PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851233

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851233

Food Intolerance Products - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

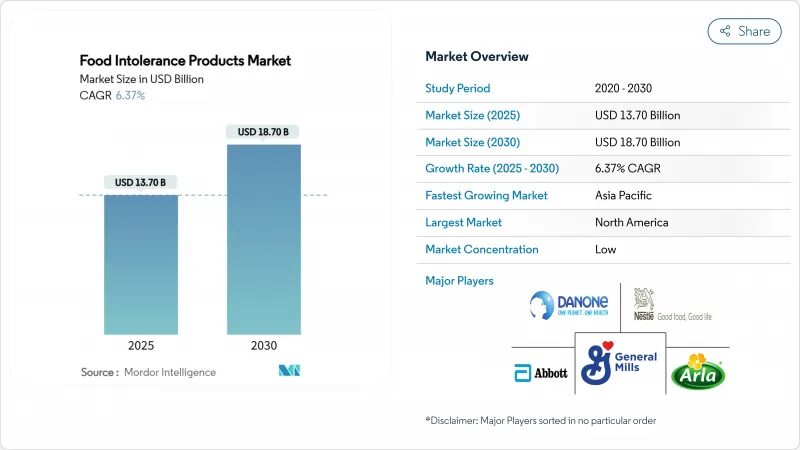

The food intolerance products market is expected to reach USD 13.7 billion in 2025 and grow to USD 18.7 billion by 2030, reflecting a solid 6.37% CAGR.

The growth trajectory is driven by stringent food-safety regulations, increased consumer awareness of diet-related health concerns, and a steady rise in medically diagnosed allergies. The 2024 update to the U.S. gluten-free rule for fermented and hydrolyzed foods has reduced compliance uncertainties, facilitating new product launches and building trust among sensitive consumers. While North America maintains its leadership due to early regulatory clarity and high label literacy, urban households in the Asia-Pacific region are driving the fastest volume growth, supported by rising incomes and expanding e-commerce. Manufacturers are prioritizing investments in cost-efficient plant-based ingredients and precision fermentation technologies to enhance taste parity with conventional foods, a critical factor for ensuring repeat purchases. Retailers are optimizing shelf space by allocating premium end-caps and algorithm-driven search placements to brands that meet clean-label, allergen-free, and organic standards. These strategic adjustments are expected to support long-term volume growth in the free-from foods market.

Global Food Intolerance Products Market Trends and Insights

Premiumization of gluten-free bakery products

The gluten-free bakery market is transitioning from basic dietary compliance to delivering enhanced sensory experiences and improved nutritional value. For instance, in 2024, General Mills introduced Annie's Super! Mac, featuring 15 grams of protein and 6 grams of fiber per serving through yellow pea integration. This highlights how manufacturers are advancing gluten-free offerings beyond traditional wheat substitutes. Premium positioning enables manufacturers to offset higher production costs while meeting consumer demand for products that match the quality of conventional options. This approach is particularly effective in developed markets, where consumers are willing to pay a premium for perceived health benefits and superior taste. Market analysis indicates that this premiumization strategy is expanding into confectionery and snack segments, unlocking new revenue opportunities for established food manufacturers. However, the sustainability of this trend relies on continuous advancements in ingredient technology and processing methods to deliver conventional-like experiences without compromising 'free-from' attributes.

Rising prevalence of food intolerances and allergies

The market for food allergies and intolerances is experiencing notable growth, driven by evolving consumer lifestyles and health awareness. Factors such as dietary changes, hygiene practices, environmental exposures, and shifts in gut microbiomes are being actively studied as contributors to this trend. In 2024, the Food Standards Agency reported that 12% of consumers in the United Kingdom (excluding Scotland) were affected by food intolerances, highlighting the scale of the issue. In response to this growing concern, the FDA implemented updated 2024 regulations for gluten-free labeling of fermented and hydrolyzed foods. These updates aim to address previous regulatory gaps that inadvertently exposed celiac disease patients to gluten, thereby enhancing consumer safety and trust. The prevalence of food intolerances among younger demographics and urban populations underscores a stable and growing demand base, which is expected to evolve into increased purchasing power over time. Furthermore, the healthcare sector's recognition of food allergies as a significant public health challenge is driving regulatory advancements, particularly in the area of transparent labeling standards. This evolving regulatory environment is creating substantial growth opportunities for manufacturers in the 'free-from' food segment, enabling them to cater to the rising demand for allergen-free and intolerance-friendly products.

Higher manufacturing and certification costs limits the growth

Free-from food manufacturers face ongoing cost challenges. Achieving gluten-free certification involves extensive documentation, facility upgrades, and continuous compliance management. According to the FDA's regulatory impact analysis, the annual compliance cost for gluten-free labeling is approximately USD 8.8 million. These costs disproportionately impact smaller manufacturers that lack economies of scale. The need for specialized ingredient sourcing, dedicated production lines, and stringent testing protocols creates structural cost disadvantages, hindering market entry in price-sensitive segments. This issue is particularly significant in emerging markets, where consumers have limited tolerance for premium pricing and regulatory frameworks for free-from foods are still evolving. However, advancements in manufacturing technologies and ingredient alternatives are gradually narrowing these cost disparities. Innovations such as precision fermentation and alternative protein technologies present opportunities to achieve cost parity.

Other drivers and restraints analyzed in the detailed report include:

- Increased consumer awareness and demand for label transparency

- Growth in plant-based and dairy-free diets

- Challenges in achieving taste and texture parity with conventional foods

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Dairy and dairy alternatives command 30.45% market share in 2024, reflecting the segment's maturity and broad consumer acceptance across multiple dietary restriction categories. This segment's success is attributed to its ability to simultaneously address the needs of lactose-intolerant consumers, individuals with dairy allergies, and those following plant-based diets, thereby capturing a broader market compared to single-restriction categories. Confectionery products represent the fastest-growing segment, achieving a 7.79% CAGR through 2030, driven by premiumization trends and innovative product development beyond traditional sugar-free offerings. Meanwhile, the bakery segment demonstrates consistent growth, supported by advancements in gluten-free products. Similarly, the meat and seafood categories benefit from innovations in plant-based proteins and alternative protein technologies.

Rising awareness of lactose intolerance symptoms and diagnoses has significantly increased the demand for lactose-free products across multiple food categories. In response, manufacturers are expanding their product portfolios to include lactose-free options in key categories such as milk, yogurt, cheese, and ice cream. For instance, in January 2023, Califia Farms introduced organic almond milk and oat milk products made with simple ingredients like purified water, sea salt, and almonds, excluding added oils or gums, to cater to lactose-intolerant consumers seeking clean-label alternatives. Additionally, sauces, condiments, and dressings present a growing opportunity as manufacturers develop 'free-from' versions of traditionally challenging categories. Furthermore, specialty products targeting niche dietary requirements contribute to the overall diversification of the market.

Gluten-free foods maintain market leadership with a 57.63% share in 2024, supported by established consumer awareness and regulatory standardization. However, lactose-free products are experiencing faster growth, with an 8.15% CAGR forecasted through 2030, reflecting a shift in consumer preferences beyond celiac disease management. The lactose-free segment capitalizes on its broader demographic reach, as lactose intolerance impacts a larger global population compared to gluten sensitivity, presenting a significant market opportunity. The FDA's updated gluten-free labeling requirements for fermented and hydrolyzed foods in 2024 provide manufacturers with clearer compliance pathways, potentially stabilizing growth in the gluten-free segment while reducing regulatory uncertainties.

Labeling categories are expanding to include emerging free-from claims such as sugar-free, preservative-free, and allergen-specific designations, addressing increasingly sophisticated consumer dietary demands. The integration of multiple free-from claims on a single product offers premium market positioning opportunities but also introduces greater manufacturing complexities and higher certification costs. Singapore's 2025 food labeling regulations highlight this regulatory evolution by establishing clear standards for gluten-free claims and prohibiting misleading statements, thereby supporting market standardization and enhancing consumer confidence.

The Food Intolerance Products Market Report is Segmented by Product Type (Dairy and Dairy Alternatives, and More), Labeling Type (Gluten-Free Food, Lactose-Free Food, and Others), Category (Conventional and Organic), Distribution Channel (Supermarkets/Hypermarkets, and More), and Geography (North America, Europe, Asia-Pacific, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2024, North America secured the largest regional revenue share at 35.86%, driven by stringent allergen-label regulations, a high prevalence of medically diagnosed intolerances, and a well-established chilled-chain logistics network. Collaborative efforts between research institutions and ingredient suppliers in the region are advancing texture-enhancing hydrocolloids and enzyme systems, which are rapidly entering commercial markets. The growing emphasis on ESG reporting has elevated the shelf presence of 'free-from' products with organic or sustainably sourced certifications, further strengthening North America's market leadership.

Asia-Pacific is the fastest-growing region, with an anticipated CAGR of 8.45% through 2030. Urban Millennials in key markets such as China, India, and Thailand are increasingly replacing dairy milk with plant-based alternatives, a trend fueled by social media influencer marketing. Singapore's planned alignment of gluten-free standards with Codex by 2025 is expected to streamline cross-border e-commerce for brands exporting from Australia and the United States. Despite disparities in purchasing power across sub-regions, the adoption of mobile payments and the rise of micro-fulfillment centers are enabling 'free-from' brands to overcome traditional distribution challenges, driving the region's significant growth in the free-from foods market.

Europe combines established organic consumption patterns with certain distribution inefficiencies that limit full product availability. Countries like Germany and Sweden benefit from strong health-food store networks. The EU's stringent allergen-label regulations, among the most rigorous globally, provide consumers with high confidence in both domestic and imported 'free-from' products. In contrast, Latin America and the Middle East and Africa are in the early stages of market adoption. However, the expanding middle class and increasing exposure to Western dietary trends in these regions indicate growth potential, particularly as regulatory frameworks advance and cold-chain infrastructure improves.

- General Mills Inc.

- Danone S.A.

- Abbott Laboratories

- Nestle S.A.

- Arla Foods amba

- Beyond Meat Inc.

- Green Valley Creamery

- Blue Diamond Growers

- Oatly Group AB

- Dr. Schar AG / SPA

- The Hain Celestial Group, Inc.

- Cabot Creamery Corporation

- Barilla G.e.R. Fratelli SpA

- Conagra Brands, Inc.

- Kraft Heinz Company

- Lactalis Group

- Otsuka Holdings Co., Ltd. (Daiya Foods Inc.)

- Amy's Kitchen Inc.

- SunOpta Inc.

- Oetker Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization of gluten-free bakery products

- 4.2.2 Rising prevalence of food intolerances and allergies

- 4.2.3 Increased consumer awareness and demand for label transparency

- 4.2.4 Growth in plant-based and dairy-free diets

- 4.2.5 Expansion of online and specialty retail channels

- 4.2.6 Demand for convenient and ready-to-eat products

- 4.3 Market Restraints

- 4.3.1 Higher manufacturing and certification costs limits the growth

- 4.3.2 Challenges in achieving taste and texture parity with conventional foods

- 4.3.3 Limited availability in emerging markets

- 4.3.4 Consumer skepticism and confusion over labeling

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Dairy and Dairy Alternatives

- 5.1.2 Bakery Products

- 5.1.3 Confectionery Products

- 5.1.4 Meat and Seafood Products

- 5.1.5 Sauces, Condiments and Dressings

- 5.1.6 Other Product Types

- 5.2 By Labeling Type

- 5.2.1 Gluten-Free Food

- 5.2.2 Lactose-Free Food

- 5.2.3 Others

- 5.3 By Category

- 5.3.1 Conventional

- 5.3.2 Organic

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets/Hypermarkets

- 5.4.2 Health-Food Stores

- 5.4.3 Convenience and Grocery Stores

- 5.4.4 Online Retail Stores

- 5.4.5 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 General Mills Inc.

- 6.4.2 Danone S.A.

- 6.4.3 Abbott Laboratories

- 6.4.4 Nestle S.A.

- 6.4.5 Arla Foods amba

- 6.4.6 Beyond Meat Inc.

- 6.4.7 Green Valley Creamery

- 6.4.8 Blue Diamond Growers

- 6.4.9 Oatly Group AB

- 6.4.10 Dr. Schar AG / SPA

- 6.4.11 The Hain Celestial Group, Inc.

- 6.4.12 Cabot Creamery Corporation

- 6.4.13 Barilla G.e.R. Fratelli SpA

- 6.4.14 Conagra Brands, Inc.

- 6.4.15 Kraft Heinz Company

- 6.4.16 Lactalis Group

- 6.4.17 Otsuka Holdings Co., Ltd. (Daiya Foods Inc.)

- 6.4.18 Amy's Kitchen Inc.

- 6.4.19 SunOpta Inc.

- 6.4.20 Oetker Group

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK