< 100 V, and More), Wafer Size (2-Inch, and More), Substrate Technology (GaN-On-SiC, and More), Packaging (Surface-Mount, and More), End-User Industry (Automotive and Mobility, and More), and Geography (North America, South America, Europe, Asia-Pacific, and Middle East and Africa).

Geography Analysis

Asia-Pacific commanded 38.2% of 2024 sales and remained the fastest riser at 29.1% CAGR. China's access to gallium, plus state subsidies, allowed Innoscience to operate the world's largest 8-inch GaN-on-Si plant at costs 35% below peers. South Korea's consumer-electronics titans and Japan's automotive majors seeded high-volume anchor customers, sustaining a virtuous cycle of demand and capacity growth.

North America stayed an innovation hotbed. Federal CHIPS grants of USD 35 million helped GlobalFoundries broaden GaN capacity in Vermont. Defense contractors deployed GaN-based phased-array radars that boosted detection range by 42% while trimming power by 18%, showcasing mission-critical gains that flow into the gallium nitride semiconductor devices market.

Europe prioritized premium automotive and industrial use cases. Cambridge GaN Devices raised EUR 30.5 million (USD 33.1 million) for expansion, reflecting investor belief in high-power European niches. A leading German OEM realized 97.8% charger efficiency and 30% component reduction, aligning with EU eco-design directives. Latin America, the Middle East, and Africa presently hold modest shares yet demonstrate promising uptake in telecom and smart-city projects as energy prices and infrastructure buildouts converge.

- Efficient Power Conversion Corporation

- Navitas Semiconductor

- Transphorm Inc.

- Innoscience Technology Co., Ltd.

- MACOM Technology Solutions Holdings, Inc.

- Tagore Technology Inc.

- VisIC Technologies Ltd.

- Cambridge GaN Devices Ltd.

- NexGen Power Systems, Inc.

- Qromis, Inc.

- EPC Space LLC

- Analog Devices, Inc.

- Power Integrations, Inc.

- Ommic SAS

- Wolfspeed GaN Solutions

- Ampleon Netherlands B.V.

- Integra Technologies, Inc.

- RFHIC Corporation

- Sumitomo Electric Device Innovations Inc.

- Infineon Technologies AG

- STMicroelectronics N.V.

- Qorvo Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of 65-240 W USB-C PD GaN Chargers Led by Chinese OEM Road-maps

- 4.2.2 5G Massive-MIMO Macro-Cell Roll-outs Requiring >200 W GaN-on-SiC PAs in Asia and India

- 4.2.3 Shift to 800 V EV Platforms Driving Bidirectional GaN OBC and DC-DC Adoption

- 4.2.4 Weight-Critical More-Electric Aircraft and eVTOL Powertrains Selecting GaN Converters

- 4.2.5 LEO Constellation Satellites Migrating to GaN Ku/Ka-Band SSPAs

- 4.2.6 Japanese and EU Fab Incentives Accelerating GaN Capacity Expansion

- 4.3 Market Restraints

- 4.3.1 Limited 200 mm GaN-on-Si Epi Wafer Supply Chain Bottlenecks

- 4.3.2 Gate Reliability Challenges >175 °C for Automotive Grade-0 Qualification

- 4.3.3 Cost Delta vs. LDMOS in Sub-3.5 GHz Macro PAs in Emerging Markets

- 4.3.4 Fragmented Test/Packaging Ecosystem for E-mode GaN QFN/CSP Packages

- 4.4 Value Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macroeconomic Factors on the market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type

- 5.1.1 Power Semiconductors

- 5.1.2 RF Semiconductors

- 5.1.3 Opto-Semiconductors

- 5.2 By Component

- 5.2.1 Transistors (HEMT/FET)

- 5.2.2 Diodes (Schottky, PiN)

- 5.2.3 Rectifiers

- 5.2.4 Power ICs (Monolithic, Multi-chip)

- 5.2.5 Modules (Half-bridge, Full-bridge)

- 5.3 By Voltage Rating

- 5.3.1 < 100 V

- 5.3.2 100 - 650 V

- 5.3.3 > 650 V

- 5.4 By Wafer Size

- 5.4.1 2-inch

- 5.4.2 4-inch

- 5.4.3 6-inch and Above (incl. 8-inch Pilot)

- 5.5 By Substrate Technology

- 5.5.1 GaN-on-SiC

- 5.5.2 GaN-on-Si

- 5.5.3 GaN-on-Sapphire

- 5.5.4 Bulk GaN

- 5.5.5 650 - 1200 V

- 5.5.6 > 1200 V

- 5.6 By Packaging

- 5.6.1 Surface-Mount (QFN, DFN)

- 5.6.2 Through-Hole (TO-220, TO-247)

- 5.6.3 Chip-Scale Package (CSP)

- 5.6.4 Bare Die

- 5.7 By End-User Industry

- 5.7.1 Automotive and Mobility

- 5.7.1.1 Electric Vehicles

- 5.7.1.2 Charging Infrastructure

- 5.7.2 Consumer Electronics

- 5.7.2.1 Smartphone Fast Chargers

- 5.7.2.2 Laptop and Tablet Chargers

- 5.7.2.3 Gaming Consoles and VR

- 5.7.3 Telecom and Datacom

- 5.7.3.1 5G Base Stations

- 5.7.3.2 Data Center Power

- 5.7.4 Industrial and Energy

- 5.7.4.1 Solar Inverters

- 5.7.4.2 Motor Drives

- 5.7.4.3 Power Supply Units (SMPS)

- 5.7.5 Aerospace and Defense

- 5.7.5.1 Radar Systems

- 5.7.5.2 Electronic Warfare

- 5.7.5.3 Satellite Payloads

- 5.7.6 Medical

- 5.7.6.1 MRI and CT

- 5.7.6.2 Portable Medical Devices

- 5.7.1 Automotive and Mobility

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 United Kingdom

- 5.8.3.3 France

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Rest of Europe

- 5.8.4 Asia-Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 South Korea

- 5.8.4.4 India

- 5.8.4.5 Taiwan

- 5.8.4.6 Rest of Asia-Pacific

- 5.8.5 Middle East and Africa

- 5.8.5.1 Middle East

- 5.8.5.1.1 Saudi Arabia

- 5.8.5.1.2 United Arab Emirates

- 5.8.5.1.3 Turkey

- 5.8.5.1.4 Rest of Middle East

- 5.8.5.2 Africa

- 5.8.5.2.1 South Africa

- 5.8.5.2.2 Rest of Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 Efficient Power Conversion Corporation

- 6.4.2 Navitas Semiconductor

- 6.4.3 Transphorm Inc.

- 6.4.4 Innoscience Technology Co., Ltd.

- 6.4.5 MACOM Technology Solutions Holdings, Inc.

- 6.4.6 Tagore Technology Inc.

- 6.4.7 VisIC Technologies Ltd.

- 6.4.8 Cambridge GaN Devices Ltd.

- 6.4.9 NexGen Power Systems, Inc.

- 6.4.10 Qromis, Inc.

- 6.4.11 EPC Space LLC

- 6.4.12 Analog Devices, Inc.

- 6.4.13 Power Integrations, Inc.

- 6.4.14 Ommic SAS

- 6.4.15 Wolfspeed GaN Solutions

- 6.4.16 Ampleon Netherlands B.V.

- 6.4.17 Integra Technologies, Inc.

- 6.4.18 RFHIC Corporation

- 6.4.19 Sumitomo Electric Device Innovations Inc.

- 6.4.20 Infineon Technologies AG

- 6.4.21 STMicroelectronics N.V.

- 6.4.22 Qorvo Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment