PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851585

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851585

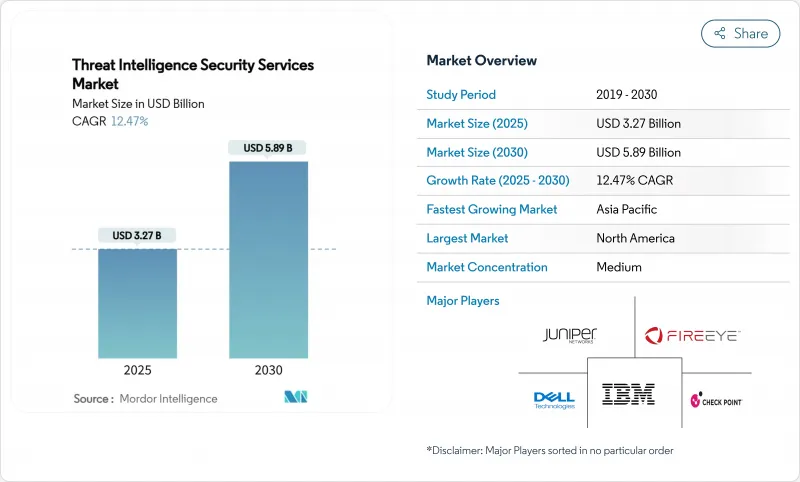

Threat Intelligence Security Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The threat intelligence security services market size stands at USD 3.27 billion in 2025 and is forecast to reach USD 5.89 billion by 2030, advancing at a 12.47% CAGR over the period.

The expansion reflects a decisive shift from reactive perimeter defense toward continuous threat hunting, exposure management, and predictive analytics. Escalating state-sponsored campaigns, a 65% rise in cloud security incidents, and mandatory breach-notification laws across major jurisdictions are amplifying demand for real-time, contextual threat data. Platform convergence, led by zero-trust and Extended Detection and Response (XDR) rollouts, is further accelerating investment as security teams seek unified visibility and automated response. At the same time, the proliferation of application programming interface attack surfaces and insider risks arising from generative AI code assistants have prompted organizations to reassess risk postures, energizing the threat intelligence security services market.

Global Threat Intelligence Security Services Market Trends and Insights

Rapid Escalation in State-Sponsored APT Campaigns

Nation-state groups such as Volt Typhoon and Salt Typhoon have intensified operations against critical infrastructure, prompting organizations to prioritize tactical intelligence and pre-incident attribution capabilities. The Cybersecurity and Infrastructure Security Agency issued 3,368 pre-ransomware notifications in 2024, underscoring the volume of advanced intrusion attempts. Attacks now go beyond espionage to include destructive pre-positioning, which demands continuous monitoring and specialized hunting. Iranian actors are simultaneously targeting healthcare and financial services, turning threat intelligence into a strategic imperative across sectors. These developments have accelerated spending on managed detection, enriched malware analysis, and contextual attribution services.

Proliferation of Cloud Workloads & API Attack-Surface

Cloud migration has multiplied attack entry points, with organizations operating thousands of APIs across multi-cloud settings. API failures contributed to a majority of cloud breaches reported in 2024, revealing visibility gaps in east-west traffic. Traditional network monitoring lacks context for ephemeral workloads, fuelling adoption of cloud-native threat intelligence that can map dependencies in real time. Microservices architectures further complicate asset inventories, increasing reliance on automated discovery and continuous risk scoring. The outcome is sustained momentum for cloud-delivered analytics engines and exposure management modules tailored to serverless and container environments.

Shortage of Tier-1 Threat-Hunters & Analysts

Demand for deep forensics and malware reverse-engineering outpaces supply. Years of training are needed to master nation-state adversary tactics, yet security teams face attrition and wage inflation. The gap is driving consolidation as smaller vendors struggle to retain experts, and clients turn to Managed Detection and Response for turnkey coverage. Providers must now automate routine triage to free scarce specialists for higher-value pursuits, heightening interest in AI-assisted analysis modules.

Other drivers and restraints analyzed in the detailed report include:

- Zero-Trust & XDR Platformisation by CISOs

- Mandatory Breach-Notification Laws

- Budget Compression in SME Segment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment already commands 58% of the threat intelligence security services market share. The segment is projected to expand at an 18.20% CAGR through 2030, reinforcing the centrality of cloud-native analytics engines. Elastic compute and distributed storage enable providers to process petabytes of telemetry without customer-side hardware, which is critical as threat intelligence security services market size grows to USD 5.89 billion in 2030. On-premises deployments persist in sovereign cloud and defense contexts that require local data processing, although development roadmaps now prioritize hybrid connectors rather than standalone appliances.

Hybrid adoption is rising among regulated firms that embrace the cloud for scale yet retain select data sets in country for compliance. API-centric attack vectors accentuate cloud resonance since traditional sensors lack context for container traffic. Palo Alto Networks reported AI-centric Annual Recurring Revenue above USD 200 million with 4x year-over-year growth, validating appetite for cloud-delivered machine learning modules. Cloud superiority is therefore entrenched, but vendors must address latency, encryption, and locality factors to accelerate further penetration.

Managed Detection and Response own 56% of the threat intelligence security services market share as of 2024 and are forecast to grow 18.55% annually. Enterprises favour MDR because it fuses technology, telemetry, and human expertise, reducing mean time to detect without staffing burdens. The surge in MDR contracts underlines how the threat intelligence security services market pivots toward outcome-based delivery. Professional services remain vital for maturity assessments, framework design, and Continuous Threat Exposure Management rollouts.

Subscription feeds form a commodity base but are evolving toward context-rich packages with actor profiling and risk scoring. Fortinet posted Security Operations ARR of USD 434.5 million in Q1 2025, up 30.3% year on year, signalling that integrated MDR plus orchestration gains momentum. Vendors blending curated telemetry with automated containment workflows are building defensible differentiation as tool consolidation continues.

Threat Intelligence Security Services Market Segmented by Deployment Mode (Cloud, On-Premises), Service Type (Managed Detection & Response, Professional/Consulting and More), Organization Size (Large Enterprises, Small & Medium Enterprises), End-User Industry (Banking & Financial Services, Healthcare and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America controls 38% of global revenue, supported by the United States' USD 27.5 billion cybersecurity allocation for 2025, which includes USD 3 billion for CISA grants that expand intelligence sharing networks. High adoption of zero-trust, robust venture funding, and an ecosystem of cloud-native vendors sustain regional leadership. Federal Executive Order 14028 compels government agencies to integrate threat intelligence into security operations, and adjacent industries replicate the model for supply-chain assurance. Canada is harmonizing with U.S. disclosure norms, while Mexico's financial regulator extends incident reporting to fintech, adding new demand vectors.

Asia-Pacific is projected to grow at an 18.90% CAGR, the fastest worldwide. China's cybersecurity market is on track to reach USD 23.66 billion by 2029 as government programs enforce in-country security controls. Japan's strategic documents call for tripling domestic cybersecurity sales and boosting national budgets by 50%, which elevates appetite for industry-grade threat intelligence. India continues rapid digitization; its CERT-IN directives oblige real-time reporting for specified incidents, driving service uptake. Australia's AUD 586 million cyber resilience package underpins managed intelligence demand, and regional telecom providers are investing in cross-border telemetry exchanges.

Europe maintains steady growth propelled by the NIS2 directive and local data protection mandates. Germany expects cybersecurity spending beyond €10 billion in 2025 to shield industrial automation from sabotage. The United Kingdom earmarked an extra £600 million for intelligence agencies and plans to devote 5% of GDP to national security by 2035 reinforce long-term visibility for vendors. Data-sovereignty requirements stimulate growth of regional security operations centers capable of processing telemetry within national borders. Providers offering residency-aware cloud fabrics and multilingual analyst support are therefore preferred.

- Google LLC (Mandiant)

- Recorded Future Inc.

- CrowdStrike Holdings Inc.

- Fortinet Inc.

- Cisco Systems Inc.

- International Business Machines Corporation

- Palo Alto Networks Inc.

- Dell Technologies Inc.

- Check Point Software Technologies Ltd.

- Trellix LLC (McAfee Enterprise)

- Broadcom Inc. (Symantec)

- LogRhythm Inc.

- Juniper Networks Inc.

- F-Secure Corporation

- LookingGlass Cyber Solutions Inc.

- Rapid7 Inc.

- Arctic Wolf Networks Inc.

- Trend Micro Incorporated

- Elastic N.V. (Security)

- Kaspersky Lab JSC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid escalation in state-sponsored APT campaigns

- 4.2.2 Proliferation of cloud workloads and API attack-surface

- 4.2.3 Zero-trust and XDR platformisation by CISOs

- 4.2.4 Mandatory breach-notification laws (US, EU, APAC)

- 4.2.5 Insider-risk from Gen-AI code-assistants (under-radar)

- 4.2.6 Adoption of CTEM* for continuous controls validation (under-radar)

- 4.3 Market Restraints

- 4.3.1 Shortage of Tier-1 threat-hunters and analysts

- 4.3.2 Budget compression in SME segment

- 4.3.3 Data-sovereignty barriers to cross-border telemetry sharing (under-radar)

- 4.3.4 Adversary abuse of spoofed TI feeds causing alert fatigue (under-radar)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud

- 5.1.2 On-premise

- 5.2 By Service Type

- 5.2.1 Managed Detection and Response

- 5.2.2 Professional / Consulting

- 5.2.3 Subscription Data-feeds

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-user Industry

- 5.4.1 Banking and Financial Services

- 5.4.2 Healthcare

- 5.4.3 IT and Telecom

- 5.4.4 Retail and e-Commerce

- 5.4.5 Life Sciences / Pharma

- 5.4.6 Government and Defense

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 Middle East

- 5.5.4.1 Israel

- 5.5.4.2 Saudi Arabia

- 5.5.4.3 United Arab Emirates

- 5.5.4.4 Turkey

- 5.5.4.5 Rest of Middle East

- 5.5.5 Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Egypt

- 5.5.5.3 Rest of Africa

- 5.5.6 South America

- 5.5.6.1 Brazil

- 5.5.6.2 Argentina

- 5.5.6.3 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Google LLC (Mandiant)

- 6.4.2 Recorded Future Inc.

- 6.4.3 CrowdStrike Holdings Inc.

- 6.4.4 Fortinet Inc.

- 6.4.5 Cisco Systems Inc.

- 6.4.6 International Business Machines Corporation

- 6.4.7 Palo Alto Networks Inc.

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Check Point Software Technologies Ltd.

- 6.4.10 Trellix LLC (McAfee Enterprise)

- 6.4.11 Broadcom Inc. (Symantec)

- 6.4.12 LogRhythm Inc.

- 6.4.13 Juniper Networks Inc.

- 6.4.14 F-Secure Corporation

- 6.4.15 LookingGlass Cyber Solutions Inc.

- 6.4.16 Rapid7 Inc.

- 6.4.17 Arctic Wolf Networks Inc.

- 6.4.18 Trend Micro Incorporated

- 6.4.19 Elastic N.V. (Security)

- 6.4.20 Kaspersky Lab JSC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment