PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850074

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850074

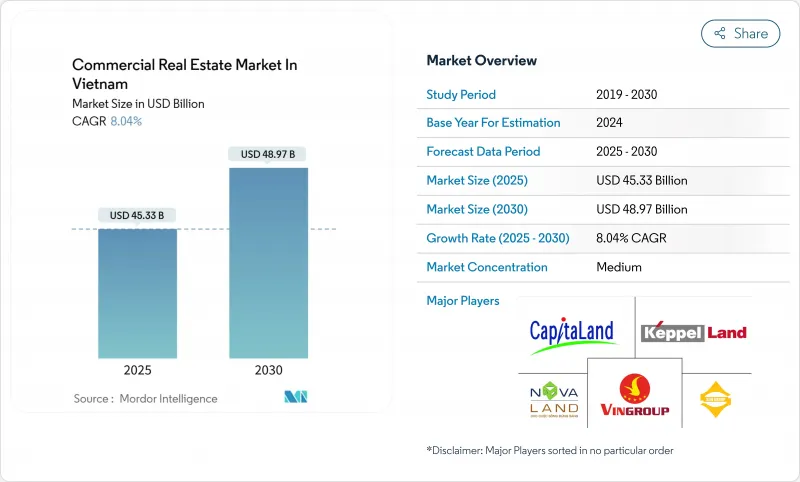

Vietnam Commercial Real Estate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Vietnam commercial real estate market stood at USD 45.33 billion in 2025 and is forecast to expand at an 8.04% CAGR, reaching USD 48.97 billion by 2030.

Healthy capital inflows, accommodative monetary settings, and large-scale infrastructure programs are widening both development and investment pipelines across offices, logistics, hospitality, data centers, and mixed-use assets. Commercial banks have cut lending rates by 0.8 percentage points since early 2025, reducing financing costs for developers and buyers alike. At the same time, government approval of USD 39.4 billion in expressway spending through 2030 and metro construction in Ho Chi Minh City (HCMC) and Hanoi is unlocking transit-oriented development corridors. Rising edge-computing and data-localization requirements are spurring a USD 1.5 billion, 150-MW data-center campus in Binh Duong. Flood risk, construction-material shortages, and hybrid-work adoption temper the outlook, but overall demand remains robust as institutional investors, corporates, and an expanding middle class scale up exposure to professionally managed assets.

Vietnam Commercial Real Estate Market Trends and Insights

Surge in institutional capital into core office assets

Foreign direct investment (FDI) in Vietnam's real estate sector rose 46% year-on-year to USD 2.4 billion in Q1 2025, funnelling mainly into Grade-A offices that command steady USD 55 per sqm monthly rents in HCMC and Hanoi. Investors favor completed, metro-linked towers that already host multinational tenants, locking in predictable cash flows while avoiding construction-cost volatility. January 2025 saw USD 4.33 billion of registered FDI-up 48.6%-underscoring persistent appetite for stabilized CBD properties.

Rising demand for Grade-A industrial & logistics parks

Vietnam's 2023 e-commerce turnover reached USD 19.6 billion, propelling build-to-suit warehouses, cross-border fulfilment hubs, and automation-ready industrial parks. The USD 168 million International Logistics Center in Bac Giang integrates with 20 industrial zones to serve Foxconn and Luxshare. Industrial absorption in HCMC topped 85 hectares in Q3 2024, holding 89% occupancy as manufacturers began shifting to Long An and Ba Ria-Vung Tau.

Persistent hybrid work softening CBD office uptake

Projected net absorption for offices may fall to 50,000 sqm in 2025 versus 88,000 sqm a year earlier as corporates rationalize footprints. Flexible-work hubs are proliferating in emerging centers such as Thu Duc City and Nghe An, reducing demand for premium CBD towers. Smart-building retrofits and shorter lease terms are becoming prerequisites for maintaining occupancy.

Other drivers and restraints analyzed in the detailed report include:

- Expressway & metro build-out lifting land values

- Tourism rebound reviving CBD hotel RevPAR

- Construction-cost inflation & labor shortages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Offices retained the largest 34% slice of the Vietnam commercial real estate market share in 2024, yet logistics assets register the quickest 8.68% CAGR to 2030. Institutional funds channel capital into last-mile hubs, cross-docks, and temperature-controlled facilities, while e-commerce tenants lock in multi-year leases to secure scarce Class-A supply. The Vietnam commercial real estate market size attributable to logistics is expected to approach double-digit billions by the end of the decade, supported by rising free-trade zones and duty-free clusters around Cai Mep port and Long Thanh Airport. CBRE cites 89% industrial-park occupancy in HCMC, prompting new parks across 3,833 ha that target green-tech manufacturers.

Retail assets occupy a mid-teen percentage of value and benefit from international brands and Vietnam's fast-urbanizing consumer base. Hospitality, data-center, and mixed-use developments comprise the "Others" bucket, where integrated townships such as the USD 2 billion Can Gio Port area illustrate scale opportunities. Hilton's forthcoming 14-hotel rollout signals more robust long-stay and mid-scale travel demand. Mixed-use masterplans like the Trump Organization's USD 1.5 billion Hung Yen township blend golf, hospitality, and residential components to capture multiple revenue streams.

The Vietnam Commercial Real Estate Market Report is Segmented by Property Type (Offices, Retail and More), by Business Model (Rental and Sales), by End User (Individuals / Households and More) and by Region (Ho Chi Minh City, Hanoi and More). The Report Offers Market Size and Forecasts in Value (USD) for all the Above Segments.

List of Companies Covered in this Report:

- Vingroup JSC

- CapitaLand (Vietnam) Holdings

- Keppel Land Vietnam

- Sun Group

- Novaland Group

- Mapletree Investments Vietnam

- Nam Long Investment Corporation

- Dat Xanh Group

- Becamex IDC Corporation

- Kinh Bac City Development Holding Corporation

- Frasers Property Vietnam

- Lotte Properties Vietnam

- Gamuda Land Vietnam

- Phat Dat Real Estate Development

- Hung Thinh Land

- BRG Group

- Viglacera Corporation

- An Gia Real Estate Investment

- Cushman & Wakefield Vietnam

- CBRE Vietnam

- JLL Vietnam

- Knight Frank Vietnam

- Colliers Vietnam

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Commercial Real-Estate Buying Trends - Socio-Economic & Demographic Insights

- 4.3 Rental Yield Analysis

- 4.4 Capital-Market Penetration & REIT Presence

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Insights into Real-Estate Tech and Start-ups Active in the Segment

- 4.8 Insights into Existing and Upcoming Projects

- 4.9 Market Drivers

- 4.9.1 Surge in Institutional Capital Allocation to Core Office Assets in Ho Chi Minh City & Hanoi

- 4.9.2 Accelerated Demand for Grade-A Industrial & Logistics Parks Driven by E-Commerce Fulfilment

- 4.9.3 Government-Backed Expressway & Metro Pipeline Lifting Commercial Land Values Along Transit Corridors

- 4.9.4 Re-rating of ESG-Compliant Green Buildings Unlocking Premium Rents from Multinationals

- 4.9.5 Rebound in International Tourism Revitalising CBD Hotel RevPAR in Coastal Cities

- 4.9.6 Data-Localisation Mandates Fueling Edge Data-Centre Campus Development

- 4.10 Market Restraints

- 4.10.1 Persistent Hybrid-Work Adoption Softening CBD Office Net Absorption

- 4.10.2 Elevated Construction Costs & Skilled-Labour Shortages Delaying Project Delivery

- 4.10.3 Monetary Tightening and Rising Cap Rates Compressing Transaction Volumes

- 4.10.4 Heightened Climate-Risk Exposure Raising Insurance Premiums for Coastal Assets

- 4.11 Value / Supply-Chain Analysis

- 4.11.1 Overview

- 4.11.2 Real-Estate Developers & Contractors - Key Quantitative & Qualitative Insights

- 4.11.3 Real-Estate Brokers & Agents - Key Quantitative & Qualitative Insights

- 4.11.4 Property-Management Companies - Key Quantitative & Qualitative Insights

- 4.11.5 Insights on Valuation Advisory and Other Real-Estate Services

- 4.11.6 State of the Building-Materials Industry & Partnerships with Key Developers

- 4.11.7 Insights on Key Strategic Real-Estate Investors / Buyers in the Market

- 4.12 Porter's Five Forces

- 4.12.1 Bargaining Power of Suppliers

- 4.12.2 Bargaining Power of Buyers

- 4.12.3 Threat of New Entrants

- 4.12.4 Threat of Substitutes

- 4.12.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Property Type

- 5.1.1 Offices

- 5.1.2 Retail

- 5.1.3 Logistics

- 5.1.4 Others (Industrial Parks, Hospitality, Mixed-Use)

- 5.2 By Business Model

- 5.2.1 Sales

- 5.2.2 Rental

- 5.3 By End-User

- 5.3.1 Individuals / Households

- 5.3.2 Corporates & SMEs

- 5.3.3 Others (Institutions, Government, NGOs)

- 5.4 By Region

- 5.4.1 Ho Chi Minh City

- 5.4.2 Hanoi

- 5.4.3 Hai Phong

- 5.4.4 Binh Duong

- 5.4.5 Da Nang

- 5.4.6 Rest of Vietnam

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 Vingroup JSC

- 6.4.2 CapitaLand (Vietnam) Holdings

- 6.4.3 Keppel Land Vietnam

- 6.4.4 Sun Group

- 6.4.5 Novaland Group

- 6.4.6 Mapletree Investments Vietnam

- 6.4.7 Nam Long Investment Corporation

- 6.4.8 Dat Xanh Group

- 6.4.9 Becamex IDC Corporation

- 6.4.10 Kinh Bac City Development Holding Corporation

- 6.4.11 Frasers Property Vietnam

- 6.4.12 Lotte Properties Vietnam

- 6.4.13 Gamuda Land Vietnam

- 6.4.14 Phat Dat Real Estate Development

- 6.4.15 Hung Thinh Land

- 6.4.16 BRG Group

- 6.4.17 Viglacera Corporation

- 6.4.18 An Gia Real Estate Investment

- 6.4.19 Cushman & Wakefield Vietnam

- 6.4.20 CBRE Vietnam

- 6.4.21 JLL Vietnam

- 6.4.22 Knight Frank Vietnam

- 6.4.23 Colliers Vietnam

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment