PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851521

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851521

Internet Of Things In Energy - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

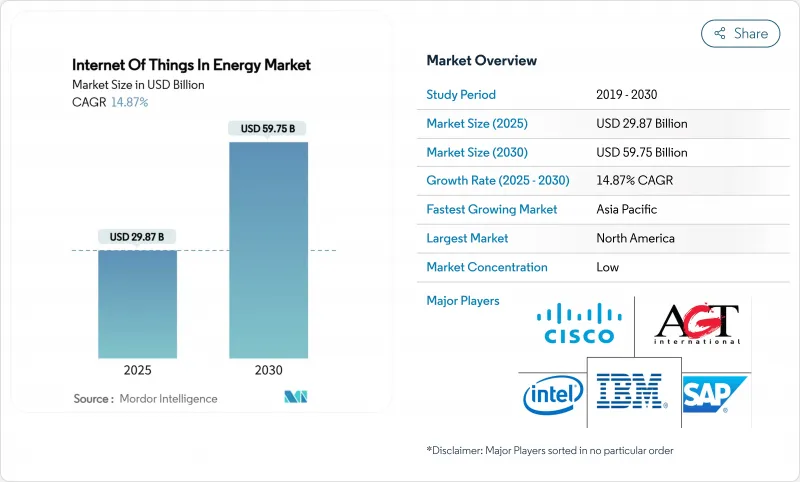

The Internet of Things in the energy market stood at USD 29.87 billion in 2025 and is on course to reach USD 59.75 billion by 2030, reflecting a 14.87% CAGR.

Utilities across major economies are moving from centralized command-and-control to distributed intelligence so that real-time grid optimization, predictive asset care, and autonomous energy trading can co-exist. Capital spending on smart meters, intelligent substation retrofits, and edge analytics stacks has risen because these investments cut outage minutes and lower maintenance budgets. Semiconductor pricing has stabilized, allowing low-power wide-area modules to fall below the USD 3 threshold, which brings connectivity to secondary feeders, rural solar farms, and behind-the-meter devices. Cellular operators, satellite fleets, and private 5G providers are converging on hybrid network offers that guarantee deterministic latency for protection relay messages while squeezing bandwidth costs for simple sensor traffic. Software vendors have responded by embedding AI toolkits inside asset performance platforms so that energy firms can predict component failures early and monetize flexibility services in wholesale markets.

Global Internet Of Things In Energy Market Trends and Insights

Utility Smart-Meter Roll-Outs and Grid-Modernization Mandates

Mandated advanced metering infrastructure has moved beyond the pilot stage as regulators demand visibility of low-voltage networks and demand response outcomes. Honeywell and Verizon now embed native 5G radios into meters, enabling remote firmware updates, self-healing mesh communication, and autonomous service disconnects. Norway completed nationwide roll-outs yet only 29.5% of households checked live consumption data, underscoring that consumer engagement and intuitive apps decide whether hard savings materialize. Utilities therefore pair technical deployment with customer education, gamified dashboards, and tariff incentives. Advanced meters feed granular interval data to distribution management systems so that rooftop solar back-feed and electric vehicle (EV) clustering can be forecast and balanced without over-building capacity.

Falling 5G/LPWAN Module Cost

Chip supply normalization pushed narrow-band IoT module prices down by 28% between 2023 and 2025, removing a key cost barrier for high-volume sensor roll-outs. Laboratory tests show LTE-M offers higher throughput and lower energy consumption than many alternative low-power protocols, which is important where battery swaps are costly. Semiconductor makers are redesigning micro-controllers with integrated AI acceleration so that anomaly detection can occur at the edge. Research teams have proved that turning LoRa gateways into lightweight compute nodes trims backhaul traffic by 70% without breaking legacy payload formats. Energy firms now equip remote wind farms, rural substations, and valve arrays with these modules, placing asset intelligence where trucks rarely visit.

Cyber-Security and OT/IT Convergence Risk

As operational equipment becomes routable on public networks, attack surfaces multiply. The EU Cyber Resilience Act will come into force in August 2025, obliging device makers to document software components and issue timely patches. Many substations still run legacy protocols that lack authentication, and intrusion studies show malware can pivot from billing servers to breaker controls in minutes if segmentation is weak. Over-the-air update pipelines, hardware root-of-trust, and zero-trust segmentation are becoming mandatory across new procurement frameworks. Effective governance hinges on closer collaboration between information-technology and operational-technology teams.

Other drivers and restraints analyzed in the detailed report include:

- Distributed-Renewable Orchestration Needs

- AI-Driven Predictive-Maintenance ROI Cases

- Legacy-SCADA Interoperability Gap

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Smart meters, intelligent sensors, gateways, and edge controllers collectively secured 41% of the Internet of Things in the energy market share in 2024. The hardware wave anchors utility digital twins and pushes granular field data into analytics clouds. Security hardware modules and trusted execution environments gain notice because regulators now ask vendors to prove device integrity from chip to cloud. IoT security platforms are forecast to compound at 17.89% through 2030, twice the system average, as the cost of a single operational breach can erase multi-year efficiency savings. Edge servers built on ruggedised ARM or x86 boards are shipping with AI accelerators that handle fault detection in milliseconds. Toshiba recently unveiled a key-management chipset that signs firmware blobs before they touch the field device, trimming audit times for compliance reviewers.

Software and services follow hardware's beachhead. Utilities are paying for full-stack offerings where the vendor bundles devices, connectivity, and a subscription dashboard. Managed service contracts appeal in regions short of data-science talent because they shift integration risk to the supplier. As a result, services revenue is taking a larger slice of the expanding Internet of Things in the energy market. Meanwhile, component suppliers are moving manufacturing closer to demand centres to buffer any geopolitical shock to semiconductor flows.

Real-time distribution grid monitoring accounted for 38.5% of 2024 revenue thanks to programs that instrument transformers, feeders, and voltage regulators. AI overlays adapt set-points on the fly so that networks avoid over-voltage when rooftop solar spikes midday. Connected EV infrastructure shows the fastest 15.35% CAGR because chargers double as both load and storage assets. Utilities view them as flexible nodes that can supply reactive power and soak up midday excess. Governments are subsidising bidirectional chargers and demanding open-protocol telemetry, which funnels more devices into the Internet of Things in the energy market.

Predictive maintenance sits close behind as renewable owners chase higher capacity factors. Offshore wind farms now integrate software-defined networking rings that maintain deterministic links to nacelle sensors despite harsh marine environments. Demand-response programs inside commercial buildings have trimmed peak kW draw by up to 86% during critical intervals. Industrial users deploy edge analytics to lower electricity per unit of output, a metric that directly feeds ESG scorecards and investor screens.

The Internet of Things in the Energy Market Report is Segmented by Component (Hardware, Software and Analytics, Iot Platforms, and More), Application (Smart Grid Monitoring, Energy Management Systems, Predictive Maintenance, and More), Connectivity Technology (Cellular (2G-5G), Satellite IoT, and More), Deployment Model (Cloud, Edge, and More), End-User (Electric and Gas Utilities, Residential and Prosumer, and More), and Geography

Geography Analysis

North America commanded 38% of 2024 revenue for the Internet of Things in the energy market. Federal investment in grid resilience, state-level clean-energy standards, and a mature cellular footprint enable rapid adoption. Schneider Electric warns that data-centre load is climbing faster than substation build-outs, forcing utilities to deploy IoT sensors to squeeze every amp from existing lines. Canada's remote microgrids are early satellite IoT adopters because fibre drops are expensive in permafrost. Mexico's energy reform is attracting distributed solar investors who demand predictive analytics from day one.

Asia Pacific is the fastest-growing region at a 17% CAGR through 2030. Japan's super-solar project targets 20 GW by 2030 using perovskite cells with a theoretical efficiency beyond 30%. China's smart-grid rollout under the 14th Five-Year Plan includes multi-energy microgrids and 5G base stations embedded in transmission pylons. India's renewables push blends IoT sensors with government-subsidised cloud hosting, while South Korean industrial parks equip factories with AI edge boxes to shave power peaks.

Europe shows steady expansion on the back of stringent carbon laws and cross-border balancing markets. The EU Cyber Resilience Act hard-codes security spending into every IoT budget. Germany's Industry 4.0 initiatives mean factories integrate power-quality meters with production scheduling so that watt-hours per unit become a KPI as important as takt time. The United Kingdom's public-sector energy efficiency program has already logged double-digit savings after building managers gained minute-level insights. France upgrades nuclear station cooling pumps with vibration sensors to extend operating licenses, and Nordic grid operators test market platforms for real-time flexibility. The Middle East and Africa are earlier in the curve but mega solar-and-storage projects linked to green-hydrogen plants guarantee future demand.

- Cisco Systems

- IBM Corporation

- Siemens AG

- Schneider Electric

- Huawei Technologies

- Intel Corporation

- SAP SE

- Oracle Corporation

- AGT International

- Davra Networks

- Flutura Business Solutions

- Wind River Systems

- Silver Spring Networks

- Verizon Business

- Vodafone IoT

- GE Digital

- Emerson Electric

- Siemens Gamesa (renewable IoT)

- Landis+Gyr

- Kamstrup

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Utility smart-meter roll-outs and grid-modernization mandates

- 4.2.2 Falling 5G/LPWAN module costs

- 4.2.3 Distributed-renewable orchestration needs

- 4.2.4 AI-driven predictive-maintenance ROI cases

- 4.2.5 Flexibility monetisation (V2G, P2P energy)

- 4.2.6 Carbon-accounting data regulations

- 4.3 Market Restraints

- 4.3.1 Cyber-security and OT/IT convergence risk

- 4.3.2 Legacy-SCADA interoperability gaps

- 4.3.3 Edge-compute talent scarcity

- 4.3.4 Semiconductor-supply volatility

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Smart Thermostats

- 5.1.1.2 Smart Meters

- 5.1.1.3 EV Charging Stations

- 5.1.1.4 Other Hardware

- 5.1.2 Software and Analytics

- 5.1.3 IoT Platforms

- 5.1.4 IoT Security

- 5.1.5 IoT Services

- 5.1.1 Hardware

- 5.2 By Application

- 5.2.1 Smart Grid Monitoring

- 5.2.2 Energy Management Systems

- 5.2.3 Predictive Maintenance

- 5.2.4 Connected EV Infrastructure

- 5.2.5 Distributed-Renewable Integration

- 5.2.6 Demand Response and Flexibility

- 5.3 By Connectivity Technology

- 5.3.1 Cellular (2G-5G)

- 5.3.2 LPWAN (NB-IoT, LoRaWAN, Sigfox)

- 5.3.3 Satellite IoT

- 5.3.4 Wi-Fi/BLE

- 5.3.5 PLC and Other

- 5.4 By Deployment Model

- 5.4.1 Cloud

- 5.4.2 Edge

- 5.4.3 On-premise

- 5.5 By End-user

- 5.5.1 Electric and Gas Utilities

- 5.5.2 Oil and Gas Up/Mid/Down-stream

- 5.5.3 Commercial and Industrial Facilities

- 5.5.4 Residential and Prosumer

- 5.5.5 Renewable Power Plants

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 Turkey

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Cisco Systems

- 6.4.2 IBM Corporation

- 6.4.3 Siemens AG

- 6.4.4 Schneider Electric

- 6.4.5 Huawei Technologies

- 6.4.6 Intel Corporation

- 6.4.7 SAP SE

- 6.4.8 Oracle Corporation

- 6.4.9 AGT International

- 6.4.10 Davra Networks

- 6.4.11 Flutura Business Solutions

- 6.4.12 Wind River Systems

- 6.4.13 Silver Spring Networks

- 6.4.14 Verizon Business

- 6.4.15 Vodafone IoT

- 6.4.16 GE Digital

- 6.4.17 Emerson Electric

- 6.4.18 Siemens Gamesa (renewable IoT)

- 6.4.19 Landis+Gyr

- 6.4.20 Kamstrup

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment