PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850115

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850115

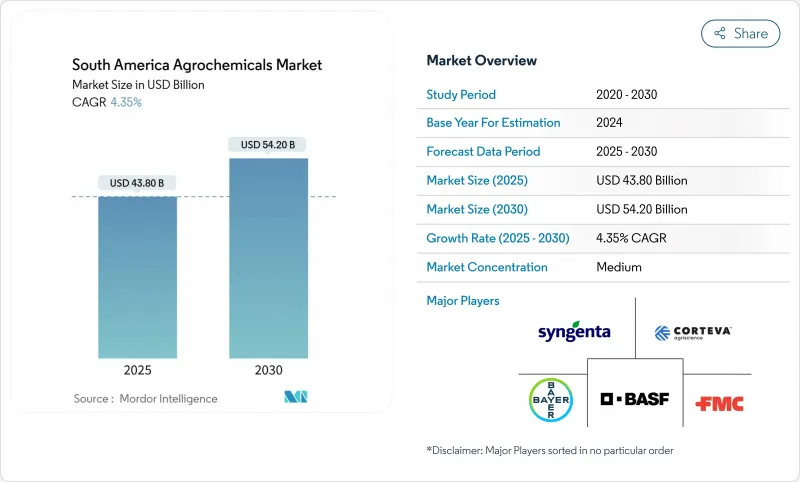

South America Agrochemicals - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The South America Agrochemicals Market size is estimated at USD 43.80 billion in 2025, and is anticipated to reach USD 54.20 billion by 2030, at a CAGR of 4.35% during the forecast period.

Expansion rests on the region's leadership in soybean, corn, and specialty horticulture, reinforced by rising genetically modified crop adoption, precision-application tools, and a rapid shift toward biological solutions. Brazil retains the largest national position and the rest of South America is delivering the fastest growth as they diversify into high-value crops and modern input systems. Fertilizers dominate, reflecting nutrient-depleted soils, while adjuvants post the quickest gains on the back of precision spraying and biological-chemical integration. Competitive intensity is high because the top four suppliers hold the majority share, though a wave of biological start-ups and digital platforms is recalibrating power balances across the South America agrochemicals market. Currency swings, tighter residue rules, and logistics gaps still temper near-term momentum even as long-run acreage expansion and carbon-linked input demand lift the opportunity curve of the South America agrochemicals market.

South America Agrochemicals Market Trends and Insights

GM-crop driven pesticide demand surge

Argentina cleared five new genetically engineered crops in 2024, streamlining approvals to six-month cycles and reinforcing its status as the world's third-largest GM grower with 25 million hectares . Brazil's Intacta2 Xtend trait already spans 30% of national soybean acreage and stimulates demand for herbicide stacks that combine glyphosate, dicamba, and glufosinate. HB4 drought-tolerant wheat commercialized in Argentina is boosting complementary crop-protection formulations tailored for novel herbicide-tolerance packages. Region-wide, biotech expansion pushes agrochemical suppliers to design rotation programs, mitigating resistance while maximizing yield gains. The resulting product bundles strengthen input loyalty, enlarge lifetime value per hectare, and reinforce the premium tier of the South America agrochemicals market.

Precision-ag platforms optimizing chemical rates

Brazil hosts 875 deep-tech firms with agricultural solutions, including AI robotics, microbiology, and remote sensing. Solinftec's solar-powered SOLIX robot autonomously scouts fields to identify weeds and recommends surgical spraying, cutting herbicide volumes while preserving yields. Syngenta's CROPWISE AI platform already maps 70 million ha, centralizing nutrient, pest, and weather data for prescriptive field plans. Hyperspectral sensors now predict nitrogen and potassium levels in real-time, allowing variable-rate fertilizer and stabilizer placement that curbs runoff. Adoption cost hurdles persist, yet mounting labor shortages and input price spikes push growers toward tech-enabled efficiency. These tools tighten the feedback loop between crop status and input need, sustaining the consumption of premium-grade adjuvants, micronutrients, and bio-stimulants within the South America agrochemicals market.

Tighter re-registration and residue limits

Chile imposed stricter maximum residue limits through Decree 47/2024, effective May 2025, raising compliance costs for formulators and exporters. Brazil's updated pesticide law accelerates approvals yet heightens environmental oversight, challenging small registrants. Peru continues to authorize chemistries banned in Europe, fracturing regulatory alignment across Andean trade routes. Wider fungicide resistance in Brazilian soybean pathotypes also presses authorities to revise mode-of-action rotation mandates. Together, these measures lift data-generation expenses, extend market-entry timelines, and may delay newer activities, weighing on the South America agrochemicals market during the transition period.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of soybean and corn acreage

- Biological crop-protection blends adoption

- Commodity-price volatility curbing spend

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizers secured a 42% share of the South America agrochemicals market in 2024, underpinned by nutrient-poor tropical soils and a strategic push to lift oilseed yields, especially in Brazil, where growers spend USD 335/hectare on fertilizer inputs. Pesticides remain the second-largest category, driven by persistent weed and pest pressure in humid climates and by widening herbicide-tolerance stacks in GM crops.

Adjuvants exhibit the fastest trajectory at a 6.0% CAGR through 2030, benefiting from digital spray maps that reward droplet-size optimization and drift reduction. Product innovation now revolves around integrated packages. ICL's launch of nitrogen-fixing inoculants after acquiring Nitro 1000 and Orion's dual-line FA 1500 applicator, able to deliver chemical and biological inputs concurrently, illustrates the convergence trend.

The South America Agrochemicals Market Report is Segmented by Product Type (Fertilizers, Pesticides, and More), by Application (Crop-Based and Non-Crop-Based), and Geography (Brazil, Argentina, and Rest of South America). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Syngenta

- Bayer Crop Science

- BASF SE

- Corteva Agriscience

- Nutrien Ltd

- FMC Corporation

- Yara International ASA

- UPL Limited

- Sumitomo Chemical Co., Ltd.

- ICL Group Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions & Market definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET DYNAMICS

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 GM-crop driven pesticide demand surge

- 4.2.2 Expansion of soybean and corn acreage

- 4.2.3 Subsidized rural credit for agri-inputs

- 4.2.4 Rise of carbon-credit-linked efficiency fertilizers

- 4.2.5 Biological crop-protection blends adoption

- 4.2.6 Precision-ag platforms optimizing chemical rates

- 4.3 Market Restraints

- 4.3.1 Tighter re-registration and residue limits

- 4.3.2 Commodity-price volatility curbing spend

- 4.3.3 Inland logistics bottlenecks on import flows

- 4.3.4 Herbicide resistance escalating switch costs

- 4.4 Technological Outlook

- 4.5 Regulatory Landscape

- 4.6 Porter's Five Force Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers/Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SEGMENTATION

- 5.1 Product Type

- 5.1.1 Fertilizers

- 5.1.1.1 Nitrogenous

- 5.1.1.2 Phosphatic

- 5.1.1.3 Potassic

- 5.1.1.4 Specialty Fertilizers

- 5.1.2 Pesticides

- 5.1.2.1 Herbicides

- 5.1.2.2 Insecticides

- 5.1.2.3 Fungicides

- 5.1.2.4 Bio-pesticides

- 5.1.3 Adjuvants

- 5.1.4 Plant Growth Regulators

- 5.1.1 Fertilizers

- 5.2 Application

- 5.2.1 Crop Based

- 5.2.1.1 Grains and Cereals

- 5.2.1.2 Pulses and Oilseeds

- 5.2.1.3 Fruits and Vegetables

- 5.2.2 Non-Crop Based

- 5.2.2.1 Turf and Ornamental Grass

- 5.2.2.2 Other Non-crop Based

- 5.2.1 Crop Based

- 5.3 Geography

- 5.3.1 Brazil

- 5.3.2 Argentina

- 5.3.3 Rest of South America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Syngenta

- 6.4.2 Bayer Crop Science

- 6.4.3 BASF SE

- 6.4.4 Corteva Agriscience

- 6.4.5 Nutrien Ltd

- 6.4.6 FMC Corporation

- 6.4.7 Yara International ASA

- 6.4.8 UPL Limited

- 6.4.9 Sumitomo Chemical Co., Ltd.

- 6.4.10 ICL Group Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK