PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851182

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851182

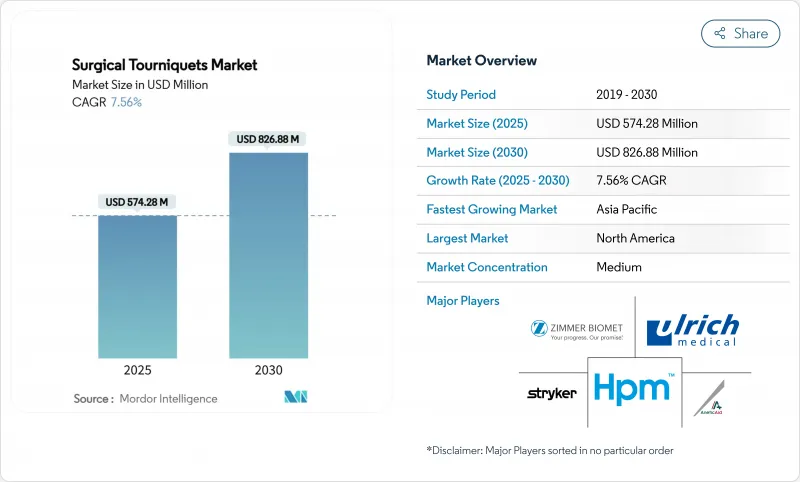

Surgical Tourniquets - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The surgical tourniquets market generated USD 574.28 million in 2025 and is on track to reach USD 826.88 million by 2030, reflecting a 7.56% CAGR through the forecast window.

Momentum stems from three intersecting forces: rising trauma caseloads linked to road accidents, sustained modernization of military medical corps, and quick uptake of limb-occlusion-pressure (LOP) technology that lowers the incidence of nerve injury during surgery. Emergency medical services now integrate tourniquet deployment into pre-hospital protocols after conflict data proved a 57.1% success rate in combat scenarios. Market penetration also benefits from infection-control mandates that heighten demand for single-use cuffs and from console-based systems that automate pressure adjustment, reducing litigation exposure for hospitals and ambulatory surgery centers.

Global Surgical Tourniquets Market Trends and Insights

Rising Trauma & Road-Accident Surgeries

Military casualty data, notably from the Russia-Ukraine conflict, validated tourniquet efficacy and spurred civilian EMS adoption. Field studies show mass-casualty tourniquet placement times under two minutes, a capability increasingly embedded in paramedic curricula worldwide. The Combat Application Tourniquet consistently achieves superior arterial occlusion when applied over clothing, a critical advantage for first responders wearing protective gear. Civilian uptake accelerates via STOP THE BLEED campaigns, and county EMS agencies in Texas deployed abdominal aortic junctional devices in 2025 for non-compressible hemorrhage control. Evidence across 4,095 civilian trauma cases shows a 52% mortality reduction without higher amputation risk when tourniquets are used pre-hospital. This cross-sector momentum widens the surgical tourniquets market beyond operating rooms into pre-hospital care.

Growth in Elective Orthopedic & Joint-Replacement Volumes

Private hospital networks in India alone are adding up to 2,500 beds in fiscal 2025, with 11-12% revenue growth that lifts joint-replacement caseloads. Aging demographics and broader insurance coverage support higher procedure volumes, while medical tourism now contributes 10-12% of hospital top lines across Asia-Pacific. Study data reveal that tourniquet use in total knee arthroplasty cuts intraoperative blood loss but slightly increases postoperative bruising.Consequently, surgeons gravitate to pressure-feedback consoles that calibrate inflation to LOP readings, mitigating tissue-related complications. Silicone ring designs also gain favor because they extend surgical fields, a benefit in bilateral knee work.

Nerve-/Tissue-Damage Litigation Risk

Meta-analyses show tourniquet use during ACL reconstruction elevates postoperative drainage by 100 ml and increases short-term pain, sharpening plaintiff arguments in malpractice suits. Cardiac-cycle efficiency drops markedly during inflation under general anesthesia, adding peri-operative risk factors. Insurers are now pricing premiums against hospital adoption rates of pressure-feedback consoles. Legal precedents increasingly oblige facilities to log pressure duration, prompting procurement of devices with automated audit trails. Vendors that bundle extended warranties and indemnification clauses gain an edge as hospitals hedge liability in the surgical tourniquets market.

Other drivers and restraints analyzed in the detailed report include:

- Hospital & ASC Capacity Expansion in Emerging Markets

- Adoption of LOP-Smart Tourniquet Systems to Cut Nerve Injuries

- Shortage of Staff Trained in Optimal Pressure Management

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Pneumatic devices controlled 54.28% of the surgical tourniquets market in 2024 owing to reliable inflation control and established surgeon preference. Disposable sterile cuffs, however, are growing at an 8.78% CAGR as infection-control guidelines push operating rooms toward single-use supplies. Re-usable cuffs now face performance audits that track cross-contamination events, amplifying the shift.

Hospitals that migrated to single-use cuffs during pandemic conservation mandates report 27% lower sterilization labor cost. Simultaneously, intelligent cuffs embedded with RFID facilitate automatic pairing with smart pumps, ensuring pressure accuracy logs match individual patients. Waterproof drape innovations further reduce skin burns in knee arthroscopy, improving patient satisfaction and accelerating adoption.

Lower-limb orthopedic surgery accounted for 62.84% of the surgical tourniquets market size in 2024, supported by sustained growth in knee and hip replacements. Nonetheless, trauma and battlefield care registers the highest CAGR at 9.18%, thanks to new military field kits and EMS protocols that stipulate tourniquet use within two minutes of extremity hemorrhage.

Combat casualty research sparked design improvements such as junctional abdominal devices for pelvic bleeding, broadening indication scope. Concurrently, upper-limb demand remains stable through wrist reconstruction and micro-vascular flap procedures, while plastic surgeons adopt silicone ring systems to expand incision visibility without raising pressure.

The Surgical Tourniquets Market is Segmented by Product Type (Pneumatic Tourniquet Systems, Intelligent LOP-Controlled Systems, and More), by Application (Lower-Limb Orthopedic Surgery, Upper-Limb Orthopedic Surgery, and More), by End User (Hospitals and Trauma Centers, Ambulatory Surgery Centers, and More), by Technology (Single-Channel (1-Cuff) Consoles, and More) and Geography (North America, Europe, Asia-Pacific, and More).

Geography Analysis

North America's 47.52% share in 2024 rests on advanced trauma systems, defense procurement, and early approval pathways such as FDA 510(k) expedited reviews, but it also sees a nascent shift toward tourniquet-less protocols in select orthopedic centers. Regional sales therefore tilt toward consoles with adaptive pressure curves that reassure surgeons wary of litigation. Texas county EMS adoption of junctional tourniquets for non-compressible bleeds underscores continuing growth in pre-hospital niches. Corporate consolidation, illustrated by Stryker's USD 4.9 billion Inari Medical purchase, extends competitive breadth into thrombectomy-a logical adjacency to bleeding-control technologies.

Asia-Pacific records the fastest CAGR at 9.69%, fueled by USD 1.75 billion bed-expansion programs across Indian hospital networks and by regulatory harmonization that eases device approvals across ASEAN. Medical-tourism inflows fortify procedure volumes, while government initiatives such as e-medical visas for 167 countries further widen access. Domestic manufacturing drives price competition; India's Make-in-India framework encourages local sourcing, which presses multinationals to establish joint ventures or risk market share erosion.

Europe maintains steady uptake under cohesive medical-device regulations and growing preference for premium LOP consoles. Ulrich medical allocated EUR 5 million in 2024 to scale production, reporting a 12% revenue uplift to EUR 150 million-evidence that medium-sized players can prosper in specialized niches. Middle East and Africa funnel petro-revenues into trauma-center upgrades, and South America's private-hospital groups cautiously phase in smart consoles, though macroeconomic volatility remains a headwind. Collectively, these dynamics distribute growth pockets that vendors must navigate with agile channel strategies to capture share in the surgical tourniquets market.

- Stryker

- Zimmer Biomet

- ulrich medical

- Hammarplast Medical

- Anetic Aid

- VBM Medizintechnik

- Delfi Medical Innovations

- Daesung Maref

- HemaClear (OHK Medical Devices Inc.)

- DESSILLIONS & DUTRILLAUX

- Riester

- SAM Medical

- Tactical Medical Solutions

- CAT Resources (C-A-T)

- Dynarex

- Medline Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising trauma & road-accident surgeries

- 4.2.2 Growth in elective Orthopedic & joint-replacement volumes

- 4.2.3 Expansion of hospitals & ASC capacity in emerging economies

- 4.2.4 Adoption of LOP-smart tourniquet systems to cut nerve injuries

- 4.2.5 Military demand for compact field tourniquets

- 4.2.6 Shift to blood-sparing outpatient arthroplasty protocols

- 4.3 Market Restraints

- 4.3.1 Nerve-/tissue-damage litigation risk

- 4.3.2 Shortage of staff trained in optimal pressure management

- 4.3.3 Move toward tourniquet-less arthroscopy & TKA techniques

- 4.3.4 Cost spike from single-use & re-processing regulations

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Product Type

- 5.1.1 Pneumatic Tourniquet Systems

- 5.1.2 Intelligent LOP-controlled Systems

- 5.1.3 Elastic / Silicone-ring Tourniquets

- 5.1.4 Disposable / Sterile Cuffs

- 5.1.5 Re-usable Cuffs

- 5.1.6 Accessories

- 5.2 By Application

- 5.2.1 Lower-Limb Orthopedic Surgery

- 5.2.2 Upper-Limb Orthopedic Surgery

- 5.2.3 Trauma & Battlefield Stabilisation

- 5.2.4 Other Surgical Specialities

- 5.3 By End User

- 5.3.1 Hospitals & Trauma Centres

- 5.3.2 Ambulatory Surgery Centres

- 5.3.3 Military / Defence Medical Units

- 5.3.4 Other End Users (Sports clinics, EMS)

- 5.4 By Technology

- 5.4.1 Single-Channel (1-cuff) Consoles

- 5.4.2 Multi-Channel (2-4 cuff) Consoles

- 5.4.3 Integrated Pressure-Feedback Software

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Stryker Corporation

- 6.3.2 Zimmer Biomet Holdings Inc.

- 6.3.3 ulrich medical

- 6.3.4 Hammarplast Medical

- 6.3.5 Anetic Aid

- 6.3.6 VBM Medizintechnik

- 6.3.7 Delfi Medical Innovations

- 6.3.8 Daesung Maref

- 6.3.9 HemaClear (OHK Medical Devices Inc.)

- 6.3.10 DESSILLIONS & DUTRILLAUX

- 6.3.11 Riester

- 6.3.12 SAM Medical

- 6.3.13 Tactical Medical Solutions

- 6.3.14 CAT Resources (C-A-T)

- 6.3.15 Dynarex Corporation

- 6.3.16 Medline Industries Ltd.

7 Market Opportunities & Future Outlook