PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906930

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1906930

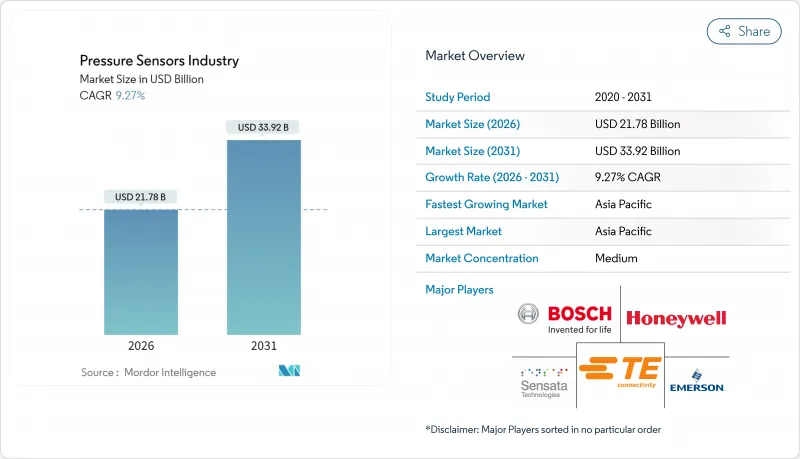

Pressure Sensors Industry - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The pressure sensors market was valued at USD 19.93 billion in 2025 and estimated to grow from USD 21.78 billion in 2026 to reach USD 33.92 billion by 2031, at a CAGR of 9.27% during the forecast period (2026-2031).

Strong demand stems from electrified power-train control, smart-factory retrofits, and disposable medical devices that require precise pressure monitoring for safety and efficiency. Electrification mandates in Asia-Pacific are accelerating adoption of high-accuracy barometric sensors in xEV battery-thermal systems, while Industry 4.0 upgrades across Europe and North America favor wireless nodes that cut installation cost. Medical device miniaturization, especially in cardiovascular catheters, is opening a sizeable opportunity for single-use MEMS designs that meet sterilization standards. At the same time, harsh-environment exploration-such as LNG carrier fleets-creates premium demand for silicon-carbide and optical technologies capable of surviving >175 °C process lines. Competitive intensity is rising: incumbents embed AI engines at the edge to defend margins, whereas Chinese white-label MEMS foundries scale volume and depress average selling prices.

Global Pressure Sensors Industry Trends and Insights

Rapid electrification of xEV power-train control systems driving high-accuracy barometric sensing

Electric vehicles use precision barometric sensors to detect cell swelling and manage heat, avoiding thermal runaway events that can cost OEMs up to USD 3,000 per vehicle. Sensor suppliers are hardening designs for >175 °C operation because silicon-carbide traction inverters will reach 50% penetration by 2027. Automotive demand is strongest in China, Japan, and South Korea where gigafactory capacity and government subsidies intersect to accelerate adoption.

Expansion of smart-factory retrofits boosting wireless sensor node demand

European and North American manufacturers are layering LoRaWAN and NB-IoT pressure nodes onto legacy equipment to enable predictive maintenance; low-power wide-area connections are forecast to exceed 3.5 billion by 2030. Assembly lines such as WIKA's gauge facility now incorporate more than 10,000 sensor variants in a single automated cell. Retrofit projects prioritize battery-powered nodes to avoid expensive conduit runs, a key factor behind the 12.8% CAGR in wireless uptake.

ASP erosion from Chinese white-label MEMS foundries

Firms such as MEMSensing posted 28.8%-36.85% revenue growth in 2024 while still running at a loss, underscoring aggressive pricing tactics that compress margins for global incumbents. Western vendors answer by pivoting toward high-temperature silicon-carbide and AI-enabled packages.

Other drivers and restraints analyzed in the detailed report include:

- Mandatory tyre-pressure monitoring adoption waves in India & ASEAN two-wheelers

- Accelerated rollout of 5G mmWave radios requiring precision thermo-mechanical pressure control

- Fragmented wireless protocol landscape inflating integration cost

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wired devices retained 71.32% revenue in 2025 due to deterministic data delivery in power-rich settings such as engine control units and surgical theaters. However, wireless nodes will outpace with a 12.61% CAGR as factories retrofit to Industry 4.0. Smart Control retrofit kits cut installation expense by 40% while enabling predictive shutdowns for pressure vessels. Power-over-Ethernet upgrades are keeping wired sensors relevant by multiplexing power and data on a single line. Wireless nodes leverage energy harvesting and edge compute, allowing placement on rotating shafts or sealed chambers once considered unreachable.

Absolute designs held 45.58% share in 2025 because manifold pressure, weather logging, and drone altimetry require vacuum-referenced readings. Differential units will see a 10.23% CAGR thanks to HVAC retrofits and filtration monitoring in cleanrooms. Recent wet-etch silicon fabrication pushed sensitivity to 5.07 mV/V/MPa with 0.67% FS linearity. Gauge units remain staple devices in hydraulics but exhibit only mid-single-digit growth.

The Pressure Sensors Market Report is Segmented by Type of Sensor (Wired, Wireless), Product Type (Absolute, Differential, Gauge), Technology (Piezoresistive, Electromagnetic, Optical, Capacitive, Resonant Solid-State, and More), Application (Automotive, Medical, Industrial, Aerospace and Defense, HVAC, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific's 35.62% leadership stems from China's MEMS fabs and India's TPMS mandates. The National Highways expansion and 5,293 EV charging stations catalyze sensor content per vehicle. Local producers are closing the technology gap; Major players notes domestic suppliers are integrating AI into automotive perception stacks. Europe leverages its industrial automation heritage; Infineon's EUR 5 billion Dresden Smart Power Fab underscores strategic semiconductor self-reliance. North America excels in aerospace and medical segments, with DARPA-funded research pushing sensing frontiers. The Middle East & Africa posts the fastest 12.08% CAGR on LNG projects needing subsea instrumentation, complemented by smart-city infrastructure that seeds wireless deployments.

- ABB Ltd

- All Sensors Corporation

- Bosch Sensortec GmbH

- Endress+Hauser AG

- TE Connectivity

- Honeywell International Inc.

- Schneider Electric SE

- Kistler Group

- Rockwell Automation Inc.

- Emerson Electric Co.

- Sensata Technologies Inc.

- Siemens AG

- Yokogawa Electric Corp.

- Infineon Technologies AG

- STMicroelectronics N.V.

- Sensirion AG

- NXP Semiconductors N.V.

- Texas Instruments Inc.

- Omron Corporation

- Murata Manufacturing Co., Ltd.

- Amphenol (S S I Technologies)

- BD Sensors GmbH

- Keller AG fur Druckmesstechnik

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid electrification of xEV power-train control systems driving high-accuracy barometric sensing (Asia)

- 4.2.2 Expansion of smart factory retrofits boosting wireless sensor node demand (Europe and NA)

- 4.2.3 Mandatory tyre-pressure monitoring adoption waves in India and ASEAN two-wheelers

- 4.2.4 Accelerated rollout of 5G mmWave radios requiring precision thermo-mechanical pressure control

- 4.2.5 Adoption of disposable MEMS pressure catheters in outpatient cardiovascular clinics (US)

- 4.2.6 LNG carrier fleet build-up elevating harsh-environment subsea pressure instrumentation (Middle East)

- 4.3 Market Restraints

- 4.3.1 ASP erosion from Chinese white-label MEMS foundries

- 4.3.2 Fragmented wireless protocol landscape inflating integration cost

- 4.3.3 Reliability concerns in optical pressure chips beyond 175 degree C process lines

- 4.3.4 Supply-chain exposure to bulk piezoresistive wafer shortages

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory and Technological Outlook

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Impact of Macro Trends on the Market

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type of Sensor

- 5.1.1 Wired

- 5.1.2 Wireless

- 5.2 By Product Type

- 5.2.1 Absolute

- 5.2.2 Differential

- 5.2.3 Gauge

- 5.3 By Technology

- 5.3.1 Piezoresistive

- 5.3.2 Electromagnetic

- 5.3.3 Capacitive

- 5.3.4 Resonant Solid-State

- 5.3.5 Optical

- 5.3.6 Other Pressure Sensors

- 5.4 By Application

- 5.4.1 Automotive

- 5.4.2 Medical

- 5.4.3 Consumer Electronics

- 5.4.4 Industrial

- 5.4.5 Aerospace and Defense

- 5.4.6 Food and Beverage

- 5.4.7 HVAC

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global- and Market-level Overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 ABB Ltd

- 6.4.2 All Sensors Corporation

- 6.4.3 Bosch Sensortec GmbH

- 6.4.4 Endress+Hauser AG

- 6.4.5 TE Connectivity

- 6.4.6 Honeywell International Inc.

- 6.4.7 Schneider Electric SE

- 6.4.8 Kistler Group

- 6.4.9 Rockwell Automation Inc.

- 6.4.10 Emerson Electric Co.

- 6.4.11 Sensata Technologies Inc.

- 6.4.12 Siemens AG

- 6.4.13 Yokogawa Electric Corp.

- 6.4.14 Infineon Technologies AG

- 6.4.15 STMicroelectronics N.V.

- 6.4.16 Sensirion AG

- 6.4.17 NXP Semiconductors N.V.

- 6.4.18 Texas Instruments Inc.

- 6.4.19 Omron Corporation

- 6.4.20 Murata Manufacturing Co., Ltd.

- 6.4.21 Amphenol (S S I Technologies)

- 6.4.22 BD Sensors GmbH

- 6.4.23 Keller AG fur Druckmesstechnik

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment