PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850197

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850197

Female Contraceptives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

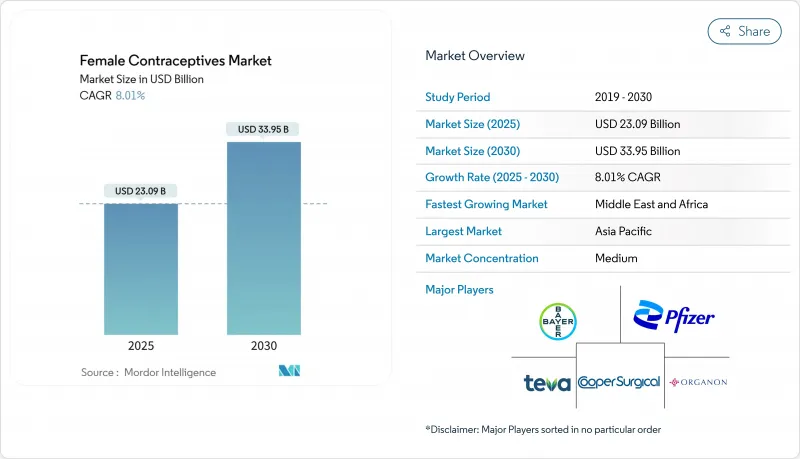

The female contraceptive market is valued at USD 23.09 billion in 2025 and is forecast to reach USD 33.95 billion by 2030, posting an 8.01% CAGR.

Accelerated demand for non-hormonal methods, rapid digital health uptake, and supportive policy measures are steering expansion. The February 2025 FDA approval of MIUDELLA, the first new copper intrauterine system in four decades, validates commercial momentum for hormone-free options. Simultaneously, direct-to-consumer telehealth platforms are widening access, while legal scrutiny of certain hormonal products is nudging users toward safer profiles. Intensifying R&D in low-cost implants and biodegradable devices is opening new addressable populations, particularly in emerging economies. Together, these forces have created a resilient growth path for the female contraceptive market.

Global Female Contraceptives Market Trends and Insights

Growing Preference for Advanced and Innovative Contraceptives

Momentum for hormone-free contraception is accelerating. MIUDELLA received FDA clearance in February 2025, introducing a lower-copper IUD that maintains 99% efficacy while reducing bleeding and pain. Clinical pipelines support the trend, with Ovaprene's Phase 3 trial read-out expected in 2025, combining barrier action and local drug delivery. R&D is targeting polymer coatings and alloy modifications to ease insertion and limit adverse events. The value proposition resonates with women seeking effective yet endocrine-neutral options, shifting demand away from legacy hormonal products. Device makers are therefore allocating larger capital budgets to copper and polymer-based platforms, signalling sustained expansion for this segment of the female contraceptive market.

Government and Market-Player Initiatives for Awareness and Access

Public-private coalitions are narrowing the contraceptive funding deficit. During the 2024 UN General Assembly, donors pledged USD 350 million toward the global contraceptive financing gap, projected at USD 1.5 billion by 2030. The Gates Foundation is contributing USD 280 million annually for innovative technologies and community programs through 2030. Early results are evident in Uganda, where integrated youth reproductive-health campaigns unexpectedly boosted uptake among women aged 25-49 years. Such commitments underpin long-term growth across the female contraceptive market, particularly in resource-limited regions.

Religious, Social and Ethical Issues for Contraceptive Adoption

Cultural norms restrict uptake in several regions. The Family Planning Policy Atlas MENA 2023 indicates that 15% of women aged 15-49 in the Middle East and North Africa still have unmet contraceptive needs due to social constraints. A 2025 Ethiopian study found rural women 53% less likely to use LARCs than urban peers. In the United States, proposed policy shifts under Project 2025 could curtail free emergency contraception for 48 million users. Such headwinds demand culturally nuanced outreach to sustain the female contraceptive market trajectory.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Trend of Tele-Prescribing and Telehealth

- Investment by Market Players in Low-Cost Implants

- Product Liability Litigation and Side-Effect Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Devices held 68.4% of female contraceptive market share in 2024, anchored by intrauterine systems that deliver 99% efficacy alongside low maintenance. MIUDELLA showcases the appetite for innovations that cut copper load yet preserve effectiveness. The segment benefits from sustained investments in polymer coatings that reduce bleeding, broadening acceptance among first-time users. Contraceptive drugs, while smaller, are rising at an 8.1% CAGR through 2030 as formulators refine dosing and extend release profiles. The first OTC progestin pill has expanded retail reach, positioning oral agents for faster gains inside the female contraceptive market size.

Advanced vaginal rings and non-hormonal candidates like Ovaprene are poised to open new sub-segments. Drug developers are leveraging sustained-release matrices to shorten dosing gaps and improve adherence. Together, these innovations are expected to close the convenience gap with devices while retaining pharmacological control. Competitive intensity is therefore increasing as firms straddle both modalities within the female contraceptive market.

Combined estrogen-progesterone products accounted for 51.2% revenue in 2024. Their long clinical history and predictable bleeding patterns reinforce physician preference. However, progesterone-only options are expanding at an 8.8% CAGR, driven by safety for women with estrogen contraindications and emerging prolonged-release injectables. Sayana Press distribution partnerships aim to supply 320 million doses to low-income markets. That plan could lift the female contraceptive market size in underserved areas.

Research into non-hormonal pathways continues, propelled by demand for side-effect-free contraception. Early copper-alloy devices and spermicidal barriers represent tangible progress. These alternatives give manufacturers scope to hedge against liability exposure while diversifying offerings in the female contraceptive market.

The Female Contraceptives Market Report is Segmented by Product Category (Contraceptive Drugs and Contraceptive Devices), Hormone Type (Estrogen-Only, Progestrone-Only, and More), Duration of Action (Short-Acting Methods and LARC), Age Group (15-19 Years and More), Distribution Channel (Hospital Pharmacies and More), End-User (Home and Clinical Use), and Geography. The Market and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the female contraceptive market with 31.60% share in 2024. Government-backed family-planning campaigns, falling fertility rates, and the rise of women's digital health ecosystems underpin leadership. China and India supply scale, while Japan and South Korea broaden uptake of LARCs among late-marrying populations. Telehealth penetration is growing quickly, with the women's digital health sector forecast to expand at 20.54% CAGR to 2034.

North America ranks second aided by mature insurance coverage and regulatory flexibility. Pharmacist prescribing authority has multiplied access points, benefiting rural users. Contraceptive deserts persist for 19 million US women, but telehealth and OTC options are gradually shrinking gaps in the female contraceptive market. Europe exhibits strong reimbursement yet heterogeneity in preferred methods. Northern markets tend toward LARCs while Southern Europe maintains oral dominance.

The Middle East and Africa region is the fastest-growing with a 9.30% CAGR to 2030. Algeria and Tunisia showcase supportive legal frameworks. Merck for Mothers has reached 8.3 million African women through mobile information services. The UAE exemplifies commercial promise as its contraceptive device segment is set to double between 2022 and 2030. Social norms still restrain adoption in conservative areas, yet rising urbanization and education catalyze progressive attitudes that favour female contraceptive market expansion.

- Bayer

- Organon

- Pfizer

- The Cooper Companies

- Teva Pharmaceutical Industries

- Agile Therapeutics Inc.

- Viatris

- Lupin Pharmaceuticals Ltd.

- Mayer Laboratories

- Amneal Pharmaceuticals

- Reckitt Benckiser Group

- Johnson & Johnson

- Chemring Group plc (AngelCare)

- Mona Lisa

- Pregna International Ltd.

- Glenmark Pharmaceuticals

- DKT International

- Gedeon Richter Polska Sp. z o.o.

- HLL Lifecare Ltd.

- Cupid Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Preference for Advanced and Innovative Contraceptives Such as Hormone-Free Copper IUDs

- 4.2.2 Government and Market Players Initiatives To Increase Awaarenss and Access of Feamle Contraceptives

- 4.2.3 Increasing Trend of Tele-Prescribing and Tele-health

- 4.2.4 Investment by Market Players in Low-Cost Implants

- 4.2.5 HPV-Linked Cancer Risk Awareness Accelerating Barrier-Method Adoption

- 4.2.6 Regulatory Green-Light for Over-The-Counter (OTC) Daily Oral Contraceptive Pills

- 4.3 Market Restraints

- 4.3.1 Religious, Social and Ethical Issues for Adoption of Various Contraceptives Such as IUDs etc.

- 4.3.2 Product Liability Litigation and Risks od Side Effects such as Hormonal Pills/ Implants

- 4.3.3 Regulatory Challenges Coupled with Limited Insurance Coverage

- 4.3.4 Supply-Chain Fragility for Key Hormonal APIs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value-USD)

- 5.1 By Product Category

- 5.1.1 Contraceptive Drugs

- 5.1.1.1 Oral Contraceptives

- 5.1.1.1.1 Combined Pills

- 5.1.1.1.2 Progestin-Only Pills

- 5.1.1.2 Contraceptive Injections

- 5.1.1.3 Topical Contraceptives

- 5.1.1.4 Spermicides

- 5.1.2 Contraceptive Devices

- 5.1.2.1 Female Condoms

- 5.1.2.2 Diaphragms & Cervical Caps

- 5.1.2.3 Vaginal Rings

- 5.1.2.4 Contraceptive Sponges

- 5.1.2.5 Sub-Dermal Implants

- 5.1.2.6 Intra-Uterine Devices (IUD)

- 5.1.2.6.1 Copper IUDs

- 5.1.2.6.2 Hormonal IUDs

- 5.1.1 Contraceptive Drugs

- 5.2 By Hormone Type

- 5.2.1 Estrogen-Only

- 5.2.2 Progesterone-Only

- 5.2.3 Combined (E+P)

- 5.3 By Duration of Action

- 5.3.1 Short-Acting Methods

- 5.3.2 Long-Acting Reversible Contraceptives (LARC)

- 5.4 By Age Group

- 5.4.1 15-19 Years

- 5.4.2 20-29 Years

- 5.4.3 30-39 Years

- 5.4.4 40+ Years

- 5.5 By Distribution Channel

- 5.5.1 Hospital Pharmacies

- 5.5.2 Retail Pharmacies

- 5.5.3 Online and DTC Platforms

- 5.5.4 Community / Fertility Clinics

- 5.6 By End-User Setting

- 5.6.1 Home Use

- 5.6.2 Clinical Use

- 5.7 Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 Europe

- 5.7.2.1 Germany

- 5.7.2.2 United Kingdom

- 5.7.2.3 France

- 5.7.2.4 Italy

- 5.7.2.5 Spain

- 5.7.2.6 Rest of Europe

- 5.7.3 Asia-Pacific

- 5.7.3.1 China

- 5.7.3.2 Japan

- 5.7.3.3 India

- 5.7.3.4 Australia

- 5.7.3.5 South Korea

- 5.7.3.6 Rest of Asia-Pacific

- 5.7.4 Middle East and Africa

- 5.7.4.1 GCC

- 5.7.4.2 South Africa

- 5.7.4.3 Rest of Middle East and Africa

- 5.7.5 South America

- 5.7.5.1 Brazil

- 5.7.5.2 Argentina

- 5.7.5.3 Rest of South America

- 5.7.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Bayer AG

- 6.4.2 Organon & Co.

- 6.4.3 Pfizer Inc.

- 6.4.4 CooperSurgical Inc.

- 6.4.5 Teva Pharmaceutical Industries Ltd.

- 6.4.6 Agile Therapeutics Inc.

- 6.4.7 Viatris

- 6.4.8 Lupin Pharmaceuticals Ltd.

- 6.4.9 Mayer Laboratories Inc.

- 6.4.10 Amneal Pharmaceuticals LLC

- 6.4.11 Reckitt Benckiser Group plc

- 6.4.12 Johnson & Johnson (ETHICON)

- 6.4.13 Chemring Group plc (AngelCare)

- 6.4.14 Mona Lisa NV

- 6.4.15 Pregna International Ltd.

- 6.4.16 Glenmark Pharmaceuticals

- 6.4.17 DKT International

- 6.4.18 Gedeon Richter Polska Sp. z o.o.

- 6.4.19 HLL Lifecare Ltd.

- 6.4.20 Cupid Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment