PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851179

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851179

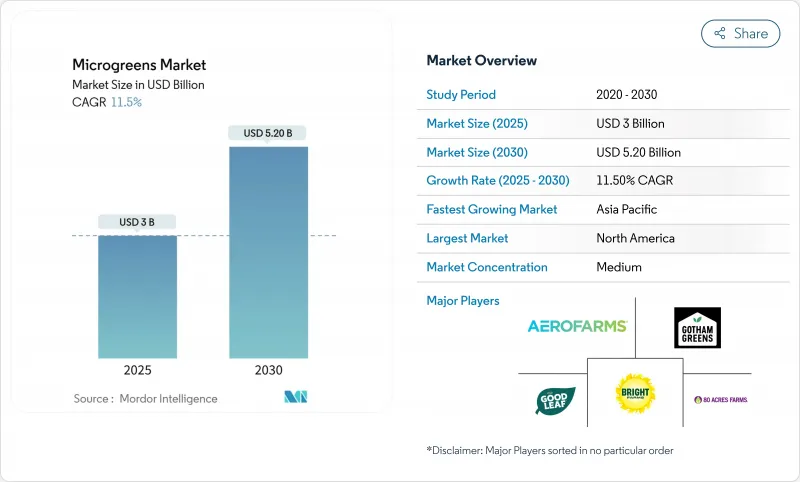

Microgreens - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The microgreens market size reached USD 3.0 billion in 2025 and is forecast to advance to USD 5.2 billion by 2030, translating into an 11.5% CAGR over the period.

Sustained demand stems from consumers seeking nutrient-dense produce, producers upgrading to high-yield indoor systems, and retailers adding premium microgreen assortments to differentiate fresh-food aisles. Scientific evidence confirming that certain varieties hold 5-40 times the vitamin and antioxidant content of their mature counterparts keeps the microgreens market firmly positioned within functional foods. Technology convergence is another lift: AI-directed LED recipes are delivering energy savings close to 32% while vertical stacks achieve production densities up to 390-fold above field output. Localization strategies that shorten supply chains and reduce spoilage further reinforce the economic appeal, and lunar agriculture trials scheduled for 2026 are catalyzing new precision-growing tools for terrestrial use. Altogether, the microgreens market continues to outpace broader controlled-environment agriculture segments and is on track for another multi-year run of double-digit expansion.

Global Microgreens Market Trends and Insights

Rising Health-Conscious Consumers Demanding Nutrient-Dense Foods

Bean microgreens supply 80.45 mg/100 g of ascorbic acid-well above mature-plant levels-while their 8-21-day growth cycle supports year-round harvests. Urban dwellers facing micronutrient gaps view this concentration as worth a premium. Healthcare professionals increasingly cite microgreens when recommending functional foods that dovetail with preventive health budgets. Aging demographics magnify the pool of customers willing to invest in proven nutrition. Peer-reviewed links between routine intake and improved cardiovascular as well as glycemic markers spur repeat purchases among wellness-minded buyers. Together, these factors keep nutrition advocacy central to microgreens market messaging.

Uptake of Urban, Indoor, and Vertical Farming Infrastructures

The UAE's plan to deploy more than 500 vertical farms inside five years signals a USD 6.2 billion upside by 2030, with microgreens positioned as anchor crops thanks to quick cycles. Dutch innovator PlantLab closed EUR 20 million (USD 20 million) in 2024 to widen European capacity, underscoring investor belief in scalable models. IoT sensors now adjust humidity, CO2, and airflow at the plant level, raising yield consistency while shrinking labor. Renewable-powered chillers and heat-exchange loops improve lifetime operating costs and answer carbon-footprint critiques. Municipal incentives that target food-miles reduction further tilt economics in favor of city-center production. Collectively, these inputs build a durable foundation for capacity expansion across both mature and emerging markets.

Food-Safety Recalls Linked to Poor Sanitation Practices

Sprout outbreaks of Salmonella and E. coli color regulators' perception of similar production methods, even though no microgreens illnesses were logged from 1998-2017 extension.unr.edu. The FDA's stronger organic enforcement, activated in 2024, adds documented hazard-analysis plans and lot-level traceability, raising compliance costs. Growers now deploy antimicrobial root-zone washes and UV-C cabin tunnels to pre-empt contamination. Certifications such as GlobalGAP and SQF have become de facto tickets to retail distribution. On-farm automation reduces human touchpoints, cutting the probability of lapses. In parallel, space-crop sanitation protocols-originally devised for nutrient film technique in orbit-feed back to earth farms, offering validated pathogen-control blueprints.

Other drivers and restraints analyzed in the detailed report include:

- Fine-Dining and Premium Culinary Adoption Worldwide

- Retail-Chain Private-Label Microgreen Launches

- Fragmented Standards Delaying Global Organic Certification

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Broccoli microgreens controlled 28% of 2024 revenue within the microgreens market size, buoyed by 825.53 mg GAE/100 g total phenolics that support premium price points. Arugula retains a 15% share, leveraging its peppery kick that chefs prize for salads and pizzas. Radish lines capture 21.4%, especially in hydroponic channels, where quick germination validates aggressive planting densities.

Basil microgreens headline growth with a forecast 14.8% CAGR, reflecting culinary familiarity and aromatic punch that retail shoppers recognize quickly. Lettuce and chicory add 12.3%, offering gentle flavors that help first-time buyers. Specialty entries-fennel, pea, sorrel, and the still-controversial hemp microgreen, keeping SKUs dynamic and inviting experimentation. Continuous breeding and seed-house collaborations open fresh cultivar cycles every season, keeping consumer curiosity alive and pricing resilient.

Indoor farms held 46% microgreens market share in 2024, anchored by climate-tight rooms that deliver uniform CO2, lighting, and nutrient flow. These conditions produce leaves with consistent texture and color, vital for retailers who demand SKU-level predictability.

Vertical farms promise the fastest 20.2% CAGR through 2030 by multiplying square-foot output. AutoStore and OnePointOne's fully robotic Arizona site packs trays into cubic lattices and snips product after 15 days, using 95% less water than field cultivation. Hybrid greenhouses that stack tiered towers beneath translucent roofing split the difference on capex, appealing to mid-tier investors. Meanwhile, container farms allow on-premise production at grocery backlots and campus food halls, shrinking last-mile challenges.

The Microgreens Market Report Segments the Industry Into Type (Broccoli, Lettuce and Chicory, Arugula, Basil, Fennel, and More), Farming (Indoor Farming, Vertical Farming, and More), Growth Medium (Peat Moss, Soil, Coconut Coir, and More), Distribution Channel (Hypermarkets/Supermarkets, Restaurants, and More) and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific is the growth engine, logging a 13.1% CAGR through 2030 as urbanization and rising incomes align with government food-security grants. China's USD 1.34 trillion fruit-and-vegetable economy offers a vast runway, and megacity pilots in Shanghai and Shenzhen now place vertical farms within city blocks to slash travel time. Singapore operates high-tech indoor hubs that export microgreens to Malaysia and Indonesia, cementing the city-state as a regional innovation lab. Australia, spurred by drought and salinity concerns, backs solar-powered greenhouse clusters in peri-urban zones, while India's Bengaluru cluster champions low-capex rack farms aimed at hotel chains.

North America retained the largest contribution to the microgreens market size at 43% in 2024, reflecting mature retail penetration and robust food-service demand. Operators like AeroFarms, Gotham Greens, and Bowery Farming serve thousands of stores, and fresh financing helped GoodLeaf add 2,700 Canadian doors. Mexico leverages lower power costs and proximity to U.S. buyers, securing joint-venture supply agreements that bypass cross-border bottlenecks. Regional regulatory clarity on organic hydroponics supports premium positioning, although fragmented standards still challenge interstate logistics.

Europe is advancing at an 8.2% CAGR on the back of urban-agriculture subsidies and carbon-border adjustments that favor local production. Dutch pioneers such as PlantLab iterate on fully enclosed "Plant Production Units," while Germany's renewable-energy credits offset greenhouse inputs. Italy's farm-to-table restaurants tout microgreens-topped dishes to culinary tourists. EU organic certificate digitization, active from 2025, may erect soft trade barriers that push supermarkets to source within the bloc. Elsewhere, the Middle East marshals sovereign-wealth capital, evidenced by a USD 180.5 million Pure Harvest raise in 2024 to build climate-tough facilities, and Africa is starting its 11.4% ascent as cold-chain corridors reach secondary cities.

- AeroFarms LLC (Dream Holdings, Inc.)

- BrightFarms (Cox Enterprises)

- GoodLeaf Farms (TrueLeaf)

- Farmbox Greens (Charlie's Produce)

- Gotham Greens Farms LLC

- 80 Acres Farms

- Chef's Garden Inc.

- 2BFresh (Teshuva Agricultural Projects)

- Metro Microgreens

- Farm.One, Inc.

- Living Earth Farm

- Ibiza Microgreens

- UnsFarms (Speedex group)

- Badia Farms

- Greeneration

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising health-conscious consumers demanding nutrient-dense foods

- 4.2.2 Uptake of urban, indoor, and vertical farming infrastructures

- 4.2.3 Fine dining and premium culinary adoption worldwide

- 4.2.4 Retail-chain private-label microgreen launches

- 4.2.5 Nanotechnology-enhanced substrates boost yield and nutrition

- 4.2.6 Microgreens selected for space life support and astronaut menus

- 4.3 Market Restraints

- 4.3.1 Short post-harvest shelf life and cold-chain gaps

- 4.3.2 High unit production costs for controlled-environment farming

- 4.3.3 Food-safety recalls linked to poor sanitation practices

- 4.3.4 Fragmented standards delaying global organic certification

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Type

- 5.1.1 Broccoli

- 5.1.2 Lettuce and Chicory

- 5.1.3 Arugula

- 5.1.4 Basil

- 5.1.5 Fennel

- 5.1.6 Carrots

- 5.1.7 Sunflower

- 5.1.8 Radish

- 5.1.9 Peas

- 5.1.10 Other Types

- 5.2 By Farming Method

- 5.2.1 Indoor Farming

- 5.2.2 Vertical Farming

- 5.2.3 Commercial Greenhouses

- 5.2.4 Other Farming Methods

- 5.3 By Growth Medium

- 5.3.1 Peat Moss

- 5.3.2 Soil

- 5.3.3 Coconut Coir

- 5.3.4 Tissue Paper

- 5.3.5 Other Growth Media

- 5.4 By Distribution Channel

- 5.4.1 Hypermarkets and Supermarkets

- 5.4.2 Restaurants

- 5.4.3 Other Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Chile

- 5.5.2.3 Argentina

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Netherlands

- 5.5.3.2 Spain

- 5.5.3.3 Germany

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Singapore

- 5.5.4.4 Australia

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, Recent Developments)

- 6.4.1 AeroFarms LLC (Dream Holdings, Inc.)

- 6.4.2 BrightFarms (Cox Enterprises)

- 6.4.3 GoodLeaf Farms (TrueLeaf)

- 6.4.4 Farmbox Greens (Charlie's Produce)

- 6.4.5 Gotham Greens Farms LLC

- 6.4.6 80 Acres Farms

- 6.4.7 Chef's Garden Inc.

- 6.4.8 2BFresh (Teshuva Agricultural Projects)

- 6.4.9 Metro Microgreens

- 6.4.10 Farm.One, Inc.

- 6.4.11 Living Earth Farm

- 6.4.12 Ibiza Microgreens

- 6.4.13 UnsFarms (Speedex group)

- 6.4.14 Badia Farms

- 6.4.15 Greeneration

7 Market Opportunities and Future Outlook