PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851576

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851576

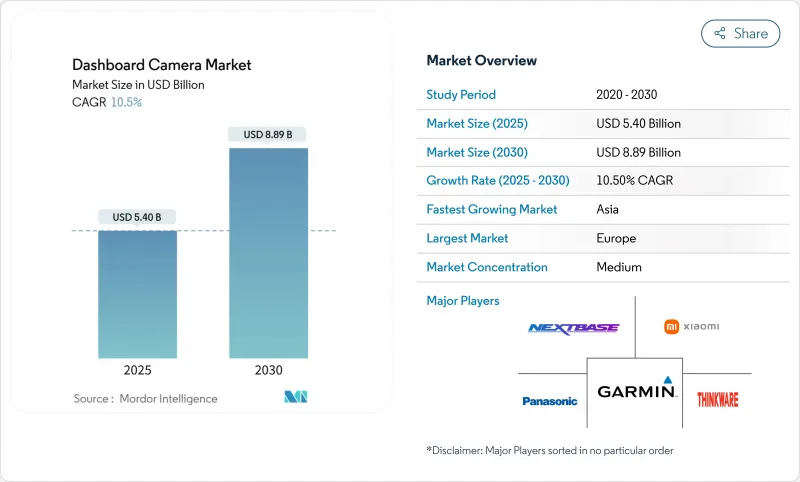

Dashboard Camera - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The dashboard camera market size is valued at USD 5.40 billion in 2025 and is forecast to reach USD 8.89 billion by 2030, reflecting a 10.50% CAGR.

This expansion stems from compulsory in-vehicle data recorders in Europe, expanding insurance telematics programs in North America, and rapid AI integration that raises perceived value among fleet operators. Europe's firm regulatory stance has positioned factory-fit units as the new norm, while Asia's thriving automotive production base and telematics-friendly insurers underpin the fastest regional growth momentum. Technological differentiation has pivoted from hardware to software; cloud-connected analytics, GDPR-compliant storage, and heat-resistant designs now determine brand preference. Competition is intensifying as aftermarket specialists, fleet telematics vendors, and OEMs converge on the same connected-video opportunity, prompting new partnerships and white-label supply models.

Global Dashboard Camera Market Trends and Insights

European eCall-Event Data Recorder mandate driving factory-fit dashcams

The July 2024 regulation obliges every new passenger vehicle in the EU to store crash-related data, making video capture a logical extension that OEMs are embedding at the production line . Manufacturers gain a compliance differentiator, suppliers secure long-term platform volume, and aftermarket brands must pivot toward dealer accessories and fleet retrofits. German Tier-1 electronics firms have moved quickly with GDPR-ready firmware and encrypted storage, giving them an edge as global platforms export EU-validated technology to other markets.

AI-enabled fleet video telematics adoption in US and UK logistics

Large carriers have transitioned from incident review to predictive coaching. AI analytics automatically flag tail-gating, distraction, or fatigue, enabling safety managers to intervene early, cut claims, and negotiate lower premiums . Scalable cloud review reduces manual footage trawling and makes enterprise deployments feasible across thousands of tractors and vans. Vendors that own proprietary computer-vision stacks now command strategic partnerships with telematics integrators eager for video-first differentiation.

GDPR-driven recording restrictions in Germany and Austria

Loop recording, anonymization, and minimal retention periods are compulsory, raising firmware complexity and cost. The Austrian traffic authority enforces fines up to EUR 20 million (USD 21.8 million) for non-compliance. Legal clarity improved after Germany's Federal Court allowed dashcam evidence in lawsuits, but hardware vendors still need region-specific SKUs, eroding economies of scale.

Other drivers and restraints analyzed in the detailed report include:

- OEM-installed dashcams by global automakers accelerating APAC uptake

- Insurance telematics discounts in Canada and selected APAC markets

- Heat-induced device failures in Middle East markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Basic dashcam technology retained the largest 58% market share in 2024, while smart/AI-integrated units register the fastest 12.2% CAGR through 2030. Smart models convert video into coaching alerts, helping fleets cut claims and negotiate lower premiums. Personal users still buy basic units for cost-effective evidence, yet upscale buyers increasingly choose app-linked devices with cloud uploads. Suppliers that control computer-vision IP secure recurring subscription revenue, buffering hardware commoditization within the dashboard camera market.

Concurrently, insurers cite AI-generated risk profiles when negotiating premiums, reinforcing demand from both carriers and self-insured corporates. Personal vehicle owners remain price-focused, yet upscale buyers gravitate to app-enhanced devices offering emergency upload and remote-viewing peace of mind. As over-the-air updates become commonplace, firmware road-maps rather than optics will anchor brand stickiness within the dashboard camera market.

Single-channel designs led with 72% revenue share in 2024, but dual-channel systems are growing at an 11.1% CAGR on the strength of fleet demand for forward-plus-cabin evidence. Logistics firms report 30% faster dispute resolution when interior footage is available, validating higher capital spend. Ride-hailing drivers and parents form a niche retail audience for multi-view kits, whereas OEMs integrate existing park-assist sensors to trigger selective cabin recording, merging privacy compliance with expanded coverage.

Consumer adoption of rear-plus-cabin views is slower; installation complexity and privacy hesitancy dampen uptake. Nonetheless, ride-hailing drivers and parents are niche segments willing to pay for 360° coverage. OEMs are experimenting with leveraging existing park-assist sensors to trigger selective interior recording, blending safety with privacy compliance.

The Dashboard Camera Market Report is Segmented by Technology (Basic, Advanced, Smart/AI-Integrated), Product Type (Single-Channel, Dual-Channel, Rear-View/Surround), Video Quality (SD and HD, Full-HD, 4K/UHD), Application (Personal Vehicles, Commercial Fleets), Distribution Channel (In-Store, and Online), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe led with 35% share in 2024, anchored by the eCall-Event Data Recorder mandate that institutionalized video evidence. Northern markets exhibit above-average attach rates as insurers embrace footage for claims triage. Privacy safeguards such as automatic face blurring are now baseline specifications, adding development complexity yet raising consumer trust.

Asia posts the fastest 11.6% CAGR to 2030. China benefits from scale manufacturing economies and municipal smart-city grants that endorse connected cameras. South Korea's insurers offer structured telematics credits, accelerating household adoption. India's 2026 commercial ADAS requirement positions the country as a major demand catalyst; localized suppliers already pilot rugged units tuned for monsoon humidity under guidelines from the Ministry of Road Transport and Highways.

North America shows robust fleet momentum. Carriers integrate video with existing ELD and route-optimization stacks, while progressive insurers and risk-management pools endorse camera evidence to curb litigation costs. Extreme-heat regions of the Southwest, alongside Middle-Eastern and African climates, remain constrained by hardware reliability issues; vendors investing in thermal-resistant designs stand to unlock latent potential as validated field data emerges.

- Garmin Ltd.

- Nextbase

- Thinkware Corporation

- Cobra Electronics (Cedar Electronics)

- Pittasoft Co. Ltd. (BlackVue)

- Xiaomi Corp.

- DOD Tech

- HP Inc.

- Lukas (Qronetek)

- Kenwood Corp. (JVC Kenwood)

- Philips N.V. (Dashcam Line)

- Steelmate Automotive

- Papago Inc.

- RoadHawk UK

- AsusTek Computer Inc.

- Vantrue

- Viofo Ltd.

- Panasonic Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 European eCall-Event Data Recorder Mandate Driving Factory-Fit Dashcams

- 4.2.2 AI-Enabled Fleet Video Telematics Adoption in US and UK Logistics

- 4.2.3 OEM-Installed Dashcams by Tesla, BMW and Hyundai Accelerating APAC Uptake

- 4.2.4 Insurance Telematics Discounts in Canada and South Korea

- 4.2.5 Government Commercial Fleet Video Evidence Regulation (e.g. India 2026 Regulation)

- 4.2.6 Insurer-driven 4K/UHD video-quality adoption for claim clarity

- 4.3 Market Restraints

- 4.3.1 GDPR-Driven Recording Restrictions in Germany and Austria

- 4.3.2 Cyber-Vulnerability Disclosures in Connected Dashcams

- 4.3.3 Heat-Induced Device Failures (e.g., Middle-East (>15 % RMA))

- 4.3.4 Installation complexity and privacy hesitancy for dual/in-cabin cameras

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Technology

- 5.1.1 Basic

- 5.1.2 Advanced

- 5.1.3 Smart / AI-Integrated

- 5.2 By Product Type

- 5.2.1 Single-Channel

- 5.2.2 Dual-Channel

- 5.2.3 Rear-View/Surround

- 5.3 By Video Quality

- 5.3.1 SD and HD

- 5.3.2 Full-HD

- 5.3.3 4K / UHD

- 5.4 By Application

- 5.4.1 Personal Vehicles

- 5.4.2 Commercial Fleets

- 5.5 By Distribution Channel

- 5.5.1 In-store

- 5.5.2 Online

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Nordics (Sweden, Norway, Denmark, Finland)

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 ASEAN (Indonesia, Thailand, Malaysia, Vietnam, Philippines)

- 5.6.4.6 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Turkey

- 5.6.5.1.4 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Garmin Ltd.

- 6.4.2 Nextbase

- 6.4.3 Thinkware Corporation

- 6.4.4 Cobra Electronics (Cedar Electronics)

- 6.4.5 Pittasoft Co. Ltd. (BlackVue)

- 6.4.6 Xiaomi Corp.

- 6.4.7 DOD Tech

- 6.4.8 HP Inc.

- 6.4.9 Lukas (Qronetek)

- 6.4.10 Kenwood Corp. (JVC Kenwood)

- 6.4.11 Philips N.V. (Dashcam Line)

- 6.4.12 Steelmate Automotive

- 6.4.13 Papago Inc.

- 6.4.14 RoadHawk UK

- 6.4.15 AsusTek Computer Inc.

- 6.4.16 Vantrue

- 6.4.17 Viofo Ltd.

- 6.4.18 Panasonic Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment