PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850309

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850309

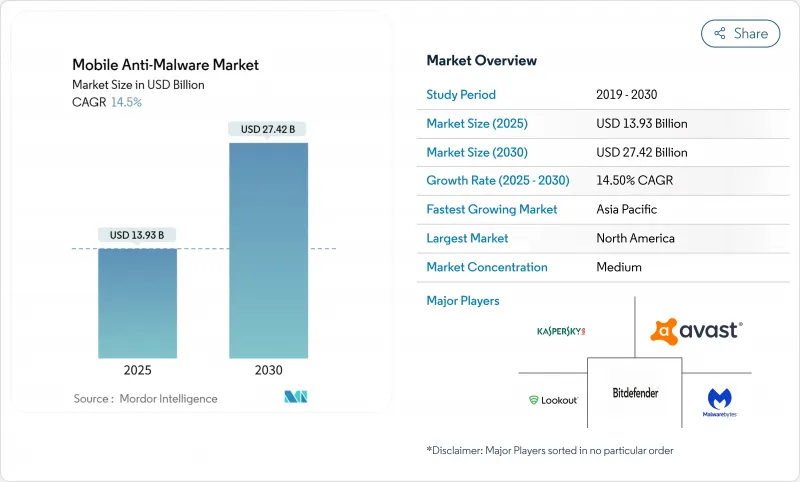

Mobile Anti-Malware - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The mobile anti-malware market size stands at USD 13.93 billion in 2025 and is projected to reach USD 27.42 billion by 2030, reflecting a 14.5% CAGR.

Rapid enterprise digitization, generative-AI-driven malware creation, and zero-trust mandates have turned mobile endpoints into primary attack surfaces for threat actors. Large organizations now treat mobile security as core infrastructure, investing in behavioral analytics that detect malicious intent rather than relying on legacy signature scans. Cloud-delivered threat intelligence, geopolitical vendor restrictions, and new device-embedded AI chips also influence adoption patterns, giving vendors with strong research pipelines and managed-service offerings a clear advantage in the mobile anti-malware market.

Global Mobile Anti-Malware Market Trends and Insights

Exploding Mobile-Specific Malware Variants Post-Generative-AI Era

Generative AI tooling now automates the creation of polymorphic code that mutates on each installation, producing 560,000 unique mobile threats every day in 2025. These campaigns blend code obfuscation with GAN-generated phishing screens that mimic trusted apps on both public and private stores. Signature databases can no longer keep pace, prompting vendors to embed device-side machine learning models that score behavior in milliseconds. Providers that combine cloud-scale correlation with on-device heuristics are gaining enterprise preference because they identify intent before execution. This structural shift places continuous R&D and data-engineering capacity at the center of competitive advantage in the mobile anti-malware market.

BYOD 2.0 and Hybrid Work Driving Corporate Demand

Corporate mobility has evolved from convenience to mission-critical access. In 2024, 84% of large North American firms lifted mobile security budgets to secure employee-owned devices that now handle CRM, ERP, and confidential data workflows. BYOD 2.0 policies prescribe runtime monitoring of applications, network calls, and hardware state, closing gaps left by conventional MDM tools. Security teams prefer consolidated suites that apply one policy across phones, laptops, and tablets, which strengthens demand for integrated platforms. As a result, premium subscription tiers that bundle threat hunting and automated response drive revenue resilience in the mobile anti-malware market.

Persistently Low Consumer Willingness to Pay for Mobile AV

Retails users view built-in protections as adequate and often ignore premium tiers that lack visible utility. Conversion rates on freemium apps stay in single digits even during high-profile breach cycles, limiting revenue scalability outside enterprise contracts. Vendors experiment with ad-supported versions, identity-protection bundles, and family plans, yet monetization remains challenging. The gap places a ceiling on consumer revenue, making the enterprise segment pivotal for long-term growth in the mobile anti-malware market.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Mobile Payment Ecosystems in Emerging Economies

- Regulatory Mandates for Zero-Trust on Employee-Owned Devices

- OS-Level Security Hardening Shrinking Threat Surface

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Android retained 60.1% of mobile anti-malware market share in 2024 due in large part to its vast installed base and lower average device cost. At the same time, iOS units are growing at a 15.5% CAGR, supported by hardware attestation and stricter code-signing controls that simplify compliance in regulated sectors. The mobile anti-malware market size for iOS endpoints is projected to almost double by 2030 as hospital groups, insurers, and financial institutions standardize on Apple devices to lower breach-response expenses. Android remains essential in high-growth economies where value phones dominate, so vendors position AI-powered behavioral engines to offset fragmentation and inconsistent patching.

Enterprises increasingly compare total cost of ownership rather than purchase price alone. Security leaders note that fewer critical incidents on iOS translate into lower forensics spending and downtime. However, Android's open ecosystem spurs innovation in ruggedized devices and specialized toolsets for logistics and field services, ensuring steady demand for next-generation protection agents. Niche operating systems-mainly hardened Linux builds for the defense sector-hold marginal volume yet command high per-seat pricing due to strict accreditation requirements.

On-premise installations accounted for 70.8% of the mobile anti-malware market size in 2024 because many banks and public agencies still store telemetry inside national borders. Nevertheless, cloud subscriptions are accelerating at 16.2% CAGR as boards approve security-as-operating-expenditure budgets that scale with device counts. Large enterprises cite 40% lower administrative overhead once signature updates, model retraining, and threat-intelligence feeds shift to vendor-managed clouds.

Carrier-grade network connectivity and edge PoPs further reduce latency, making cloud consoles viable for always-on validation even under poor Wi-Fi conditions. Vendors assure compliance via regional datacenters and granular data-retention policies. As a result, hybrid rollouts mixing on-prem for crown-jewel assets with cloud for remote staff are now standard. This transition unlocks incremental revenue because customers expand license volumes rather than perform one-off hardware refreshes.

The Mobile Anti-Malware Market Report is Segmented by Operating System (Android, IOS, and Others), Deployment Mode (On-Premise and Cloud), Solution Type (Stand-Alone Mobile Antivirus Apps, Integrated Endpoint-Protection Suites, and More), End User (Enterprises and Consumers / Individuals), Industry Vertical (BFSI, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 38.1% of 2024 revenue. This lead stems from large enterprise budgets, established mobility programs, and stringent laws such as the U.S. DOJ data-transfer safeguards that require continuous risk scoring on every endpoint. Canadian banks comply with OSFI-B-13, further cementing demand for certified platforms capable of reporting device posture to regulators. Local vendors also benefit from geopolitical screening that sidelines certain foreign suppliers, reallocating spending toward trusted domestic ecosystems.

Asia-Pacific is the fastest-growing region with a projected 14.9% CAGR to 2030. Cashless commerce, super-app ecosystems, and mobile-first workforces expand the total device pool faster than in mature markets. Enterprises in India, Indonesia, and Vietnam adopt threat-defense agents to satisfy payment-security mandates, while Japanese and Australian organizations upgrade to meet zero-trust guidelines. Regional channel partners bundle managed detection services with connectivity plans, accelerating outreach into mid-market enterprises.

Europe ranks third by revenue, yet remains pivotal because GDPR fines link data breaches to material financial penalties. Multinationals demand local data centers and strict contractual clauses on data export, encouraging vendors to open EU-based threat-intelligence nodes. In Southern Europe and the Middle East, uptake increases as 5G rollouts push mobile workflows deeper into oil, logistics, and smart-city projects. Latin America follows similar patterns, though macroeconomic volatility keeps some deployments in pilot phases rather than full production.

- AO Kaspersky Lab

- Avast Software

- Bitdefender

- Lookout

- Malwarebytes

- McAfee

- Sophos

- Broadcom (Symantec)

- Trend Micro

- ESET

- Check Point Software

- CrowdStrike

- Cisco Secure Endpoint

- Quick Heal Technologies

- Zimperium

- F-Secure

- NortonLifeLock

- Panda Security

- Qihoo 360

- Tencent Mobile Manager

- Dr.Web

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Exploding mobile-specific malware variants post-Generative-AI era

- 4.2.2 BYOD 2.0 and hybrid-work driving corporate demand

- 4.2.3 Expansion of mobile payment ecosystems in emerging economies

- 4.2.4 Regulatory mandates for zero-trust on employee-owned devices

- 4.2.5 Rise of "app-clone" supply-chain attacks in 3rd-party Android stores

- 4.2.6 Proliferation of on-device AI security chips enabling premium, real-time scanning

- 4.3 Market Restraints

- 4.3.1 Persistently low consumer willingness to pay for mobile AV

- 4.3.2 OS-level security hardening shrinking threat surface

- 4.3.3 Geopolitical distrust of foreign cybersecurity vendors

- 4.3.4 Privacy-centric OS features reducing AV visibility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Operating System

- 5.1.1 Android

- 5.1.2 iOS

- 5.1.3 Others

- 5.2 By Deployment Mode

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Solution Type

- 5.3.1 Stand-alone Mobile Antivirus Apps

- 5.3.2 Integrated Endpoint-Protection Suites

- 5.3.3 Security-as-a-Service (SECaaS) for Mobile

- 5.4 By End User

- 5.4.1 Enterprises

- 5.4.2 Consumers / Individuals

- 5.5 By Industry Vertical

- 5.5.1 BFSI

- 5.5.2 Healthcare

- 5.5.3 IT and Telecom

- 5.5.4 Government and Defense

- 5.5.5 Education

- 5.5.6 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 Germany

- 5.6.2.2 United Kingdom

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 Japan

- 5.6.3.3 India

- 5.6.3.4 South Korea

- 5.6.3.5 Australia

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Egypt

- 5.6.5.2.3 Nigeria

- 5.6.5.2.4 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 AO Kaspersky Lab

- 6.4.2 Avast Software

- 6.4.3 Bitdefender

- 6.4.4 Lookout

- 6.4.5 Malwarebytes

- 6.4.6 McAfee

- 6.4.7 Sophos

- 6.4.8 Broadcom (Symantec)

- 6.4.9 Trend Micro

- 6.4.10 ESET

- 6.4.11 Check Point Software

- 6.4.12 CrowdStrike

- 6.4.13 Cisco Secure Endpoint

- 6.4.14 Quick Heal Technologies

- 6.4.15 Zimperium

- 6.4.16 F-Secure

- 6.4.17 NortonLifeLock

- 6.4.18 Panda Security

- 6.4.19 Qihoo 360

- 6.4.20 Tencent Mobile Manager

- 6.4.21 Dr.Web

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment