PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850127

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850127

Soft Drinks Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

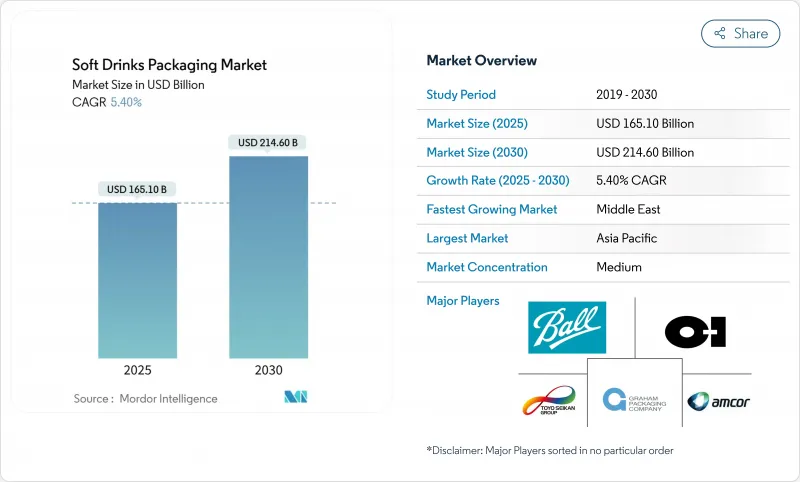

The soft drink packaging market generated USD 165.1 billion in 2025 and is projected to reach USD 214.6 billion by 2030, advancing at a 5.4% CAGR.

Growth reflects rising regulatory demands for recyclability, accelerating brand investments in premium, connected packs, and rapid scale-up of chemical recycling assets. Stricter mandates-such as the European Union's requirement for 30% recycled content in PET bottles by 2030-are forcing redesigns across formats while spurring rPET capacity expansion. Brands are also pivoting toward lightweight bottles and bio-based polymers that lower carbon footprints, a shift intensified by Gen-Z preferences for portion-controlled, visually distinctive packs. Meanwhile, mergers such as the USD 8.4 billion Amcor-Berry Global deal highlight an industry racing to secure scale economies and innovation pipelines. Across regions, Asia-Pacific's urbanizing middle class anchors demand, and the Middle East posts the fastest growth as governments court local beverage production.

Global Soft Drinks Packaging Market Trends and Insights

Surge in PET bottle lightweighting and rPET integration

Regulatory targets and cost pressure are pushing converters to cut resin use, with some Japanese PET bottles now below 20 g-half the traditional weight. High collection rates-90% in Japan versus 75% in Europe-underpin closed-loop economics, while India's Ganesha Ecopet is scaling to 42,000 t rPET to capture 25% of local bottle waste by 2026. Lightweighting trims material cost 15-20% and lowers freight emissions, but demands superior oxygen and CO2 barriers to safeguard taste over shelf life.

Growth of "functional soda" SKUs demanding premium packs

Global functional beverage sales headed toward USD 198.1 billion by 2026 are forcing packs that signal health credentials and enable ingredient storytelling. Gen-Z already drives 38% of category expansion and values transparency, prompting PepsiCo to embed on-pack narratives that justify 20-30% higher packaging spend. Metal cans win favor for their light-blocking and superior gas barriers that protect active compounds without preservatives, sustaining shelf stability and delivering premium cues.

Extended Producer-Responsibility (EPR) fees squeezing margins

Five U.S. states have enacted EPR laws that shift 90% of curbside recycling costs to producers by 2031. Eco-modulated charges tied to design recyclability can push packaging spend up 2-3%, compressing beverage margins while firms retool to lighter, mono-material formats. Navigating multiple state PROs adds administrative load and penalty risk for non-compliance.

Other drivers and restraints analyzed in the detailed report include:

- On-the-go slim-can demand from Gen-Z consumers

- Bottle-to-bottle chemical recycling capacity build-out

- Volatile aluminium premiums and supply bottlenecks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

PET and rPET bottles dominated with 71% revenue in 2024, reflecting a decades-long alignment of cost, clarity, and line compatibility. The soft drink packaging market size for PET equated to USD 117.2 billion in 2025 and is set for stable mid-single-digit expansion as the supply of food-grade rPET improves. Avantium's PEF and Danimer's PHA pipelines underpin a 17.4% CAGR for bioplastics, a niche today but one poised to carve premium categories with superior barrier metrics and lower cradle-to-grave footprints.

Shifting brand targets, net-zero pledges, and recycled-content quotas are hastening rPET uptake even in price-sensitive markets, with India mandating 30% PCR by 2025. Aluminium cans benefit from infinite recyclability and a 76.1% European recycling rate, yet volatile premiums dent converter margins. Glass retains cachet in craft lines but carries logistics penalties, while paperboard innovators scramble to replace PFAS coatings before looming bans take hold.

Bottles commanded 59% of 2024 sales thanks to entrenched blow-molding fleets, broad SKU sizes, and wrap-label real estate. The soft drink packaging market size for bottles is forecast to cross USD 122 billion by 2030, aided by barrier innovations allowing lower-weight preforms. Slim aluminum cans, however, are surging at 8.9% CAGR as Gen-Z ranks portability and Instagram-ready silhouettes above volume.

Retailers embrace the format's shelf efficiencies, and brands glean up to 20% price uplifts on identical fill volumes. Cartons gain share in chilled juice aisles as Tetra Pak shifts to plant-derived HDPE caps. Sachets remain vital in emerging markets, delivering ultra-low-cost entry points even as eco-taxes loom.

The Soft Drinks Packaging Market Report Segments the Industry Into by Material (Plastic, Metal, Glass and More), Product Type (Bottle, Can, Cartons and Boxes), Capacity (Less Than 250 Ml, 251-600 Ml and More), Closure Type (Screw and Sports Caps, Crown and Pull-Tab and More), Soft-Drink Category (Carbonated Soft Drinks, Juices and Nectars and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 43% revenue share stems from surging middle-class purchasing power, dense urban retail, and robust post-consumer PET recovery systems that fuel low-cost rPET loops. Japan's 90% PET collection rate supplies domestic converters, while China subsidizes chemical recycling hubs to beat ambitious recycled-content goals. India's EPR roadmap intensifies demand for bottle-grade rPET, positioning the region as a bellwether for circular-economy scale-up.

The Middle East posts the highest 7.1% CAGR to 2030 as Saudi Arabia and the UAE fast-track local can-sheet rolling lines and beverage plants in pursuit of food-security agendas. Youthful demographics gravitate to energy drinks packaged in sleek cans, reinforcing metal demand despite global aluminium price swings. Government incentives for sustainable industry clusters further spur adoption of rPET preforms in Gulf Cooperation Council filling lines.

North America wrestles with EPR-induced cost headwinds and aluminium sheet tightness, yet benefits from first-mover commercial trials of AI-driven design software that cuts new-SKU timelines. Europe continues to set the regulatory pace: the PPWR's recyclability mandates catalyze investment in mono-material flexible films and advanced depolymerization. South America secures steady gains through Brazil's new ALPLA HDPE recycling plant and rising consumption of functional drinks among urban millennials. Africa, still nascent, observes double-digit volume growth on the back of urban sprawl and expanding cold-chain logistics, though inadequate collection infrastructure tempers rPET uptake.

- Amcor PLC

- Ball Corporation

- Tetra Pak International SA

- Crown Holdings Inc.

- Toyo Seikan Group Holdings Ltd

- Owens-Illinois Inc.

- Graham Packaging Company

- Ardagh Group SA

- CAN-PACK SA

- Refresco Group NV

- CKS Packaging Inc.

- Pacific Can China Holdings

- Berry Global Group Inc.

- Silgan Holdings Inc.

- Huhtamaki Oyj

- Mondi plc

- WestRock Company

- Plastipak Holdings Inc.

- UFlex Ltd.

- Nihon Yamamura Glass Co. Ltd

- Vetropack Holding AG

- Visy Industries

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in PET bottle lightweighting and rPET integration

- 4.2.2 Growth of "functional soda" SKUs demanding premium packs

- 4.2.3 On-the-go slim-can demand from Gen-Z consumers

- 4.2.4 Bottle-to-bottle chemical recycling capacity build-out

- 4.2.5 AI-enabled design platforms cutting packaging development lead-times

- 4.2.6 Carbon-negative PEF and PHA pilots reaching commercial scale

- 4.3 Market Restraints

- 4.3.1 Extended Producer-Responsibility (EPR) fees squeezing margins

- 4.3.2 Volatile aluminium premiums and supply bottlenecks

- 4.3.3 PFAS phase-outs disrupting barrier-coated paperboard

- 4.3.4 Retailer bans on single-use secondary plastics

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Competitive Rivalry

- 4.7 Investment Analysis (CapEx and MandA Trends)

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Material

- 5.1.1 Plastic (PET, rPET, HDPE, Bioplastics)

- 5.1.2 Metal (Aluminium, Steel)

- 5.1.3 Glass

- 5.1.4 Paper and Paperboard

- 5.1.5 Flexible and Compostable Films

- 5.2 By Product Type

- 5.2.1 Bottles

- 5.2.2 Cans

- 5.2.3 Cartons and Aseptic Bricks

- 5.2.4 Pouches and Sachets

- 5.2.5 Bag-in-Box / Dispense Packs

- 5.3 By Capacity

- 5.3.1 Less Than 250 ml

- 5.3.2 251-600 ml

- 5.3.3 601-1 L

- 5.3.4 More Than 1 L Family Packs

- 5.4 By Closure Type

- 5.4.1 Screw and Sports Caps

- 5.4.2 Crown and Pull-tab

- 5.4.3 Snap-on / Press-fit

- 5.4.4 Smart / Connected Closures

- 5.5 By Soft-Drink Category

- 5.5.1 Carbonated Soft Drinks

- 5.5.2 Juices and Nectars

- 5.5.3 Energy and Functional Drinks

- 5.5.4 RTD Tea and Coffee

- 5.5.5 Flavoured and Sparkling Water

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Israel

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 United Arab Emirates

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Amcor PLC

- 6.4.2 Ball Corporation

- 6.4.3 Tetra Pak International SA

- 6.4.4 Crown Holdings Inc.

- 6.4.5 Toyo Seikan Group Holdings Ltd

- 6.4.6 Owens-Illinois Inc.

- 6.4.7 Graham Packaging Company

- 6.4.8 Ardagh Group SA

- 6.4.9 CAN-PACK SA

- 6.4.10 Refresco Group NV

- 6.4.11 CKS Packaging Inc.

- 6.4.12 Pacific Can China Holdings

- 6.4.13 Berry Global Group Inc.

- 6.4.14 Silgan Holdings Inc.

- 6.4.15 Huhtamaki Oyj

- 6.4.16 Mondi plc

- 6.4.17 WestRock Company

- 6.4.18 Plastipak Holdings Inc.

- 6.4.19 UFlex Ltd.

- 6.4.20 Nihon Yamamura Glass Co. Ltd

- 6.4.21 Vetropack Holding AG

- 6.4.22 Visy Industries

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment