PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850058

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850058

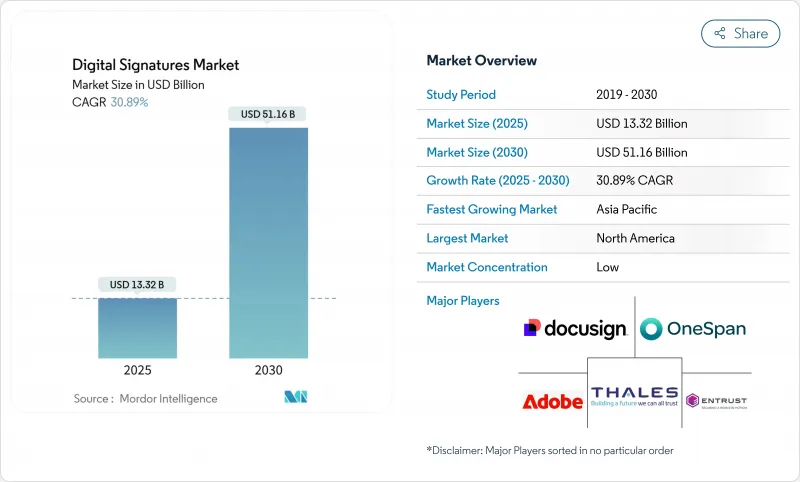

Digital Signatures - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The digital signatures market size stands at USD 13.32 billion in 2025 and is forecast to climb to USD 51.16 billion by 2030, advancing at a 30.89% CAGR.

Sustained momentum comes from stringent global compliance mandates, full-scale enterprise digitization projects, and the looming need for quantum-resistant cryptography. Cloud deployment remains the default architecture, remote work drives soaring transaction volumes, and application programming interface (API) integration turns signatures into an invisible step inside everyday business processes. Vendor differentiation now rests on post-quantum roadmaps and cross-platform interoperability rather than on basic signing features. At the same time, fragmented data-sovereignty regimes and bandwidth constraints in emerging markets temper the otherwise rapid global roll-out of advanced signing technologies.

Global Digital Signatures Market Trends and Insights

Accelerated compliance mandates for qualified e-signatures in EU (eIDAS 2.0)

The eIDAS 2.0 regulation, effective May 2024, obliges every Member State to launch at least one European Digital Identity Wallet within a year and compels private service providers to accept those wallets for strong user authentication. Organizations must shift from TLv5 to TLv6 trust lists by May 2025, prompting accelerated upgrades to signature creation devices and validation services. Qualified electronic signatures become the gold standard, driving investment in Hardware Security Modules (HSMs) and multi-factor authentication. Multinationals with pan-EU operations, therefore, synchronize global signing stacks to EU guidelines to avoid legal exposure. Vendors offering turnkey, wallet-ready solutions gain early-mover advantage as enterprises race to comply.

Mega-scale digitisation programmes in APAC public sector workflows

Governments in China, India, Japan, and Vietnam are fast-tracking paperless governance, propelling digital signature transaction counts across citizen-facing portals. Vietnam's late-2024 surge in digital signatures underscored how public-sector mandates ignite private-sector adoption. India's e-Sign initiative under Digital India shows similar network effects, with eMudhra holding 35% of national certificate issuance. As millions of civil servants transact online, standardized trust frameworks become de facto requirements for suppliers, banks, and insurers. The sudden volume also pressures vendors to deliver low-latency, mobile-first experiences.

Country-specific data-localisation rules hindering cross-border validity

Roughly 100 localisation measures across 40 countries require sensitive data to stay in domestic clouds, fragmenting infrastructure and driving up compliance costs. Digital signature providers must replicate key stores, audit logs, and timestamp services in every regulated jurisdiction while preserving global validation chains. Financial institutions handling multi-currency trade documents feel the burden most, incurring extra latency and audit complexity. Studies show data localisation can weaken 13 of 14 ISO 27002 security controls, undermining threat hunting and crisis response. The resulting overhead slows deployment outside technology-rich, high-margin sectors.

Other drivers and restraints analyzed in the detailed report include:

- Embedded e-signature APIs in enterprise SaaS suites (Microsoft 365, Salesforce)

- Renewal cycle toward post-quantum cryptography certificate stacks

- UX gaps for biometric signatures on low-bandwidth mobile networks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud solutions generated USD 9.06 billion in 2024, translating into 68% of the digital signatures market share. Continued acceleration at a 33.5% CAGR positions cloud to exceed half of the total incremental revenue through 2030. Tight integration with identity-as-a-service platforms, instantaneous feature roll-outs, and elastic scaling resonate with enterprises seeking rapid returns. Cloud providers embed tamper-resistant HSM clusters certified to FIPS 140-3, alleviating past fears about key escrow and multi-tenancy. As a result, procurement teams routinely default to subscription licensing rather than capital expenditure installations.

On-premise deployments endure in defense, core banking, and sovereign-cloud mandates where hardware ownership is non-negotiable. Data-residency statutes in China, Russia, and India elevate local data centers from preference to requirement, ensuring a persistent 32% revenue share for on-premise solutions. During 2025-2030, hybrid architecture emerges as a pragmatic bridge, offloading routine transactions to SaaS yet reserving "qualified" or classified signatures for in-house HSM racks. This dual-track model allows regulated enterprises to tap API-rich ecosystems without forfeiting sovereign control. The digital signatures industry, therefore, sees integrators focusing on unified policy orchestration that spans both environments.

Digital Signatures Market is Segmented by Deployment (On-Premise, Cloud), Offering (Software, Hardware, Services), End-User Industry (BFSI, Government, Healthcare, Oil and Gas, Military and Defense, Logistics and Transportation, and More), Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America's 34% revenue share, worth USD 4.53 billion in 2024, reflects early regulatory clarity under E-SIGN, mature cloud penetration, and a dense ecosystem of ISV and reseller partners. BFSI and technology verticals dominate consumption, but state-level digital-government programs add fresh volume. Case studies show retail banks doubling online loan closures after embedding signing inside mobile apps. The region is also home to leading vendors, securing talent and partnership advantages.

Asia-Pacific is the highest-velocity arena with a 35.5% CAGR to 2030. Mega-government digitisation in India, China, and Japan underpins demand spikes that cascade into private-sector procurement. India's Aadhaar-linked e-Sign lowers identity verification cost per transaction, pushing digital signatures market adoption at grassroots banking and insurance tiers. China's Cybersecurity Law triggers local HSM sourcing, shaping unique supply-chain patterns.

Europe's adoption accelerates following the eIDAS 2.0 rollout. Germany, France, and the United Kingdom head enterprise spending, especially in healthcare, finance, and legal services. The European Digital Identity Wallet promises frictionless cross-border recognition, yet legacy integration remains a hurdle. Vendors equipped with TLv6 trust-list management and remote qualified signature support see growing RFP inclusion.

The Middle East and Africa post healthy mid-teen growth anchored by Gulf Cooperation Council e-government efforts. The United Arab Emirates enforces national trust frameworks that recognize remote signatures, streamlining foreign investor onboarding. South Africa's financial sector adopts cloud solutions despite sporadic power and network constraints, leveraging redundant data centers in Johannesburg and Cape Town.

South America witnesses rising demand, with Brazil, Argentina, and Chile enacting legal recognition statutes. Brazil's CertiSign expands certificate issuance for cross-border trade documents, spurring procurement among exporters. Regional growth still contends with heterogeneous tax and notary regulations, prompting cloud vendors to pre-package compliance templates for Mercosur trade lanes. Across all regions, the digital signatures market benefits from sustained governmental push toward secure digital economies.

- DocuSign Inc.

- Adobe Inc. (Adobe Sign)

- OneSpan Inc.

- Thales Group (SafeNet)

- Entrust Corporation

- Nitro Software Ltd.

- airSlate Inc. (SignNow)

- Dropbox Inc. (HelloSign)

- Box Inc. (SignRequest)

- SIGNiX Inc.

- Ascertia Limited

- GlobalSign GMO

- Signeasy

- PandaDoc Inc.

- RPost Communications Ltd.

- CertiSign Certificadora Digital

- Kofax Ltd.

- Digicert Inc.

- Signicat AS

- Zoho Corporation (Zoho Sign)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated compliance mandates for qualified e-signatures in EU (eIDAS 2.0)

- 4.2.2 Mega-scale digitisation programmes in APAC public sector workflows

- 4.2.3 Embedded e-signature APIs in enterprise SaaS suites (Microsoft 365, Salesforce)

- 4.2.4 Renewal cycle toward post-quantum cryptography certificate stacks

- 4.2.5 ESG-linked push for paperless transactions and Scope-3 carbon reduction

- 4.3 Market Restraints

- 4.3.1 Country-specific data-localisation rules hindering cross-border validity

- 4.3.2 Fragmented global trust-service accreditation regimes

- 4.3.3 UX gaps for biometric signatures on low-bandwidth mobile networks

- 4.3.4 High cost of HSM-backed qualified signatures for SMBs

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Assessment of Macroeconomic Factors Impact

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-premise

- 5.1.2 Cloud

- 5.2 By Offering

- 5.2.1 Software

- 5.2.2 Hardware

- 5.2.3 Services

- 5.3 By End-user Industry

- 5.3.1 BFSI

- 5.3.2 Government

- 5.3.3 Healthcare

- 5.3.4 Oil and Gas

- 5.3.5 Military and Defense

- 5.3.6 Logistics and Transportation

- 5.3.7 Others (Research and Education, Real Estate, Manufacturing, Legal, IT and Telecom)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Chile

- 5.4.2.4 Peru

- 5.4.2.5 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia

- 5.4.4.6 New Zealand

- 5.4.4.7 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 United Arab Emirates

- 5.4.5.1.2 Saudi Arabia

- 5.4.5.1.3 Turkey

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Kenya

- 5.4.5.2.3 Nigeria

- 5.4.5.2.4 Rest of Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Strategic Developments

- 6.2 Market Share Analysis

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 DocuSign Inc.

- 6.4.2 Adobe Inc. (Adobe Sign)

- 6.4.3 OneSpan Inc.

- 6.4.4 Thales Group (SafeNet)

- 6.4.5 Entrust Corporation

- 6.4.6 Nitro Software Ltd.

- 6.4.7 airSlate Inc. (SignNow)

- 6.4.8 Dropbox Inc. (HelloSign)

- 6.4.9 Box Inc. (SignRequest)

- 6.4.10 SIGNiX Inc.

- 6.4.11 Ascertia Limited

- 6.4.12 GlobalSign GMO

- 6.4.13 Signeasy

- 6.4.14 PandaDoc Inc.

- 6.4.15 RPost Communications Ltd.

- 6.4.16 CertiSign Certificadora Digital

- 6.4.17 Kofax Ltd.

- 6.4.18 Digicert Inc.

- 6.4.19 Signicat AS

- 6.4.20 Zoho Corporation (Zoho Sign)

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment