PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850349

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850349

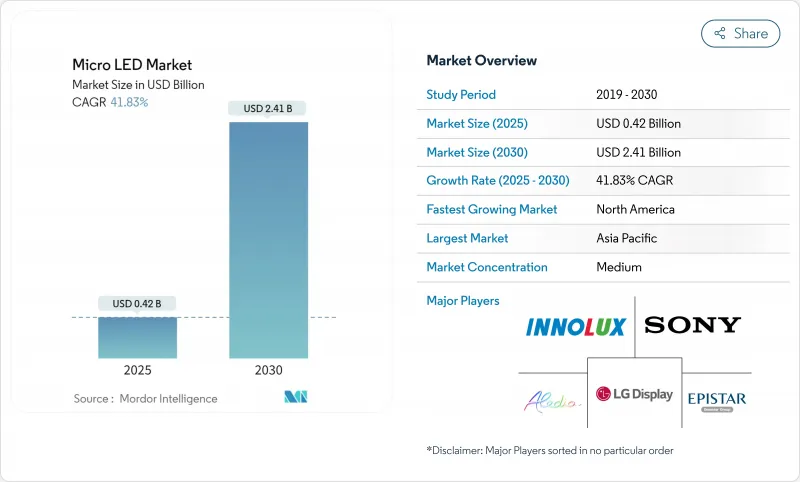

Micro LED - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Micro LED market stood at USD 0.42 billion in 2025 and is forecast to reach USD 2.41 billion by 2030, advancing at a 41.83% CAGR.

Commercial traction hinges on the technology's high brightness, low power draw, and proven longevity that outperforms LCD and OLED displays. Manufacturers are steadily lifting mass-transfer yields, and capital-intensive pilot lines in Taiwan and South Korea are scaling the technology for wearables, large-format signage, and automotive cockpits. Asia Pacific commands manufacturing leadership on the back of mature semiconductor ecosystems and supportive industrial policies, while North America is accelerating investment for defense and AR/VR programs. Pricing remains elevated, yet end-users with severe power, thermal, or sunlight-readability constraints are moving first, reinforcing premium positioning and underscoring the long-run competitiveness of the Micro LED market.

Global Micro LED Market Trends and Insights

Apple and Samsung Roadmaps for Micro-LED Wearables Accelerating Small-Display Demand

Apple's USD 3 billion outlay since acquiring LuxVue and Samsung's parallel R&D programs signal long-term commitment despite near-term schedule shifts. Rising design wins for driver ICs and transfer equipment suppliers indicate a supply-chain pivot toward sub-2-inch panels. High brightness, stringent power budgets, and demand for outdoor readability underpin a projected 45% CAGR for smartwatch displays. Specialized tool vendors are commercializing high-throughput pick-and-place systems, helping democratize pilot production beyond flagship brands. This dynamic underlines how strategic roadmaps from two market leaders shape broader capital allocation across the Micro LED market.

Transparent and Flexible Retail Signage Uptake in GCC and East Asia

Luxury malls in Dubai and flagships in Seoul are installing bezel-less, transparent Micro LED facades that merge digital content with physical storefronts. Tianma's PID prototypes, engineered for 4,000-nit outdoor brightness, illustrate performance headroom over LCD alternatives. Modular architectures simplify custom dimensions, trimming installation cycles for retail integrators. Energy efficiency also reduces total cost of ownership for 24/7 operation. These attributes safeguard the 38% application lead held by digital signage and set the stage for new revenue pools inside the Micro LED market.

Mass-Transfer Yield Sub 60% for Sub-10 µm LEDs Beyond 4-Inch Wafers

Placement accuracy for millions of micro-emitters on large substrates remains below 60%, inflating scrap rates and depressing line utilization. Equipment makers are trialing laser-induced transfer and electromagnetic pick-up to reach 99.99% placement accuracy, while VueReal's MicroSolid Printing demonstrates sub-7 µm pitch capability. Until these solutions mature, output costs will stay above OLED equivalents, limiting near-term penetration in mass-market televisions and smartphones inside the Micro LED market.

Other drivers and restraints analyzed in the detailed report include:

- Defense-Grade Micro-Displays Funded by US and EU Governments

- Taiwanese Mini-LED Cost Decline Enabling Pilot Micro-LED Lines

- GaN-on-Si Wafer Supply Concentration in Asia

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Digital signage delivered 38% of 2024 revenue, validating Micro LED's suitability for high-impact, day-light-readable video walls. Luxury retail chains deploy modular tiles that form seamless canvases, while transportation hubs favor Micro LED's low failure rates for critical information boards. The segment's stable order flow underpins early capacity utilization, reinforcing the Micro LED market.

Smartwatch shipments, in contrast, scale with consumer electronics release cycles. Battery-limited wearables demand sub-1-watt displays, and 3,000-nit peak brightness extends outdoor usability. The segment's 45% forecast CAGR positions it as a pivotal volume driver. Near-eye AR modules are also progressing as pixel densities exceed 4,000 PPI, setting the stage for broader adoption and supporting the long-run expansion of the Micro LED market size at the small-panel end.

Consumer electronics captured 72.1% of 2024 demand as premium TVs, watches, and smartphones embraced the technology's high contrast and longevity. Samsung's flagship television line, The Wall, anchors large-screen showcase deployments and validates premium pricing. The segment's breadth stabilizes component demand across backplanes, driver ICs, and inspection tools, cementing its central role in the Micro LED market.

Automotive demand is rising at a projected 47% CAGR amid stricter European sun-readability mandates. HUD prototypes achieve over 10,000 nits, ensuring legibility through polarized windscreens. Extended temperature tolerance and vibration resistance also meet AEC-Q standards. As more carmakers integrate advanced driver displays, the Micro LED market size for cockpit electronics is set to widen, diversifying revenue beyond consumer gadgets.

Panels larger than 50 inches held 55.6% of 2024 revenue. Luxury residential and corporate lobbies adopt 110-inch to 220-inch assemblies where installation flexibility and unrivaled peak luminance justify premium prices. High-end hospitality venues leverage bezel-free surfaces to create immersive experiences, reinforcing share dominance within the Micro LED market.

Panels below 10 inches will grow 49% CAGR to 2030 as manufacturing breakthroughs lower cost per die. Sub-1-inch micro-displays now reach 6,500 PPI for VR headsets, and smart-instrument clusters in vehicles demand compact, high-resolution formats. Adoption of advanced transfer printing hastens the learning curve, signaling that small-panel volumes will increasingly reshape Micro LED market share dynamics later in the decade.

The Micro LED Market Report is Segmented by Application (Smartwatch, and More), End-Use Industry (Automotive, and More), Panel Size (Less Than 10 Inch, and More), Pixel Pitch (Fine Pitch, and More), Technology (Color) (RGB, and More), Component (Epitaxial Wafers, and More), Manufacturing Process (Mass Transfer, and More), Offering (Display Modules, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia Pacific held 46.9% of 2024 revenue, powered by Taiwan's role in back-end processing and South Korea's deep display know-how. BOE's acquisition of HC SemiTek and Sanan's USD 2 billion fab plan underscore continued capital inflows. Government facilitation, including export rebates on GaN wafers, sustains regional cost advantages and solidifies leadership in the Micro LED market.

North America is growing fastest at 43% CAGR to 2030. Federal incentives under the CHIPS Act spur new gallium-nitride lines, while defense and AR/VR programs lock in offtake agreements. Apple's multi-site R&D footprint and Meta's headset ambitions concentrate ecosystem activity, driving robust design iterations and supporting higher substrate demand.

Europe carves out a specialty role in automotive and industrial deployments. Sun-readability mandates accelerate HUD integration, and local tier-1 suppliers collaborate with Asian LED makers to secure stable die flow. Parallel EU subsidies for clean-room retrofits nurture a nascent wafer supply base, providing strategic hedges against Asian concentration. Adoption in Middle East and Africa begins with premium retail signage in GCC malls, whereas Latin America pilots large-venue displays tied to sports infrastructure investments.

- Samsung Electronics Co. Ltd.

- Sony Corporation

- LG Display Co. Ltd.

- BOE Technology Group Co. Ltd.

- AU Optronics Corp.

- Epistar Corporation

- PlayNitride Inc.

- Innolux Corporation

- Apple Inc. (LuxVue Technology)

- Tianma Microelectronics Co. Ltd.

- Nichia Corporation

- Sharp Corporation

- VueReal Inc.

- Plessey Semiconductors Ltd.

- Aledia SA

- Ostendo Technologies Inc.

- Rohinni LLC

- Leyard Optoelectronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- San'an Optoelectronics Co. Ltd.

- Allos Semiconductors GmbH

- Optovate Ltd.

- Foxconn (Hon Hai Precision)

- Konka Group Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Apple and Samsung Roadmaps for Micro-LED Wearables Accelerating Small-Display Demand

- 4.2.2 Transparent and Flexible Retail Signage Uptake in Gulf Cooperation Council Countries and East Asia

- 4.2.3 Defense-grade Micro-Displays Funded by United States and EU Governments

- 4.2.4 Taiwanese Mini-LED Cost Decline Enabling Pilot Micro-LED Lines

- 4.2.5 European Automotive Sun-Readability Norms Boosting Micro-LED HUD Integration

- 4.3 Market Restraints

- 4.3.1 Mass-Transfer Yield Sub 60 % for Sub-10 µm LEDs Beyond 4-inch Wafers

- 4.3.2 Non-standardised Automotive Qualification Protocols

- 4.3.3 GaN-on-Si Wafer Supply Concentration in Asia

- 4.3.4 More than USD 600 m Capex Requirement Limiting Expansion in South America and Africa

- 4.4 Industry Ecosystem Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Application

- 5.1.1 Smartwatch

- 5.1.2 Near-to-Eye Devices (AR/VR)

- 5.1.3 Television

- 5.1.4 Smartphone and Tablet

- 5.1.5 Monitor and Laptop

- 5.1.6 Head-up Display

- 5.1.7 Digital Signage

- 5.1.8 Micro-Projector

- 5.1.9 Medical and Surgical Displays

- 5.1.10 Industrial Inspection Panels

- 5.2 By End-use Industry

- 5.2.1 Consumer Electronics

- 5.2.2 Automotive

- 5.2.3 Aerospace and Defense

- 5.2.4 Healthcare

- 5.2.5 Advertising and Retail

- 5.2.6 Industrial and Manufacturing

- 5.2.7 Others

- 5.3 By Panel Size

- 5.3.1 Less than 10 inch (Small and Micro-Displays)

- 5.3.2 10 - 50 inch (Medium)

- 5.3.3 Above 50 inch (Large)

- 5.4 By Pixel Pitch

- 5.4.1 Fine Pitch (Less than 1.5 mm)

- 5.4.2 Standard (1.5 - 2.5 mm)

- 5.4.3 Large (Above 2.5 mm)

- 5.5 By Technology (Color)

- 5.5.1 RGB Full-Color

- 5.5.2 Monochrome

- 5.6 By Component

- 5.6.1 Epitaxial Wafers

- 5.6.2 Backplanes

- 5.6.3 Driver ICs

- 5.6.4 Transfer and Bonding Equipment

- 5.6.5 Inspection and Repair Tools

- 5.7 By Manufacturing Process

- 5.7.1 Mass Transfer

- 5.7.2 Epitaxial Wafer Bonding

- 5.7.3 Hybrid Bonding

- 5.8 By Offering

- 5.8.1 Display Modules

- 5.8.2 Lighting Modules

- 5.9 By Geography

- 5.9.1 North America

- 5.9.1.1 United States

- 5.9.1.2 Canada

- 5.9.1.3 Mexico

- 5.9.2 Europe

- 5.9.2.1 Germany

- 5.9.2.2 United Kingdom

- 5.9.2.3 France

- 5.9.2.4 Italy

- 5.9.2.5 Spain

- 5.9.2.6 Rest of Europe

- 5.9.3 Asia-Pacific

- 5.9.3.1 China

- 5.9.3.2 Japan

- 5.9.3.3 South Korea

- 5.9.3.4 India

- 5.9.3.5 South East Asia

- 5.9.3.6 Rest of Asia-Pacific

- 5.9.4 South America

- 5.9.4.1 Brazil

- 5.9.4.2 Rest of South America

- 5.9.5 Middle East and Africa

- 5.9.5.1 Middle East

- 5.9.5.1.1 United Arab Emirates

- 5.9.5.1.2 Saudi Arabia

- 5.9.5.1.3 Rest of Middle East

- 5.9.5.2 Africa

- 5.9.5.2.1 South Africa

- 5.9.5.2.2 Rest of Africa

- 5.9.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Samsung Electronics Co. Ltd.

- 6.4.2 Sony Corporation

- 6.4.3 LG Display Co. Ltd.

- 6.4.4 BOE Technology Group Co. Ltd.

- 6.4.5 AU Optronics Corp.

- 6.4.6 Epistar Corporation

- 6.4.7 PlayNitride Inc.

- 6.4.8 Innolux Corporation

- 6.4.9 Apple Inc. (LuxVue Technology)

- 6.4.10 Tianma Microelectronics Co. Ltd.

- 6.4.11 Nichia Corporation

- 6.4.12 Sharp Corporation

- 6.4.13 VueReal Inc.

- 6.4.14 Plessey Semiconductors Ltd.

- 6.4.15 Aledia SA

- 6.4.16 Ostendo Technologies Inc.

- 6.4.17 Rohinni LLC

- 6.4.18 Leyard Optoelectronics Co. Ltd.

- 6.4.19 Seoul Semiconductor Co. Ltd.

- 6.4.20 San'an Optoelectronics Co. Ltd.

- 6.4.21 Allos Semiconductors GmbH

- 6.4.22 Optovate Ltd.

- 6.4.23 Foxconn (Hon Hai Precision)

- 6.4.24 Konka Group Co. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment