PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851192

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851192

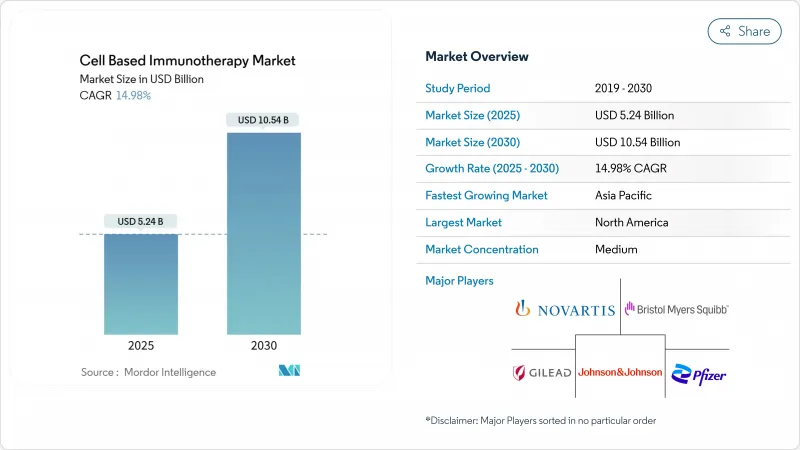

Cell Based Immunotherapy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The cell-based immunotherapy market generated USD 5.24 billion in 2025 and is forecast to reach USD 10.54 billion by 2030, yielding a 14.98% CAGR.

CAR-T platforms now move from last-line rescue to second-line standard care, encouraged by eight novel cellular products cleared by the FDA in 2024, including the first mesenchymal stromal therapy, Ryoncil. Outpatient infusion protocols are further reshaping the cell-based immunotherapy market by lowering total care costs; registry data show that 25% of outpatients avoid a 30-day hospital admission. Autologous products held 89.55% of 2024 revenue, yet the allogeneic segment is growing at 30.25% CAGR, reflecting demand for off-the-shelf convenience. Therapeutic focus remains on B-cell malignancies, which comprised 45.53% of treated cases in 2024, but renal cell carcinoma leads the next indication wave with a 25.15% CAGR nature.com. North America commanded 47.72% of 2024 spending, while Asia-Pacific is expanding fastest at 27.22% CAGR as local manufacturers cut production costs.

Global Cell Based Immunotherapy Market Trends and Insights

Surging Cancer Prevalence and Earlier-Line Use Approvals

Second-line adoption accelerated when Carvykti secured an FDA label expansion after CARTITUDE-4 showed a 45% mortality risk reduction against standard care. Long-term follow-up from CARTITUDE-1 found 33% of recipients alive and progression-free at 5 years, suggesting functional cure potential. The Centers for Medicare & Medicaid Services plans a 17% base-rate increase for CAR-T in FY 2026, improving hospital economics and accelerating physician adoption. Earlier-line positioning enlarges the cell-based immunotherapy market by treating fitter patients who tolerate shorter manufacturing windows and experience fewer adverse events. Expanded labels also translate into broader payer coverage, enhancing volume growth across oncology centers.

Rapid Advances in Gene-Editing and Viral-Vector Engineering

Regulatory precedent for CRISPR editing was set in 2024 when the FDA cleared the first Cas9-modified therapies for hemoglobinopathies. IL-15-armored GPC3 CAR-T cells subsequently achieved 66% disease-control rates in solid tumors, validating cytokine-enhanced constructs. Dual-target designs such as Johnson & Johnson's CD19/CD20 program posted 100% objective responses in first-line large B-cell lymphoma. Meanwhile, next-generation vector platforms standardize lentiviral manufacture, lowering per-dose cost curves. These innovations enhance persistence, reduce relapse risk and increase manufacturing throughput, directly expanding the cell-based immunotherapy market.

Complex, Fragile Supply-Chain and Talent Shortages

The U.S. Government Accountability Office highlights that many contract development and manufacturing organizations run under capacity because of GMP workforce gaps. Lentiviral vector shortages threaten production continuity, with demand outstripping supply unless scale-up inefficiencies are corrected. Automation reduces but does not eliminate expert-operator needs, and most skilled technicians cluster around a handful of U.S. and EU hubs, raising regional fragility during global travel disruptions. Capital-intensive cold-chain networks compound risk, as any deviation jeopardizes product viability, potentially delaying treatment for high-acuity patients and slowing revenue recognition across the cell-based immunotherapy market.

Other drivers and restraints analyzed in the detailed report include:

- Expanding Reimbursement Frameworks for CAR-T Launches

- Big-Pharma M&A, Licensing and Capacity Build-Outs

- Cytokine-Release-Syndrome Management Liability Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Autologous constructs generated 89.55% of 2024 revenue, anchoring the cell-based immunotherapy market size at USD 4.70 billion that year. Legendary outcomes and well-established regulatory templates sustain hospital preference, though each patient-specific batch still demands specialized logistics and lengthy processing. Meanwhile, the allogeneic segment is forecast to advance at 30.25% CAGR, expanding its contribution to the cell-based immunotherapy market size by an incremental USD 1.9 billion between 2025 and 2030. Regulatory precedent was cemented when the FDA cleared Ryoncil, the first off-the-shelf mesenchymal stromal product for pediatric acute graft-versus-host disease fda.gov.

Automation is narrowing cost differentials; Cellares's Cell Shuttle shows 80% space efficiency and 75% labor savings, translating into lower all-in COGS that push the allogeneic price curve below USD 150,000 per dose. Universal CAR-NK pipelines reduce graft-versus-host-disease risk and simplify donor screening. Astellas and Poseida alone committed USD 800 million to expand allogeneic programs that can be stock-piled like biologics, significantly expanding treatment capacity. As payer scrutiny intensifies, lower-priced, off-the-shelf constructs could erode autologous incumbency, though most oncologists still rely on empirical survival data before switching.

The Cell Based Immunotherapy Market Report is Segmented by Therapy (Autologous and Allogeneic), Primary Indication (B-Cell Malignancies, Prostate Cancer, Renal Cell Carcinoma, Liver Cancer, and More), and Geography (North America, Europe, Asia-Pacific, Middle East and Africa, South America). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North American providers benefit from advanced reimbursement certainty and a deep referral network, keeping treatment volume dense despite workforce shortages and vector bottlenecks. CMS payment increases and multiple domestic expansion projects can absorb earlier-line demand without severe backlog, positioning the region for stable double-digit growth. Academic centers such as UCSF are simultaneously exploring autoimmune applications, which may diversify revenue streams outside oncology.

Asia-Pacific markets embrace policy incentives that support domestic manufacturing sovereignty, exemplified by China's high trial density and India's cost-efficient mobile facilities. Local price points under USD 60,000 broaden eligibility for middle-income patients; however, center accreditation lags behind population need, prompting partnerships between Western license holders and regional contract manufacturers. Japan and South Korea offer streamlined regulatory approvals that encourage multinationals to site facilities domestically, yet supply chain resilience still hinges on imported vectors and single-use bioreactor consumables.

European activity remains steady, driven by centralized regulatory processes and incremental reimbursement reforms toward performance-linked payment. Localization strategies by Novartis and Bristol Myers Squibb mitigate logistical complexity, and academic cell-manufacture programs provide lower-cost options for national health services. The EBMT reports sustained CAR-T activity growth as transplant numbers flatten, underscoring shifting therapeutic preferences. Nonetheless, cost-containment pressures limit broad second-line use until outcomes data mature, moderating the region's contribution to the expanding cell-based immunotherapy market.

- Novartis

- Gilead Sciences Inc (Kite Pharma)

- Bristol-Myers Squibb

- Johnson & Johnson

- Pfizer

- Roche

- Legend Biotech Corp.

- Bluebird Bio

- JW Therapeutics Co. Ltd

- Autolus Therapeutics plc

- Adaptimmune Therapeutics plc

- Gamida Cell Ltd

- Atara Biotherapeutics Inc.

- Precision BioSciences Inc.

- Tessa Therapeutics Ltd

- Caribou Biosciences Inc.

- Mustang Bio Inc.

- Sorrento Therapeutics

- Miltenyi Biotec B.V. & Co. KG

- Celyad Oncology SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Cancer Prevalence And Earlier-Line Use Approvals

- 4.2.2 Rapid Advances In Gene-Editing & Viral-Vector Engineering

- 4.2.3 Expanding Reimbursement Frameworks For CAR-T Launches

- 4.2.4 Big-Pharma M&A, Licensing And Capacity Build-Outs

- 4.2.5 Point-Of-Care Micro-Factories Slashing Vein-To-Vein Cycle

- 4.3 Market Restraints

- 4.3.1 Complex, Fragile Supply-Chain & Talent Shortages

- 4.3.2 Cytokine-Release-Syndrome Management Liability Risk

- 4.3.3 Viral-Vector Raw-Material Bottlenecks Constrain Scale-Up

- 4.4 Porter's Five Forces

- 4.4.1 Threat of New Entrants

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Bargaining Power of Suppliers

- 4.4.4 Threat of Substitutes

- 4.4.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Therapy

- 5.1.1 Autologous

- 5.1.2 Allogeneic

- 5.2 By Primary Indication

- 5.2.1 B-cell Malignancies

- 5.2.2 Prostate Cancer

- 5.2.3 Renal Cell Carcinoma

- 5.2.4 Liver Cancer

- 5.2.5 Other Indications

- 5.3 Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.2 Europe

- 5.3.2.1 Germany

- 5.3.2.2 United Kingdom

- 5.3.2.3 France

- 5.3.2.4 Italy

- 5.3.2.5 Spain

- 5.3.2.6 Rest of Europe

- 5.3.3 Asia-Pacific

- 5.3.3.1 China

- 5.3.3.2 Japan

- 5.3.3.3 India

- 5.3.3.4 South Korea

- 5.3.3.5 Australia

- 5.3.3.6 Rest of Asia-Pacific

- 5.3.4 Middle East and Africa

- 5.3.4.1 GCC

- 5.3.4.2 South Africa

- 5.3.4.3 Rest of Middle East and Africa

- 5.3.5 South America

- 5.3.5.1 Brazil

- 5.3.5.2 Argentina

- 5.3.5.3 Rest of South America

- 5.3.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Novartis AG

- 6.3.2 Gilead Sciences Inc (Kite Pharma)

- 6.3.3 Bristol-Myers Squibb Co.

- 6.3.4 Johnson & Johnson (Janssen)

- 6.3.5 Pfizer Inc.

- 6.3.6 F. Hoffmann-La Roche Ltd

- 6.3.7 Legend Biotech Corp.

- 6.3.8 Bluebird Bio Inc.

- 6.3.9 JW Therapeutics Co. Ltd

- 6.3.10 Autolus Therapeutics plc

- 6.3.11 Adaptimmune Therapeutics plc

- 6.3.12 Gamida Cell Ltd

- 6.3.13 Atara Biotherapeutics Inc.

- 6.3.14 Precision BioSciences Inc.

- 6.3.15 Tessa Therapeutics Ltd

- 6.3.16 Caribou Biosciences Inc.

- 6.3.17 Mustang Bio Inc.

- 6.3.18 Sorrento Therapeutics Inc.

- 6.3.19 Miltenyi Biotec B.V. & Co. KG

- 6.3.20 Celyad Oncology SA

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment