PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851329

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851329

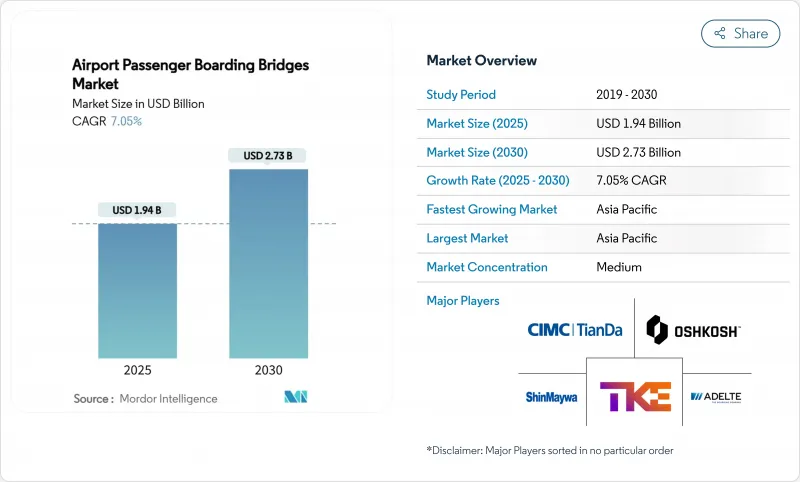

Airport Passenger Boarding Bridges - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The airport passenger boarding bridges market is valued at USD 1.94 billion in 2025 and is forecasted to reach USD 2.73 billion by 2030, reflecting a 7.05% CAGR.

Recovery in global air travel, combined with an unprecedented wave of terminal construction and expansion projects, underpins this acceleration. Asia-Pacific alone has more than USD 488 billion of airport development in the pipeline, and many legacy hubs in North America, Europe, and the Middle East are modernizing gates to meet stringent sustainability mandates. Electro-mechanical bridges that cut energy use and lifetime maintenance costs are steadily displacing hydraulic units. At the same time, airport operators increasingly emphasize passenger-experience features such as natural light and biometric readiness. Competitive dynamics favor manufacturers able to demonstrate life-cycle value, quick installation, and seamless systems integration, as airports increasingly assign procurement weight to total cost of ownership rather than first cost.

Global Airport Passenger Boarding Bridges Market Trends and Insights

Ongoing Airport Capacity Expansion Programs Across Global Hubs

Global hubs inject multi-billion-dollar sums into terminal upgrades to relieve gate bottlenecks and comply with sustainability codes. Schiphol's EUR 6 billion (USD 7.07 billion) five-year capital program focuses heavily on Pier C stand additions requiring new bridges. Munich Airport's EUR 665 million (USD 783.89 million) Terminal 1 pier stretches 360 m and adds multiple new boarding positions. In the United States, FAA-backed megaprojects at John Glenn International, Tampa, and Pittsburgh exceed USD 1 billion and collectively translate into dozens of bridge orders. Asia-Pacific projects such as Long Thanh International in Vietnam and Changi Terminal 5 in Singapore will each deploy several hundred bridges during phased construction. The cadence of these expansions provides sustained, forecastable demand for manufacturers across the airport passenger boarding bridges market.

Surge in International and Domestic Air Passenger Volumes

Passenger throughput rebounded sharply in 2024 and is expected to cross pre-pandemic peaks in 2025 at many hubs, exerting pressure on gate infrastructure. Groupe ADP recorded 363.7 million travellers in 2024, an 8.1% annual jump. Asia-Pacific traffic is projected to hit 2.9 billion by the mid-2030s, nearly tripling today's levels. Airlines now factor guaranteed bridge access into route economics, and some operators charge premium rates for jet-way use, improving payback for new installations. As passenger peaks intensify, airports accelerate bridge procurement to avoid stand conflicts and to shorten turnaround times-direct catalysts for growth in the airport passenger boarding bridges market.

Significant Initial Investment Required for Boarding Bridge Installations

Single bridges cost USD 750,000-1 million, creating budget friction for smaller airports and public-sector owners reliant on constrained capital plans. Arizona's State Aviation System Plan lists USD 8.7 billion of facility needs over 20 years, with passenger boarding bridges a sizeable line item. The result is staggered procurement schedules or reduced scope, especially in cost-sensitive emerging markets, slowing near-term penetration in the airport passenger boarding bridges market.

Other drivers and restraints analyzed in the detailed report include:

- Transition Toward Energy-Efficient Electro-Mechanical Systems

- Growing Integration of Biometric and Automated Boarding Technologies

- High Maintenance Complexity and Total Life-Cycle Cost Burdens

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Movable boarding bridges generated 60.01% of 2024 revenue and are forecast to compound at 8.45% annually. Their ability to align with diverse aircraft-from regional jets to Code F wide-bodies-enables airports to widen gate utilisation without structural overhauls. Fixed bridges, although cheaper, remain suited to gates dedicated to a single aircraft family. Movable variations now integrate automated docking, collision-avoidance radar, and condition-based maintenance tools, further widening the value gap. At Key West International, eight new glass-clad movable bridges costing USD 1 million each opened in April 2025, eliminating ground-level boarding and increasing turnaround predictability.

Bridge manufacturers tailor telescopic ranges up to 36 m and elevation spans exceeding 8 m to cover the majority of global fleets. As a result, the airport passenger boarding bridges market size attributable to movable systems will rise from USD 1.16 billion in 2025 to roughly USD 1.85 billion by 2030, sustaining an outsized contribution to revenue and installed base expansion. Airports in Asia-Pacific and the Middle East, where fleet mix often changes hour-by-hour, assign premium tenders to suppliers that can validate broad aircraft compatibility. With net-zero agendas adding demand for energy-optimised operations, movable units incorporating regenerative drives or on-bridge photovoltaic panels stand to capture an additional share within the airport passenger boarding bridges market.

At the stand level, apron-drive bridges, positioned on rotundas, controlled 41.78% of the 2024 turnover. Their robust steel truss, dual telescoping bodies, and rotunda rotation up to 180 degrees make them the workhorse for large-gate layouts worldwide. Yet Over-the-Wing (OTW) bridges are accelerating at 9.01% CAGR, spurred by regional jet proliferation and stand-constrained projects in Japan and India. OTW units mount behind the wing root, freeing a contiguous stand for baggage and catering vehicles.

Dual-boarding configurations also scale, where A350-1000s, B777-9s, and A380s dominate traffic banks. San Francisco International's dual-level gates enable simultaneous upper- and lower-deck entry, cutting boarding time by almost 40%. Although niche in volume, such specialized models command high ASPs that lift segment revenue. Overall, the airport passenger boarding bridges market continues to diversify its model mix, mapping bridge geometry to fleet planning and terminal flow objectives.

The Airport Passenger Boarding Bridges Market Report is Segmented by Type (Movable and Fixed), Model (Apron-Drive Bridge, Commuter Bridge, Nose-Loader Bridge, Over-The-Wing Bridge, T-Bridge), Technology (Electro-Mechanical and Hydraulic), Structure (Steel-Walled and Glass-Walled), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounts for 31.72% of 2024 revenue and is projected to post the fastest 8.87% CAGR through 2030. China targets more than 270 commercial airports by 2025, and India plans 220 new facilities by 2035, guaranteeing sustained procurement cycles. Vietnam alone expects 30 new airports to serve 653 million passengers by 2030, a scenario that will swell the airport passenger boarding bridges market size on the sub-regional level. Simultaneously, mega-projects like Long Thanh International and Changi Terminal 5 each incorporate bridge counts in the high hundreds, setting scale benchmarks across the market.

North America's outlook pivots on replacement and modernization. The FAA allocated USD 289 million in 2025 Airport Infrastructure Grants to 129 US airports, many earmarked for passenger boarding bridge programs. JFK's USD 4.2 billion Terminal 6 will field 10 gates sized for wide-body aircraft, while Pittsburgh, Tampa, and Boston airports embed bridge enhancement inside multi-billion redevelopment packages. Sustained spend on life-cycle upgrades keeps the region critical to global vendor order books even as greenfield construction slows.

Europe maintains steady demand via renewal and sustainability retrofits. Schiphol's Pier upgrades, Munich's new T1 satellite, and Heathrow's GBP 2.3 billion (USD 3.13 billion) two-year acceleration plan include bridge modernizations to align with net-zero ops. EU regulations on energy performance further channel purchases toward electro-mechanical platforms, deepening unit values within the airport passenger boarding bridges market.

The Middle East is witnessing outsized bridge requirements at giga-projects. Dubai's USD 35 billion Al Maktoum expansion foresees 400 stands equipped with more than 800 bridges, while Saudi Arabia's King Salman International plots a multistage rollout to 120 million passengers by 2030. Zayed International's biometric-ready bridges highlight the region's swift move toward tech-integrated infrastructure. Across Africa, growth is led by Addis Ababa and Nairobi expansions, though volumes remain smaller.

- ADELTE GROUP S.L.

- CIMC Tianda Holdings Co., Ltd.

- Oshkosh Corporation

- ShinMaywa Industries, Ltd.

- HUBNER GmbH & Co. KG

- UBS Airport Systems

- Vataple Group

- PT Bukaka Teknik Utama Tbk

- Aviramp Ltd.

- Dabico Airport Solutions

- TK Airport Solutions S.A.

- ACCESSAIR Systems Inc.

- AviaSafe GmbH

- Jiangsu Tianyi Aviation Industry Co., Ltd.

- J&D McLennan Ltd.

- Mitsubishi Heavy Industries Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ongoing airport capacity expansion initiatives across global hubs

- 4.2.2 Surge in international and domestic air passenger volumes

- 4.2.3 Transition toward energy-efficient electro-mechanical boarding bridge systems

- 4.2.4 Growing integration of PBBs with biometric and automated boarding technologies

- 4.2.5 Net-zero emission targets prompting replacement of legacy PBB infrastructure

- 4.2.6 Rising deployment of wide-body aircraft driving demand for dual-arm bridges

- 4.3 Market Restraints

- 4.3.1 Significant initial investment required for boarding bridge installations

- 4.3.2 High maintenance complexity and total lifecycle cost burdens

- 4.3.3 Supply chain risks associated with specialized hydraulic components

- 4.3.4 Infrastructure limitations due to outdated apron and gate configurations at older terminals

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Movable

- 5.1.2 Fixed

- 5.2 By Model

- 5.2.1 Apron-Drive Bridge

- 5.2.2 Commuter Bridge

- 5.2.3 Nose-Loader Bridge

- 5.2.4 Over-the-Wing Bridge

- 5.2.5 T-Bridge

- 5.3 By Technology

- 5.3.1 Electro-Mechanical

- 5.3.2 Hydraulic

- 5.4 By Structure

- 5.4.1 Steel-Walled

- 5.4.2 Glass-Walled

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 France

- 5.5.2.3 Germany

- 5.5.2.4 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Qatar

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 ADELTE GROUP S.L.

- 6.4.2 CIMC Tianda Holdings Co., Ltd.

- 6.4.3 Oshkosh Corporation

- 6.4.4 ShinMaywa Industries, Ltd.

- 6.4.5 HUBNER GmbH & Co. KG

- 6.4.6 UBS Airport Systems

- 6.4.7 Vataple Group

- 6.4.8 PT Bukaka Teknik Utama Tbk

- 6.4.9 Aviramp Ltd.

- 6.4.10 Dabico Airport Solutions

- 6.4.11 TK Airport Solutions S.A.

- 6.4.12 ACCESSAIR Systems Inc.

- 6.4.13 AviaSafe GmbH

- 6.4.14 Jiangsu Tianyi Aviation Industry Co., Ltd.

- 6.4.15 J&D McLennan Ltd.

- 6.4.16 Mitsubishi Heavy Industries Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment