PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850957

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1850957

Ophthalmic Lasers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

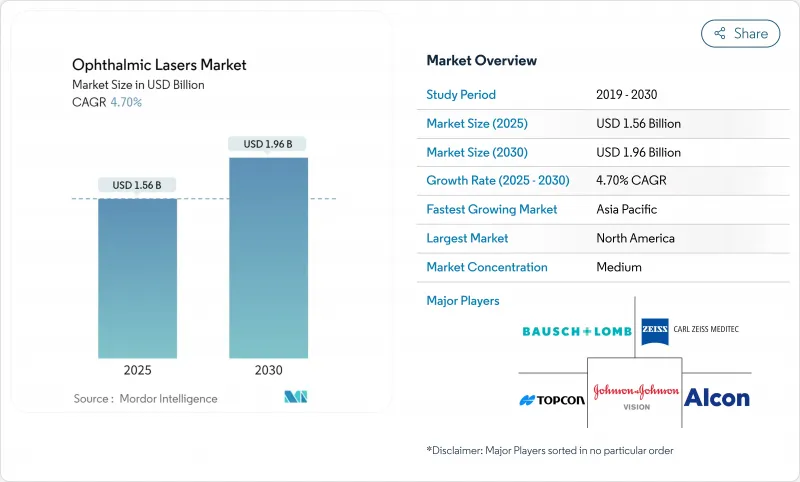

The ophthalmic lasers market is valued at USD 1.56 billion in 2025 and is forecast to touch USD 1.96 billion by 2030, advancing at a 4.7% CAGR.

Momentum derives more from precision-engineering upgrades than volume expansion, with femtosecond platforms setting new speed benchmarks while retaining tissue accuracy. North America anchors demand through high procedural volumes and early regulatory approvals, yet Asia-Pacific supplies the steepest growth curve as rising myopia and aging demographics converge. The sustained shift toward ambulatory surgery centers (ASCs) and office-based suites is reshaping capital-equipment preferences toward portable, integrated platforms. Competition now pivots on AI-ready systems that compress treatment times, improve outcome predictability, and streamline clinical workflows, allowing premium pricing even under cost-containment pressure.

Global Ophthalmic Lasers Market Trends and Insights

High Prevalence of Ophthalmic Disorders

Cataract cases already affect over 20.5 million Americans and continue to climb, guaranteeing a steady patient pool for laser-assisted surgeries. Asia-Pacific adds additional pressure as visual-impairment prevalence rose 17.9% from 1990 to 2015, mainly because of urban myopia and diabetes-linked retinopathy.These overlapping pathologies often require multipurpose laser platforms capable of photocoagulation, capsulotomy, and trabeculoplasty in a single session, encouraging providers to purchase broad-spectrum systems. The demographic wave also underpins service-contract revenue, as high device utilization necessitates predictable maintenance. Manufacturers with complete portfolios are therefore better positioned to capture the compounding demand across cataract, refractive, and retinal indications.

Rising Regulatory Approvals & Clearances

Regulators have become more receptive to genuine innovations, shortening time-to-market. The FDA cleared Bausch + Lomb's Teneo excimer platform in 2024, the first such approval in two decades. LumiThera's Valeda system secured authorization as the inaugural photobiomodulation therapy for dry AMD, widening therapeutic frontiers. Parallel activity in Europe saw ViaLase win a CE mark for femtosecond glaucoma therapy and Espansione Group gain approval for photobiomodulation devices. Each clearance enlarges the addressable patient pool and sets clinical precedent, easing future submissions and supporting a healthy pipeline of differentiated offerings.

High System Purchase & Maintenance Cost

Advanced laser units range between USD 500,000 and USD 1.5 million, while annual service contracts absorb 8-12% of that figure, stressing smaller practices. Emerging economies face 25-40% import mark-ups and currency-related volatility that prolong payback periods. Although leasing and shared-usage models alleviate cash flow barriers, they often cap monthly shots or procedures, limiting revenue upside. Consequently, group purchasing and multi-site health networks favor vendors that bundle fleet-wide service at predictable rates, nudging the market toward a few scale-efficient suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Continuous Femtosecond & Excimer Technology Upgrades

- AI-Driven Personalized Ablation Profiles

- Shortage of Laser-Trained Ophthalmic Surgeons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Photocoagulation systems retained 38.3% of the ophthalmic lasers market share in 2024, a testament to their entrenched role in retinal care. However, femtosecond platforms are on an 8.8% CAGR trajectory through 2030, propelled by ultrafast pulse rates that slash chair time and discomfort. The VisuMax 800's 2,000 kHz speed not only enhances throughput but also supports SMILE procedures that preserve corneal biomechanics. In contrast, excimer devices rely on incremental gains such as Teneo's 1,740 Hz eye-tracking, reinforcing their place in surface ablation. Nd:YAG disruptors continue to anchor capsulotomy and vitreolysis, while selective laser trabeculoplasty (SLT) systems broaden glaucoma therapy options. Multipurpose consoles that merge photocoagulation with femtosecond or Nd:YAG modules are increasingly favored for capital efficiency.

The femtosecond surge underscores a transition from thermal to photo-disruptive precision. Vendors integrating AI-driven planning and ergonomic improvements command premium placements. As a result, segment players investing in cross-platform ecosystems are set to outpace niche specialists, especially in high-volume ASCs seeking all-in-one devices. In value terms, the ophthalmic lasers market size for femtosecond equipment is projected to capture USD 0.59 billion by 2030, reflecting sustained replacement demand among early adopters.

Cataract-oriented lasers safeguarded a 34.1% stake in 2024, yet refractive error corrections promise the quickest lift at 9.4% CAGR to 2030, fuelled by consumer willingness to finance vision-enhancement electives. Femtosecond-assisted LASIK and SMILE now compete on optical-zone stability and reduced dry-eye incidence, with small-incision lenticule implantation reporting 87% visual-acuity maintenance.

Sub-threshold micropulse modalities advance retinal-disease management by limiting collateral damage, while SLT innovations like Alcon's Voyager DSLT remove gonio-lens handling, simplifying glaucoma workflows. The ophthalmic lasers market size for refractive applications is forecast to expand from USD 0.46 billion in 2025 to USD 0.71 billion by 2030 as elective procedure volumes climb. Integrated consoles capable of toggling between cataract fragmentation, corneal reshaping, and trabeculoplasty appeal to mixed-case sites, further blurring historical single-indication boundaries.

The Ophthalmic Lasers Market is Segmented by Product (Femtosecond Lasers, Excimer Lasers, and More), Application (Cataract Surgery, Refractive Error Correction, and More), End User (Hospitals, Specialist Eye Clinics & Chains, and More), Technology Integration (Stand-Alone Laser Systems and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the ophthalmic lasers market with 37.4% revenue in 2024 and is expected to post mid-single-digit growth through 2030. High equipment penetration, favorable reimbursement, and early FDA clearances keep the region ahead, yet looming surgeon shortages cap upside. Projections show a 30% ophthalmologist deficit by 2035, with rural access dipping lowest. Migration to ASCs and value-based payment rewards lasers that cut complications, but rising capital costs nudge some practices toward leasing consortia and shared-service models.

Asia-Pacific is the fastest-advancing territory at 6.3% CAGR. Escalating myopia-now exceeding 80% in certain urban young-adult cohorts-combines with aging populations to swell cataract and refractive workloads. Yet uneven surgeon distribution and price-sensitive procurement favor stripped-down, low-maintenance designs. China's volume-based procurement squeezes margins, pushing manufacturers to offer value-tier SKUs, while India and Southeast Asia reward portable handheld units suited to outreach camps. Robust clinical-training alliances and philanthropic programs will be pivotal in converting underlying disease prevalence into sustainable device adoption.

Europe exhibits steady expansion courtesy of CE-mark alignment and universal insurance coverage. CE approvals in 2024 for femtosecond glaucoma and photobiomodulation devices demonstrate regulatory agility. Country-level reimbursement nuances, however, generate market fragmentation, requiring vendors to tailor value-submission dossiers by payer. Western Europe champions clinical-outcome data while Eastern markets lean on affordability, creating bifurcated demand streams within the continent. Middle East & Africa and South America house significant unmet surgical need but grapple with supply-chain gaps and currency risk. Donation programs, mobile surgery caravans, and government co-payment schemes could gradually unlock latent potential, though short-term growth remains modest.

- Alcon

- Johnson & Johnson

- Carl Zeiss

- Bausch + Lomb

- Topcon Corp

- IRIDEX Corp

- Lumenis

- Lumibird Group

- Nidek

- Ellex Medical Laser

- Coherent

- Ziemer Group

- SCHWIND eye-tech-solutions

- LENSAR

- Lightmed

- Quantel Laser USA

- iVIS Technologies

- ViaLase

- ForSight Robotics

- WaveLight GmbH

- HAAG-Streit

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 High Prevalence Of Ophthalmic Disorders

- 4.2.2 Rising Regulatory Approvals & Clearances

- 4.2.3 Continuous Femtosecond & Excimer Technology Upgrades

- 4.2.4 Expanding Optometrist Scope-Of-Practice Laws

- 4.2.5 Portable Low-Energy "Table-Top" Lasers Lowering Capex

- 4.2.6 AI-Driven Personalised Ablation Profiles

- 4.3 Market Restraints

- 4.3.1 High System Purchase & Maintenance Cost

- 4.3.2 Shortage Of Laser-Trained Ophthalmic Surgeons

- 4.3.3 Reimbursement Uncertainty For FLACS Codes In EMs

- 4.3.4 Competing Premium IOL & Pharma Pipelines Curbing Demand

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product

- 5.1.1 Femtosecond Lasers

- 5.1.2 Excimer Lasers

- 5.1.3 Nd:YAG Photodisruption Lasers

- 5.1.4 Photocoagulation/Diode & Argon Lasers

- 5.1.5 Selective Laser Trabeculoplasty (SLT) Lasers

- 5.1.6 Pattern-Scanning Photocoagulators

- 5.1.7 Combined Multipurpose Platforms

- 5.2 By Application

- 5.2.1 Cataract Surgery (FLACS, Capsulotomy)

- 5.2.2 Refractive Error Correction (LASIK, SMILE, PRK)

- 5.2.3 Glaucoma (SLT, Cylophotocoagulation)

- 5.2.4 Diabetic Retinopathy & DME

- 5.2.5 Age-Related Macular Degeneration

- 5.2.6 Pediatric & Other Retinal Disorders

- 5.3 By End User

- 5.3.1 Hospitals

- 5.3.2 Specialist Eye Clinics & Chains

- 5.3.3 Ambulatory Surgery Centers (ASC)

- 5.3.4 Academic & Research Institutes

- 5.4 By Technology Integration

- 5.4.1 Stand-alone Laser Systems

- 5.4.2 Integrated Phaco-Laser Workstations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia Pacific

- 5.5.4 Middle East & Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East & Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Alcon

- 6.3.2 Johnson & Johnson Vision

- 6.3.3 Carl Zeiss Meditec

- 6.3.4 Bausch + Lomb

- 6.3.5 Topcon Corp

- 6.3.6 IRIDEX Corp

- 6.3.7 Lumenis

- 6.3.8 Lumibird (Quantel Medical)

- 6.3.9 NIDEK Co., Ltd.

- 6.3.10 Ellex Medical Lasers

- 6.3.11 Coherent Inc.

- 6.3.12 Ziemer Ophthalmic Systems

- 6.3.13 SCHWIND eye-tech-solutions

- 6.3.14 LENSAR

- 6.3.15 Lightmed

- 6.3.16 Quantel Laser USA

- 6.3.17 iVIS Technologies

- 6.3.18 ViaLase

- 6.3.19 ForSight Robotics

- 6.3.20 WaveLight GmbH

- 6.3.21 Haag-Streit Surgical

7 Market Opportunities & Future Outlook

- 7.1 White-Space & Unmet-Need Assessment