PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850303

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850303

Dry Beans - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

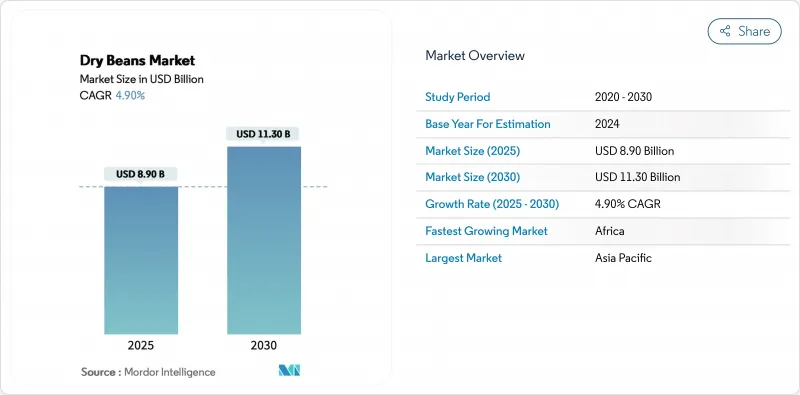

The global dry beans market, valued at USD 8.9 billion in 2025, is projected to reach USD 11.3 billion by 2030, registering a CAGR of 4.9%.

The market expansion is attributed to increasing demand for plant-based proteins, heightened health consciousness, and the agricultural advantages of beans as nitrogen-fixing crops. Investments in high-moisture extrusion technology, protein extraction methods, and gene-edited varieties are facilitating new industrial applications while strengthening climate resilience. Market growth is further supported by the expansion of pulse-crop rotations and tariff reductions in major consuming nations, complemented by increased consumption among vegan, vegetarian, and flexitarian populations. Despite challenges from climate-induced yield variations and disparate mechanization levels, the dry beans market maintains its significance as both a traditional food staple and a functional ingredient in modern food applications.

Global Dry Beans Market Trends and Insights

Rising Global Adoption of Vegan and Flexitarian Diets

The consumption of plant-forward foods continues to expand beyond traditional vegetarian consumer segments. Consumers select legumes over meat products due to their protein content, cholesterol-free nutritional profile, and environmental benefits. Dry beans contain 20-45% protein and significant fiber content, attracting health-conscious urban consumers who demonstrate a willingness to pay premium prices for organic and quick-cook varieties. Manufacturers are increasing their retail presence through convenient microwave-ready pouches and flavored bean snacks. E-commerce and direct-to-consumer distribution channels enhance product visibility among younger consumers. The food service industry's integration of bean-based dishes in their menus facilitates the mainstream adoption of plant-rich meals.

Expanding Pulse-Crop Rotations Across the Globe

Farmers in Canada, the United States, and Australia are transitioning from cereal-only rotations to diversified systems incorporating dry beans, chickpeas, and lentils. The nitrogen-fixing properties of these crops enable farmers to reduce synthetic fertilizer use by 50-100 kg/ha, decreasing costs and lowering nitrous oxide emissions by up to 90%. Government support through cost-share programs for pulse inoculants and cover-crop insurance further encourages this transition. The practice increases soil organic matter content, improving water retention and yield stability for subsequent wheat and barley crops. This rotation system benefits processors by expanding supply while reducing chemical residues, facilitating compliance with European and Japanese residue-limit regulations.

Pest and Viral Disease Vulnerability Raising Farm-Gate Losses

Disease pressures from bacterial blight, root rots, and Bean common mosaic virus result in yield reductions of 15-25% across tropical regions. The insufficient diagnostic laboratory infrastructure impedes the timely detection and implementation of integrated pest management protocols. Agricultural producers utilize fungicide applications, which increase operational costs and present residue compliance issues for European market access. Despite the ongoing development of disease-resistant cultivars by seed companies, rapid pathogen mutations necessitate continuous varietal improvements. Processing operations encounter operational inefficiencies in optical sorting systems and increased rework expenses due to variations in raw material specifications and moisture parameters.

Other drivers and restraints analyzed in the detailed report include:

- Import-Tariff Cuts on Plant Proteins in Key Consuming Nations

- On-Farm Carbon-Credit Monetization for Nitrogen-Fixing Beans

- Yield Volatility from Extreme Weather Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Geography Analysis

Asia-Pacific held a 47% share of the dry beans market in 2024, driven by China's production capacity and India's consumption patterns. China produced 706.5 million metric tons of total grains in 2024, reflecting its focus on agricultural self-sufficiency. India experienced a 90% increase in pulse imports due to domestic supply shortages and changing dietary preferences, while reduced tariffs facilitated increased North American exports. In Myanmar, manual bean harvesting remains prevalent, with women workers facing potential displacement from increasing mechanization. Australia projects a 22% increase in pulse production in 2025, supported by favorable farm-gate prices and increased chickpea cultivation.

Africa demonstrates the highest growth rate with a CAGR of 4.2% through 2030. The African Bean Consortium implements marker-assisted selection to develop disease-resistant cultivars in response to anthracnose outbreaks affecting 100 million dependents. Uganda's Yellow Star Produce introduced a high-protein composite flour to address child malnutrition, showing progress in local value addition. Kenya works with CGIAR on genome sequencing to accelerate breeding for heat tolerance. Tanzania and Ethiopia report gradual yield improvements from conservation-agriculture initiatives, despite some drought-affected areas. Minor challenges persist regarding preparation time and digestive comfort concerns.

South America exhibits divergent patterns. Brazil projects bean production of 3.4 million metric tons in 2025, representing a 9.3% increase due to expanded first-crop area and yields of 880 kg/ha. Argentina experienced substantial losses with frost damage impacting 80% of bean fields in 2024, reducing alubia exports. Mexico achieved production of 856,000 metric tons, supported by PROSEBIEN's price guarantee of USD 1.41/kg (MX 27/kg) and elite seed distribution. North America leverages mechanization and rail infrastructure to supply domestic canners and Asian processors, while Europe maintains its position as a premium market specializing in organic production, with emphasis on traceability and climate-smart practices.

- Market Overview

- Market Drivers

- Market Restraints

- Value / Supply-Chain Analysis

- Regulatory Landscape

- Technological Outlook

- PESTLE Analysis

- List of Stakeholders

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Global Adoption of Vegan and Flexitarian Diets

- 4.2.2 Expanding Pulse-Crop Rotations Across the Globe

- 4.2.3 Import-Tariff Cuts on Plant Proteins in Key Consuming Nations

- 4.2.4 On-Farm Carbon-Credit Monetization for Nitrogen-Fixing Beans

- 4.2.5 Development of Gene-edited Drought-Tolerant Cultivars

- 4.2.6 Growth of Pulse-Based Meat Analog Processing Capacity

- 4.3 Market Restraints

- 4.3.1 Pest and Viral Disease Vulnerability Raising Farm-Gate Losses

- 4.3.2 Yield Volatility from Extreme Weather Cycles

- 4.3.3 Slow Mechanization in Smallholder-Dominated Regions

- 4.3.4 Export-Price Swings Linked to Currency Shocks

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 PESTLE Analysis

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Geography (Production Analysis (Volume), Consumption Analysis (Volume and Value), Import Analysis (Volume and Value), Export Analysis (Volume and Value), and Price Trend Analysis)

- 5.1.1 North America

- 5.1.1.1 United States

- 5.1.1.2 Mexico

- 5.1.2 Europe

- 5.1.2.1 Russia

- 5.1.2.2 Italy

- 5.1.2.3 France

- 5.1.2.4 Germany

- 5.1.3 Asia-Pacific

- 5.1.3.1 China

- 5.1.3.2 India

- 5.1.3.3 Myanmar

- 5.1.3.4 Australia

- 5.1.4 South America

- 5.1.4.1 Brazil

- 5.1.4.2 Argentina

- 5.1.5 Middle East

- 5.1.5.1 United Arab Emirates

- 5.1.5.2 Turkey

- 5.1.5.3 Iran

- 5.1.6 Africa

- 5.1.6.1 Tanzania

- 5.1.6.2 Uganda

- 5.1.6.3 Kenya

- 5.1.6.4 Egypt

- 5.1.1 North America

6 Competitive Landscape

- 6.1 List of Stakeholders

7 Market Opportunities and Future Outlook