PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850398

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850398

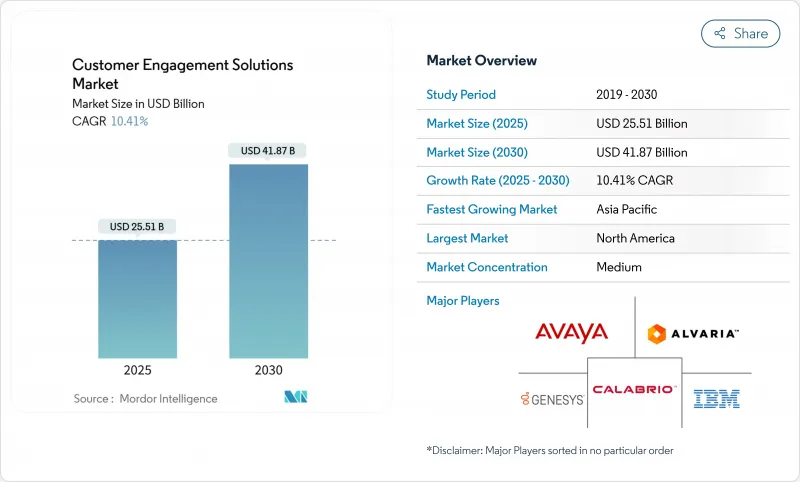

Customer Engagement Solutions - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The customer engagement solutions market size is valued at USD 25.51 billion in 2025 and is forecast to expand to USD 41.87 billion by 2030, reflecting a 10.4% CAGR.

Rapid enterprise migration to cloud contact-center platforms, rising adoption of agentic AI, and the omnichannel customer-experience (CX) imperative are the primary accelerants. Mid-sized companies are closing capability gaps by leveraging low-code generative-AI toolsets, while large enterprises consolidate after-sales tasks into unified customer-facing teams to improve lifetime value. Macro conditions also favor vendors that blend automation with human empathy, as 86% of consumers now acknowledge AI's role in resolving issues quickly. Competitive intensity continues to rise because contact-center specialists, CRM platforms, and AI-first start-ups all aim to own the last mile of customer relationships.

Global Customer Engagement Solutions Market Trends and Insights

Cloud-based Contact-center Adoption Surge

Commercial cloud migration now serves as a structural pivot for CX operations rather than a cost-reduction exercise. 80.4% of enterprises report that cloud contact centers help future-proof technology infrastructures. The architecture delivers elastic scale for globally distributed workforces and integrates natively with AI engines that automate call transcription and sentiment analysis. Less than 40% of businesses have moved unified communications to the cloud, leaving a deep runway for growth. Adoption is strongest among organizations that must quickly spin up seasonal capacity or navigate multi-site operations. Migration complexity, especially for firms with legacy PBX investments, is spawning a robust ecosystem of managed-services providers that orchestrate phased cutovers while ensuring business continuity.

Omnichannel CX Imperative Across Industries

Customer journeys now stretch across messaging apps, live chat, social media, and voice, prompting 87% of users to demand seamless hand-offs between channels. True omnichannel delivery goes beyond simply adding digital touchpoints; it relies on a unified data fabric that preserves interaction context. Brands that remove data silos report higher agent productivity because staff can instantly retrieve prior conversations without toggling interfaces. Voice remains relevant for emotionally charged or high-value transactions, but messaging and asynchronous video gain favor for routine inquiries. Leaders deploy single-agent desktop environments that blend digital and voice routing within one queue, thereby aligning KPIs around customer effort rather than channel utilization.

Data-privacy and Cybersecurity Concerns

A majority 68% of consumers express anxiety over how brands handle their personal information. Global regulators are responding with stringent rules covering biometric data, call recording, and automated decision-making. Contact-center AI deployments that monitor emotion or track location can trigger legal action if consent workflows are weak, as illustrated by recent U.S. lawsuits involving unauthorized monitoring. Enterprises now prioritize encryption at rest, tokenization of sensitive fields, and "explainable AI" dashboards that document the logic behind automated recommendations. Vendors offering differential-privacy tooling and data-residency controls gain a competitive edge because they de-risk compliance without sacrificing personalization fidelity.

Other drivers and restraints analyzed in the detailed report include:

- AI-driven Hyper-personalization and Analytics

- Distributed Workforce Accelerating Digital Service

- Legacy System Integration Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solutions maintained 67.5% of 2024 revenue thanks to robust demand for omnichannel routing engines, conversational bots, and speech analytics modules that underpin modern CX strategy. The services arm, however, is growing faster at an 11.8% CAGR as enterprises lean on external specialists for migration, model-tuning, and governance. Advisory teams help phase out redundant IVR scripts, create persona-based dialog flows, and set up continuous-learning loops so AI agents improve after each interaction. Managed-services contracts increasingly bundle proactive performance monitoring to spot latency spikes that impair voice quality. Professional-services engagements also emphasize change-management programs that coach frontline supervisors on interpreting real-time coaching dashboards. This consultative focus indicates that differentiation in the customer engagement solutions market now tilts toward execution excellence rather than feature checklists.

A parallel investment narrative emerges in managed security for CX stacks, encompassing endpoint hardening, penetration testing, and compliance audits mapped to ISO 27001 controls. Vendors that combine platform IP with mature service desks capture longer annuity streams because clients prefer one throat to choke when outages occur. As more enterprises adopt agentic AI, demand escalates for prompt-engineering workshops and hallucination-mitigation frameworks. Collectively, these trends place services at the center of value creation, cementing their double-digit growth trajectory inside the broader customer engagement solutions market.

Although on-premise deployments still account for 70.8% of the customer engagement solutions market size, the growth engine is squarely in the cloud, which is expanding at a 12.5% CAGR. Hybrid calling services ease the transition by interconnecting legacy time-division-multiplexing trunks with WebRTC endpoints, allowing agents to work from home without compromising voice clarity. The economics also favor consumption-based pricing models that let companies flex capacity during peak shopping periods. Security objections are steadily receding as hyperscalers adopt zero-trust blueprints and provide granular key-management options that align with industry mandates such as PCI-DSS.

Large enterprises often pilot individual business units on the cloud before executing a full rip-and-replace program. Small and medium enterprises, by contrast, jump straight to multitenant architectures because they have fewer legacy baggage. Industry regulators now certify cloud contact-center providers for advanced use cases like real-time mortgage servicing or tele-health triage, further accelerating migration. As a result, vendor roadmaps prioritize API-first design, ensuring seamless integration between contact-center as a service (CCaaS) and workflow platforms. The momentum suggests that cloud will command a decisive lead in incremental bookings within the customer engagement solutions market by the end of the decade.

The Customer Engagement Solutions Market Report is Segmented by Component (Solution and Services), Deployment Type (On-Premise and Cloud), Organization Size (Large Enterprises and Small and Medium Enterprises (SMEs)), End-User Industry (BFSI, IT and Telecom, Retail and Consumer Goods, Media and Entertainment, Healthcare, and Other End-User Industries), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained its lead at 41.3% of 2024 revenue because enterprises in the United States and Canada possess mature cloud infrastructures and sizable AI budgets. The region is a launchpad for agentic AI pilots that autonomously handle password resets and subscription changes without human escalation. Cloud migration also accelerated after multiple state privacy laws introduced stiff penalties for data breaches, nudging firms toward standardized, certified environments. Large financial services firms in New York deploy multimodal AI assistants that interpret voice stress levels to trigger fraud alerts, reflecting advanced use-case maturity. Canadian telcos pioneer 5G-enabled video-chat support, while Mexican manufacturers implement multilingual chatbots to serve cross-border customers.

Asia-Pacific is the fastest-growing region, posting an 11.4% CAGR through 2030. The conversational-AI submarket alone is expanding 24.1% annually as mobile-first consumers demand round-the-clock support across messaging super-apps. China's e-commerce giants operate AI-rich live-stream shopping shows that blend entertainment with instant purchasing, driving volumes that reshape global CX expectations. Singapore's Monetary Authority offers regulatory sandboxes that de-risk AI experimentation in banking, while India's start-up ecosystem supplies high-quality developers at competitive rates. Combined, these factors create a fertile environment for the rapid adoption of the customer engagement solutions market.

Europe follows a measured trajectory shaped by GDPR and emerging AI-ethics legislation. Firms prioritize privacy-preserving architectures that keep inference data within regional borders, spurring demand for on-premise or sovereign-cloud deployments. Germany leverages customer engagement platforms to support Industry 4.0 after-sales service, United Kingdom fintechs refine real-time KYC verification in chat flows, and France's luxury houses deliver concierge-style messaging to high-spend clients. Southern and Eastern Europe show a growing appetite as EU recovery funds earmark digital modernization. South America and the Middle East and Africa remain nascent but promising; Brazil's fintech boom and GCC smart-city projects position both regions to leapfrog legacy voice-centric models by adopting cloud-native platforms from day one. Widespread 4G and rising smartphone penetration underpin the next demand wave for the customer engagement solutions market.

- Adobe Inc.

- Amazon Web Services

- Avaya Inc.

- Alvaria Inc.

- Calabrio Inc.

- Cisco Systems Inc.

- Five9 Inc.

- Freshworks Inc.

- Genesys

- IBM Corporation

- Microsoft Corporation

- NICE Ltd.

- Nuance Communications Inc.

- OpenText Corporation

- Oracle Corporation

- Pegasystems Inc.

- Salesforce Inc.

- SAP SE

- Twilio Inc.

- Verint Systems Inc.

- Zendesk Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-based contact-center adoption surge

- 4.2.2 Omnichannel CX imperative across industries

- 4.2.3 AI-driven hyper-personalization and analytics

- 4.2.4 Distributed workforce accelerating digital service

- 4.2.5 Agentic-AI bots autonomously resolving inquiries

- 4.2.6 Accessibility-first compliance mandates

- 4.3 Market Restraints

- 4.3.1 Data-privacy and cybersecurity concerns

- 4.3.2 Legacy system integration complexity

- 4.3.3 Generative-AI hallucination brand-risk

- 4.3.4 Talent gap in CX-AI governance and ethics

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Assessment of the Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Solution

- 5.1.1.1 Omni-channel Platforms

- 5.1.1.2 Workforce Engagement Management

- 5.1.1.3 Robotic Process Automation

- 5.1.1.4 Self-Service and Chatbots

- 5.1.2 Services

- 5.1.2.1 Managed Services

- 5.1.2.2 Professional Services

- 5.1.1 Solution

- 5.2 By Deployment Type

- 5.2.1 On-premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises (SMEs)

- 5.4 By End-user Industry

- 5.4.1 BFSI

- 5.4.2 IT and Telecom

- 5.4.3 Retail and Consumer Goods

- 5.4.4 Media and Entertainment

- 5.4.5 Healthcare

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Nigeria

- 5.5.5.2.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adobe Inc.

- 6.4.2 Amazon Web Services

- 6.4.3 Avaya Inc.

- 6.4.4 Alvaria Inc.

- 6.4.5 Calabrio Inc.

- 6.4.6 Cisco Systems Inc.

- 6.4.7 Five9 Inc.

- 6.4.8 Freshworks Inc.

- 6.4.9 Genesys

- 6.4.10 IBM Corporation

- 6.4.11 Microsoft Corporation

- 6.4.12 NICE Ltd.

- 6.4.13 Nuance Communications Inc.

- 6.4.14 OpenText Corporation

- 6.4.15 Oracle Corporation

- 6.4.16 Pegasystems Inc.

- 6.4.17 Salesforce Inc.

- 6.4.18 SAP SE

- 6.4.19 Twilio Inc.

- 6.4.20 Verint Systems Inc.

- 6.4.21 Zendesk Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment