PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850334

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850334

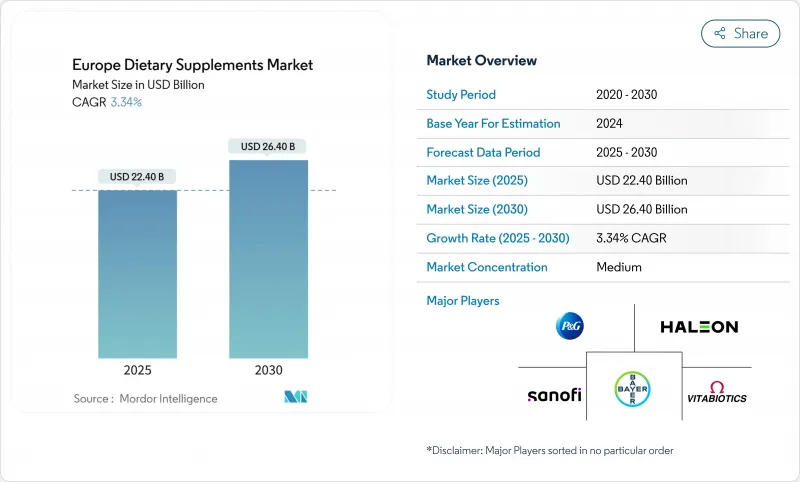

Europe Dietary Supplements - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The European Dietary Supplements market is projected to grow from USD 22.40 billion in 2025 to USD 26.40 billion by 2030, at a CAGR of 3.34%.

Women, the largest consumer group, are driving strong demand for synthetic/ fermentation-derived supplements. While the primary focus remains on enhancing immunity, online retail is swiftly emerging as a dominant distribution channel. Germany currently holds the largest market share, but Poland is poised for the quickest growth through 2030, fuelled by a burgeoning interest in plant-based and personalized nutrition solutions. Furthermore, the European regulatory environment strengthens the market by elevating quality standards and benefiting companies that meet compliance requirements. In 2024, the European Union implemented mandatory labeling requirements for dietary supplements to enhance quality control and consumer protection. As per the regulations the companies must adhere to these labeling standards to maintain their market access in the EU. These regulations mandate the inclusion of unique identification codes for supply chain traceability, detailed ingredient disclosures, manufacturer details, and potential contraindications. As a result, counterfeit activities have seen a significant decline, consumer trust has been reinforced, and brand credibility has been enhanced in the European dietary supplements market.

Europe Dietary Supplements Market Trends and Insights

Preventive healthcare trends are driving regular supplement consumption

European households are now making supplements a staple in their daily preventive healthcare routines, moving from occasional to regular use. Spending on preventive health is outpacing overall healthcare expenditures. Countries like Germany, France, and the Netherlands are emphasizing immunization, nutrition counseling, and routine health screenings. This commitment has led to a consistent, year-round demand for supplements. As Europeans increasingly prioritize proactive health management, there's been a notable uptick in supplement consumption, especially for immunity, gut health, and age-related issues. Preventive health management is being driven by rising awareness of the long-term benefits of maintaining overall well-being and reducing the risk of chronic diseases. Responding to this trend, European brands such as Doppelherz, Orkla Health, and Vitabiotics are broadening their product lines. They're focusing on daily use, personalized nutrition, and solutions tailored to specific conditions, bolstering their retail presence with these targeted formulations. These brands are also leveraging advancements in research and development to create innovative products that cater to evolving consumer needs, further solidifying their position in the market.

Supplements targeting women consumers fueling growth

The European dietary supplements market is experiencing growth in women-specific formulations, particularly in segments related to fertility, menopause, and beauty-from-within products. Products labeled "for her" demonstrate higher basket attachment rates and lower price sensitivity compared to gender-neutral alternatives. Innovation in this segment focuses on mood and stress relief supplements, addressing the intersection of hormonal changes and work-life demands. Companies effectively communicating emotional well-being benefits have gained traction, particularly in the United Kingdom and France, where mental health awareness has increased. Women's health supplements continue to influence broader ingredient trends, as active ingredients initially tested in female-focused trials expand into general wellness products. For instance, in May 2025, Optibac introduced Women's Wellbeing, a probiotic supplement combining friendly bacteria with essential vitamins. The product features a blend of live cultures complemented by Vitamin D, C, B6, and Biotin, designed to support energy levels, mental function, immune system, skin health, hormone balance, and gut microbiome health.

Presence of counterfeit products hampering the growth

The presence of counterfeit supplements remains a significant constraint in the market, particularly affecting high-margin beauty capsules sold through online channels. While mandatory unique identification codes have reduced seizures reported by enforcement agencies, discounted grey-market listings continue to appear on cross-border platforms. In response, brands have increased their investments in brand-protection software to monitor marketplaces and initiate takedown procedures. Companies are also leveraging their anti-counterfeit measures as marketing tools by emphasizing authenticity guarantees in their brand messaging, effectively transforming a regulatory requirement into a trust-building feature. In March 2024, the European Commission (EC) launched a formal investigation into a Chinese e-commerce giant for potential violations of the Digital Services Act (DSA). The investigation focuses on the platform's management of illegal or harmful products, including counterfeit medicines, food, and dietary supplements, along with influencer involvement in promoting these items.

Other drivers and restraints analyzed in the detailed report include:

- Europe's aging population boosts demand for age-related supplements

- Consumers' inclination towards clean-label and natural supplements

- Scientific skepticism reduces consumer trust in unproven products

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2024, vitamins commanded a dominant 33.21% share of the European dietary supplements market. This stronghold is bolstered by a robust scientific consensus, their prevalent use in preventive health measures, and their endorsement in public health initiatives. Highlighting the industry's evolving focus, ILSI Europe launched its Vitamin K2 Task Force in 2024, spotlighting emerging micronutrients. These nutrients, especially those targeting bone and cardiovascular health, are expanding the appeal of the category beyond mere general wellness.

Prebiotics and probiotics, set to grow at a 9.61% CAGR from 2025 to 2030, are riding the wave of heightened consumer awareness about gut health and its pivotal roles in immunity and mood regulation. Products tailored to specific strains enjoy elevated repeat purchase rates, and collaborations with fermented foods amplify both trial and adoption rates. Minerals hold consistent demand, driven by a healthcare spotlight on micronutrient deficiencies. Meanwhile, omega-3s experience surges in popularity during cardiovascular health campaigns. Additionally, protein and amino acid supplements are carving out spaces in general wellness sections, touted for their muscle benefits and role in promoting satiety.

Tablets currently hold the largest market share with 28.17% in 2024, while gummies are expected to grow at a CAGR of 10.01% during 2025-2030. Tablets are the dominant form of dietary supplements, offering advantages such as convenience, cost-effectiveness, efficient manufacturing, and extended shelf life. Their precise dosage control and consumer familiarity contribute to their widespread adoption in the market. The increasing consumer preference for gummies stems from pill fatigue and the enhanced consumption experience. The development of starch-free gummy formulations enables manufacturers to incorporate temperature-sensitive active ingredients, broadening their application scope. Premium travel-size pouches have gained market share over larger bottles in specific regions, indicating consumer willingness to pay more for convenience and product freshness. Capsules and softgels remain dominant in specific segments, particularly for fish-oil concentrates, due to their superior oxidation protection, while powders maintain popularity among consumers who incorporate supplements into smoothies.

Liquid formulations address the needs of elderly consumers and children who have difficulty swallowing, highlighting the importance of accessibility in product development. New formats, such as liquid-filled gummy capsules, combine the benefits of softgels with gummy appeal. These delivery format innovations serve as product differentiators, enabling companies to distinguish themselves beyond their ingredient offerings.

The Europe Dietary Supplements Market Report is Segmented by Product Type (Vitamins, Enzymes, and More), Form (Tablets, Powders, and More), Source (Plant, Animal, and More), Consumer Group (Men, Women, and More), Health Applications (General Health and Wellness, Eye Health and More), Distribution Channel (Specialty Stores, Online Retail Channels, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Bayer AG

- Herbalife Nutrition Ltd.

- Nestle S.A.

- GlaxoSmithKline plc

- Procter & Gamble Company

- Perrigo Company plc

- Sanofi S.A

- Reckitt Benckiser Group plc

- Arkopharma Laboratories

- Probi AB

- DSM-Firmenich AG

- Orkla ASA

- Abbott Laboratories

- BioGaia AB

- Pileje SAS

- Lonza Group AG

- Vitabiotics Ltd.

- Unilever plc (OLLY)

- H&H Group (Swisse)

- Pharma Nord ApS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Preventive healthcare trends are driving regular supplement consumption

- 4.2.2 Supplements targeting women consumers fueling growth

- 4.2.3 Consumers' inclination towards clean-label and natural supplements

- 4.2.4 Europe's aging population boosts demand for age-related supplements

- 4.2.5 Growing popularity of sports nutrition and fitness trends drives supplement use among younger consumers

- 4.2.6 E-Commerce expansion makes supplements more accessible and promotes market growth

- 4.3 Market Restraints

- 4.3.1 Presence of counterfeit products hampering the growth

- 4.3.2 Scientific skepticism reduces consumer trust in unproven products

- 4.3.3 Strict regulations limit health claims on supplements

- 4.3.4 Growing preference for natural food-based nutrition reduces reliance on supplements

- 4.4 Regulatory Outlook

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Vitamins

- 5.1.2 Minerals

- 5.1.3 Fatty Acids

- 5.1.4 Protein and Amino Acids

- 5.1.5 Prebiotic and Probiotic Supplements

- 5.1.6 Herbal Supplements

- 5.1.7 Enzymes

- 5.1.8 Blended Supplements

- 5.1.9 Other Product Types

- 5.2 By Form

- 5.2.1 Tablets

- 5.2.2 Capsules and Softgels

- 5.2.3 Powders

- 5.2.4 Gummies

- 5.2.5 Liquids

- 5.2.6 Other Forms

- 5.3 By Source

- 5.3.1 Plant-based

- 5.3.2 Animal-based

- 5.3.3 Synthetic / Fermentation-derived

- 5.4 By Consumer Group

- 5.4.1 Men

- 5.4.2 Women

- 5.4.3 Kids/Children

- 5.5 By Health Application

- 5.5.1 General Health and Wellness

- 5.5.2 Bone and Joint Health

- 5.5.3 Energy and Weight Management

- 5.5.4 Gastrointestinal and Gut Health

- 5.5.5 Immunity Enhancement

- 5.5.6 Cardiovascular Health

- 5.5.7 Diabetes Management

- 5.5.8 Cognitive and Mental Health

- 5.5.9 Skin, Hair and Nail Care

- 5.5.10 Eye Health

- 5.5.11 Other Health Applications

- 5.6 By Distribution Channel

- 5.6.1 Supermarkets/Hypermarkets

- 5.6.2 Specialty Stores

- 5.6.3 Online Retail Channels

- 5.6.4 Direct Selling

- 5.6.5 Other Distribution Channels

- 5.7 By Geography

- 5.7.1 Germany

- 5.7.2 United Kingdom

- 5.7.3 Italy

- 5.7.4 France

- 5.7.5 Spain

- 5.7.6 Netherlands

- 5.7.7 Poland

- 5.7.8 Belgium

- 5.7.9 Sweden

- 5.7.10 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 Bayer AG

- 6.4.2 Herbalife Nutrition Ltd.

- 6.4.3 Nestle S.A.

- 6.4.4 GlaxoSmithKline plc

- 6.4.5 Procter & Gamble Company

- 6.4.6 Perrigo Company plc

- 6.4.7 Sanofi S.A

- 6.4.8 Reckitt Benckiser Group plc

- 6.4.9 Arkopharma Laboratories

- 6.4.10 Probi AB

- 6.4.11 DSM-Firmenich AG

- 6.4.12 Orkla ASA

- 6.4.13 Abbott Laboratories

- 6.4.14 BioGaia AB

- 6.4.15 Pileje SAS

- 6.4.16 Lonza Group AG

- 6.4.17 Vitabiotics Ltd.

- 6.4.18 Unilever plc (OLLY)

- 6.4.19 H&H Group (Swisse)

- 6.4.20 Pharma Nord ApS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK