PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851498

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851498

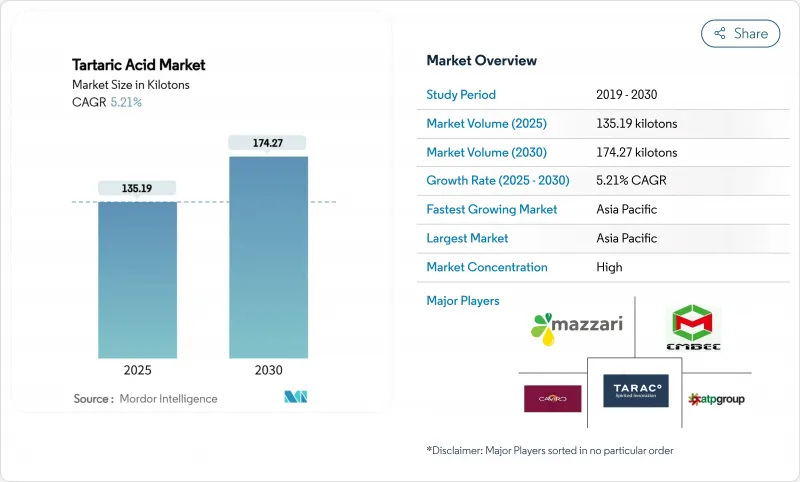

Tartaric Acid - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Tartaric Acid Market size is estimated at 135.19 kilotons in 2025, and is expected to reach 174.27 kilotons by 2030, at a CAGR of 5.21% during the forecast period (2025-2030).

This progression mirrors the compound's broad utility, stretching from wine stabilization to advanced pharmaceutical excipients. Supply resilience anchors the tartaric acid market because producers can toggle between grape-derived recovery and maleic anhydride synthesis, cushioning raw-material shocks. Elevated purity specifications in wine making, rising clean-label food preferences, and steady pharmaceutical formulations are together widening the commercial base. At the same time, sustainability pressures spur investment in electrodialysis and other energy-saving processes that trim production costs for synthetic grades without eroding the quality edge held by natural variants.

Global Tartaric Acid Market Trends and Insights

Growing Demand for Wine Production

Lower global wine output, which fell to 226 million hectoliters in 2024, has paradoxically lifted demand for external tartaric acid supplies as producers rely less on in-house grape waste recovery. Scarcity premiums enable European natural producers to secure 15-20% higher prices over synthetic offerings. Trials in Virginia show that potassium-based tartaric additions before fermentation deliver superior sensory scores versus post-fermentation use. Climate-driven rises in grape potassium further increase routine acidification needs. The International Organisation of Vine and Wine now stipulates 99.5% purity, a threshold favoring established natural suppliers. Producers also valorize distillery vinasses, reaching 69.7% purity via electrodialysis, aligning quality goals with circular-economy mandates.

Rising Pharmaceutical Excipient Demand

The tartaric acid market benefits from the compound's chiral properties that aid drug dissolution, tablet disintegration, and bioavailability. Banana-starch complexes outperform standard super-disintegrants in disintegration time. FDA guidance treats tartaric acid as GRAS, lowering regulatory hurdles. Patent filings for metalloproteinase inhibition and antimicrobial actives underscore therapeutic potential. Growth in laxative formulations accelerates at 6.06% CAGR as aging populations seek gentle natural options. Harmonized daily-intake limits of 240 mg/kg in the United States and European Union streamline global product rollouts.

Regulatory Scrutiny on Synthetic Tartaric Acid Residues

Traceability gaps exposed by the European Parliament spur stricter oversight that raises compliance outlays for Chinese synthetic plants. Heavy-metal limits introduced in EFSA's 2024 opinion require costlier purification. Coupled with isotope testing, regulators can now discern fermentation-derived and petrochemical origins, tightening import inspections.

Other drivers and restraints analyzed in the detailed report include:

- Micro-Encapsulation Adoption in Nutraceuticals

- Shift toward Natural Acidity Regulators in Clean-Label Foods

- Availability of Suitable Substitutes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The natural grade of the tartaric acid market commanded 72.19% share in 2024 on the strength of integrated grape-waste processing. Natural recovery thrives in Europe, where wine producers extract acid as a byproduct, slashing feedstock costs. Synthetic capacity, concentrated in China, is gaining pace at a 5.91% CAGR because maleic anhydride furnishes an agricultural-cycle-free route. Sustainable membrane electrodialysis cuts energy use by 30%, narrowing cost gaps.

Synthetic producers tout uniform purity and year-round availability, attracting buyers focused on predictable specifications. Natural suppliers counterbalance with organic certification advantages and premium positioning in clean-label foods. Alvinesa's acquisitions in Chile and Argentina underpin continuous grape-waste flows across hemispheres. As regulatory bodies favor plant-origin acids in organic labeling, natural volumes are likely to hold majority share even as synthetics gain numerical ground within the tartaric acid market.

The Tartaric Acid Market Report is Segmented by Type (Natural Tartaric Acid, Synthetic Tartaric Acid), Application (Preservative and Additive, Laxative, Intermediate, and Other Applications), End-User Industry (Food and Beverage, Pharmaceutical, Cosmetics, Construction, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa).

Geography Analysis

Asia-Pacific stands at the forefront of the tartaric acid market with 46.52% share in 2024 and a 5.88% CAGR outlook to 2030. China's integrated petrochemical complexes supply competitively priced maleic anhydride, allowing synthetics to undercut European offers by 15-20%. Pharmaceutical production in India and Southeast Asia further bulks demand for high-purity grades. Authorities in Japan, South Korea, and Singapore encourage low-carbon manufacturing, spurring trials in electrochemical synthesis that curb energy use.

Europe upholds a strong position anchored in natural extraction linked to its wine sector. Grape-processing hubs in Italy, Spain, and France enable continuous raw-material access and ensure compliance with the 99.5% purity threshold. EU authentication rules using isotope analysis strengthen domestic suppliers against synthetic imports. Downstream food and beverage brands within Germany and the Nordics value organically certified inputs, bolstering intra-regional flows.

North America forms a mature yet steady slice of the tartaric acid market. The United States drives consumption through generic drug production and clean-label formulations, while Canada emphasizes natural ingredients in ready meals. Mexico's expanding confectionery and beverage exports add incremental demand. USDA organic standards, which mandate plant-derived acids, direct buyers toward grape-waste processors. Regional research fosters innovations such as bee-mite biocontrol, hinting at fresh avenues for volume diversification.

- Alvinesa Natural Ingredients

- Anhui Hailan Bio-technology Co., Ltd

- ATPGroup

- Australian Tartaric Products

- Caviro

- Changmao Biochemical Engineering Company Limited

- Distillerie Mazzari S.p.A

- Fuso Chemical Co., Ltd.

- Giovanni Randi SpA

- Industria Chimica Valenzana I.C.V. SpA

- Merck KGaA

- Ningbo Jinzhan Biotechnology Co., Ltd.

- Tartaros Gonzalo Castello S.L.

- The Greatwall Bi0-Chemical Engineering Co., Ltd.

- The Tartaric Chemicals Corporation

- Vinicas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Wine Production

- 4.2.2 Rising Pharmaceutical Excipient Demand

- 4.2.3 Micro-Encapsulation Adoption in Nutraceuticals

- 4.2.4 Shift toward Natural Acidity Regulators in Clean-Label Foods

- 4.2.5 Emerging Use in Bee-Mite Biocontrol Formulations

- 4.3 Market Restraints

- 4.3.1 Regulatory Scrutiny on Synthetic Tartaric Acid Residues

- 4.3.2 Availability of Suitable Substitutes

- 4.3.3 Price Pressure from Alternative Organic Acids

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Natural Tartaric Acid

- 5.1.2 Synthetic Tartaric Acid

- 5.2 By Application

- 5.2.1 Preservative and Additive

- 5.2.2 Laxative

- 5.2.3 Intermediate

- 5.2.4 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Food and Beverage

- 5.3.2 Pharmaceutical

- 5.3.3 Cosmetics

- 5.3.4 Construction

- 5.3.5 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Thailand

- 5.4.1.6 Indonesia

- 5.4.1.7 Vietnam

- 5.4.1.8 Malaysia

- 5.4.1.9 Philippines

- 5.4.1.10 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 NORDIC Countries

- 5.4.3.8 Turkey

- 5.4.3.9 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 United Arab Emirates

- 5.4.5.3 Qatar

- 5.4.5.4 South Africa

- 5.4.5.5 Nigeria

- 5.4.5.6 Egypt

- 5.4.5.7 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Alvinesa Natural Ingredients

- 6.4.2 Anhui Hailan Bio-technology Co., Ltd

- 6.4.3 ATPGroup

- 6.4.4 Australian Tartaric Products

- 6.4.5 Caviro

- 6.4.6 Changmao Biochemical Engineering Company Limited

- 6.4.7 Distillerie Mazzari S.p.A

- 6.4.8 Fuso Chemical Co., Ltd.

- 6.4.9 Giovanni Randi SpA

- 6.4.10 Industria Chimica Valenzana I.C.V. SpA

- 6.4.11 Merck KGaA

- 6.4.12 Ningbo Jinzhan Biotechnology Co., Ltd.

- 6.4.13 Tartaros Gonzalo Castello S.L.

- 6.4.14 The Greatwall Bi0-Chemical Engineering Co., Ltd.

- 6.4.15 The Tartaric Chemicals Corporation

- 6.4.16 Vinicas

7 Market Opportunities and Future Outlook

- 7.1 White-space and unmet-need assessment

- 7.2 Adoption in niche applications (biocontrol, advanced materials)