PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851259

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851259

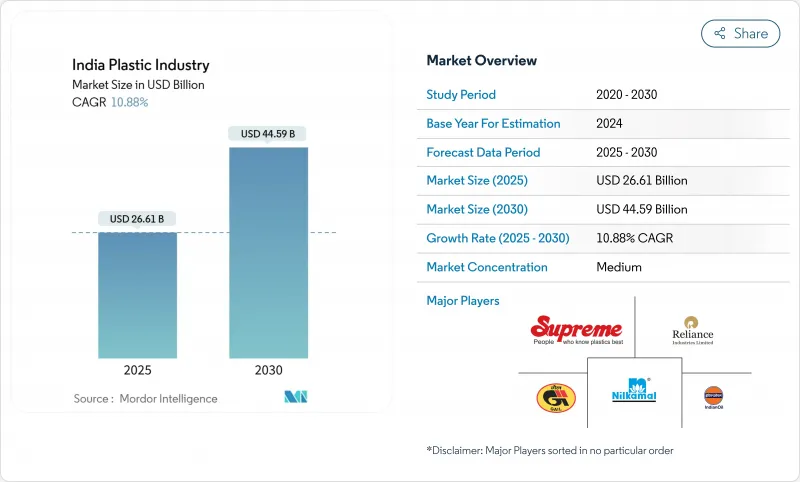

India Plastic Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The India plastic industry market is currently valued at USD 26.61 billion in 2025 and is forecast to reach USD 44.59 billion by 2030, translating to a 10.88% CAGR.

Strong public-sector incentives such as the Production-Linked Incentive scheme, large-scale infrastructure programs and accelerating consumer demand across packaging, construction and mobility are sustaining this double-digit trajectory. Western India remains the consumption epicenter, powered by Gujarat's and Maharashtra's dense petrochemical clusters, while specialty grades are gaining share as brands look for lightweighting and recyclability. Supply-side additions in polyolefins and PVC, amplified by recent brownfield and greenfield investments, are easing the country's long-standing dependence on imports. Meanwhile, rising waste-management regulations, volatile feedstock costs and rapid adoption of digital production controls are shaping a sharper focus on operational efficiency and circularity.

India Plastic Industry Market Trends and Insights

Government PLI Scheme Accelerating Polymer Capacity Expansions in Gujarat

Investment incentives under the PLI program are funneling unprecedented capital into Gujarat's Jamnagar-Dahej petrochemical corridor. Projects such as Reliance Industries' 1.5 MTPA PVC complex and Adani's 2 MTPA PVC build-out are expected to narrow the 2.5 million-tonne local supply gap by 2027. Alongside output gains, firms are deploying chemical-recycling technologies that convert mixed plastic waste into ISCC-Plus certified resins, positioning Gujarat as a regional circular-economy hub. Allied logistics upgrades, including dedicated polymer rail corridors, further strengthen the material flow from western coast ports to inland processors.

Quick-Commerce Boom Driving Demand for High-Rigidity Food Containers

Same-hour grocery delivery is reshaping rigid packaging specifications. Operators require containers that resist impact, maintain barrier integrity under rapid temperature swings and stack efficiently in micro-fulfilment centers. Injection-grade polypropylene and clarified random copolymers dominate current supply, but brand owners are piloting mono-material designs to comply with 2026 recyclability targets. Major rigid packaging converters have announced capacity additions in Maharashtra and Telangana to address forecast container demand growth above 15% annually.

Single-Use Plastic Ban Escalating Compliance Costs for FMCG Packagers

Ban enforcement has removed 19 disposable items from legal circulation, forcing brands to pivot toward paper laminates, biodegradable films or thicker reusable formats. Substitute materials cost at least 40% more than legacy LDPE flexibles, squeezing price-sensitive categories such as condiments and on-the-go beverages. Smaller converters report capital-expenditure hurdles in retrofitting extrusion-coating and lamination lines for alternative substrates.

Other drivers and restraints analyzed in the detailed report include:

- Swachh Bharat Phase II Fueling Urban HDPE Pipe Replacement

- EV Lightweighting Strategy Boosting Engineering Plastics in Two-Wheelers

- Volatile Naphtha Feedstock Prices from Middle-East Tensions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyethylene retained a 34% slice of the India plastic industry market in 2024, anchored by film and blow-molded container demand. High-density grades grew faster than low-density grades owing to pipe, cap and closure applications. The India plastic industry market size for biodegradable/bio-plastics is projected to widen at a 12.3% CAGR, reaching USD 1.81 billion by 2030, as brands adopt PLA, PBS and PHA blends in serviceware and personal-care packaging. Polypropylene remains intrinsic to woven sacks, appliance housings and automotive trim, while PVC's future hinges on the timely start-up of domestic chlor-alkali expansions.

Circularity gains momentum through mechanical and chemical recycling. India's PET bottle stream already touches a 95% recovery rate, supported by well-organized informal collection networks. New depolymerization ventures in Gujarat intend to close the loop on polyester textiles, signalling a shift from export-oriented bottle flakes toward domestic resin circularity.

Biodegradable grades capture most venture attention, yet bio-based drop-in resins such as bio-PE and bio-PET are scaling faster in beverage and personal-care lines because they slot into existing molds without process change. Local compounders are experimenting with lignin-filled PLA and starch-grafted PBAT to cut cost premiums below 70% versus fossil-based equivalents. Certification schemes under the India Plastics Pact require 50% recycled content or biogenic feedstock in rigid packaging by 2030, pushing brand owners to lock in forward supply contracts.

Pilot-scale projects in Karnataka and Tamil Nadu demonstrate enzymatic recycling of multilayer films into feedstock monomers. Although volumes remain small, successful commercialization would open pathways to recover up to 2 million tonnes of composite waste annually, mitigating landfill pressure.

India Plastic Industry Market Report Segments the Industry Into by Polymer Type (Polyethylene, Polypropylene, and More), by Specialty and Bioplastics Type (Biodegradable Bioplastics, Bio-Based Non-Biodegradable Plastics), by Processing Technology (Injection Molding, Blow Molding, and More), and by Application (Packaging, Automotive and Transportation, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Reliance Industries Ltd

- Indian Oil Corporation Ltd

- GAIL (India) Ltd

- Haldia Petrochemicals Ltd

- Supreme Industries Ltd

- Nilkamal Ltd

- Time Technoplast Ltd

- Jain Irrigation Systems Ltd

- Kingfa Science and Technology India Ltd

- Mayur Uniquoters Ltd

- Plastiblends India Ltd

- Responsive Industries Ltd

- Safari Industries (India) Ltd

- VIP Industries Ltd

- Wim Plast Ltd (Cello)

- Cosmo Films Ltd

- Manjushree Technopack Ltd

- Ester Industries Ltd

- SRF Ltd

- Jindal Poly Films Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Government PLI Scheme Accelerating Polymer Capacity Expansions in Gujarat

- 4.2.2 Quick-Commerce Boom Driving Demand for High-Rigidity Food Containers

- 4.2.3 Swachh Bharat Phase-II Fueling Urban HDPE Pipe Replacement

- 4.2.4 EV Lightweighting Strategy Boosting Engineering Plastics in Two-Wheelers

- 4.2.5 Pharma Export Surge in West India Raising Medical-Grade Resin Consumption

- 4.2.6 Tier-II Mall Construction Upsurge Increasing PVC Profiles and Cladding Demand

- 4.3 Market Restraints

- 4.3.1 Single-Use Plastic Ban Escalating Compliance Costs for FMCG Packagers

- 4.3.2 Volatile Naphtha Feedstock Prices from Middle-East Tensions

- 4.3.3 Inter-State Waste Rules Causing Logistic Bottlenecks and Capacity Under-Utilization

- 4.3.4 Consumer Backlash on Microplastics in Packaged Drinking Water

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory or Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Polymer Type

- 5.1.1 Polyethylene (LDPE, LLDPE, HDPE)

- 5.1.2 Polypropylene

- 5.1.3 Polyvinyl Chloride

- 5.1.4 Polyethylene Terephthalate (PET)

- 5.1.5 Polystyrene and EPS

- 5.1.6 Acrylonitrile Butadiene Styrene (ABS)

- 5.1.7 Polycarbonate

- 5.1.8 Others (PMMA, POM, etc.)

- 5.2 By Specialty and Bioplastics Type

- 5.2.1 Biodegradable Bioplastics (PLA, PHA, Starch Blends)

- 5.2.2 Bio-Based Non-Biodegradable Plastics (Bio-PE, Bio-PET)

- 5.3 By Processing Technology

- 5.3.1 Injection Molding

- 5.3.2 Blow Molding

- 5.3.3 Extrusion

- 5.3.4 Thermoforming

- 5.3.5 Rotational Molding

- 5.3.6 Compression Molding

- 5.3.7 Additive Manufacturing (3D Printing)

- 5.4 By Application

- 5.4.1 Packaging

- 5.4.1.1 Rigid Packaging

- 5.4.1.2 Flexible Packaging

- 5.4.2 Building and Construction

- 5.4.3 Automotive and Transportation

- 5.4.4 Electrical and Electronics

- 5.4.5 Agriculture and Irrigation

- 5.4.6 Healthcare and Pharmaceuticals

- 5.4.7 Consumer Goods and Housewares

- 5.4.8 Furniture and Bedding

- 5.4.9 Others (Textiles, Sports and Leisure)

- 5.4.1 Packaging

- 5.5 By Region (India)

- 5.5.1 West India (Gujarat, Maharashtra, Goa)

- 5.5.2 North India (Delhi-NCR, Uttar Pradesh, Punjab, Haryana, Rajasthan)

- 5.5.3 South India (Tamil Nadu, Karnataka, Telangana, Andhra Pradesh, Kerala)

- 5.5.4 East and North-East India (West Bengal, Odisha, Bihar, Assam and NE States)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Reliance Industries Ltd

- 6.4.2 Indian Oil Corporation Ltd

- 6.4.3 GAIL (India) Ltd

- 6.4.4 Haldia Petrochemicals Ltd

- 6.4.5 Supreme Industries Ltd

- 6.4.6 Nilkamal Ltd

- 6.4.7 Time Technoplast Ltd

- 6.4.8 Jain Irrigation Systems Ltd

- 6.4.9 Kingfa Science and Technology India Ltd

- 6.4.10 Mayur Uniquoters Ltd

- 6.4.11 Plastiblends India Ltd

- 6.4.12 Responsive Industries Ltd

- 6.4.13 Safari Industries (India) Ltd

- 6.4.14 VIP Industries Ltd

- 6.4.15 Wim Plast Ltd (Cello)

- 6.4.16 Cosmo Films Ltd

- 6.4.17 Manjushree Technopack Ltd

- 6.4.18 Ester Industries Ltd

- 6.4.19 SRF Ltd

- 6.4.20 Jindal Poly Films Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment