PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851593

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 1851593

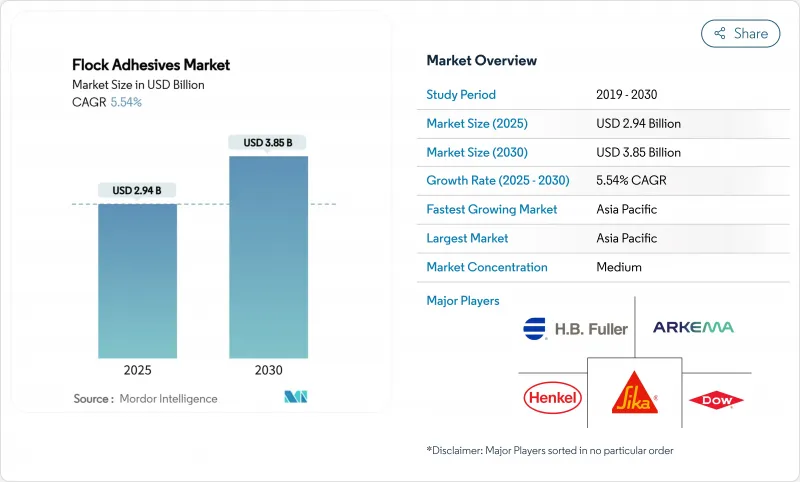

Flock Adhesives - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The Flock Adhesives Market size is estimated at USD 2.94 billion in 2025, and is expected to reach USD 3.85 billion by 2030, at a CAGR of 5.54% during the forecast period (2025-2030).

Growth is anchored in automotive interior demand, accelerated by rising electric-vehicle (EV) production, and reinforced by premium packaging requirements that emphasize soft-touch aesthetics and thermal functionality. Regulatory shifts toward water-based and VOC-free chemistries are prompting rapid product reformulation, especially as the European Union restricts diisocyanates and China tightens interior-emission limits. Automotive applications command the largest slice of the flock adhesives market at 42.56% in 2024 and also expand the fastest at 6.42% CAGR, underscoring the segment's dual role as volume base and innovation engine. Asia-Pacific retains geographic leadership with 51.84% share in 2024 and a 6.19% CAGR outlook through 2030, benefiting from concentrated automotive manufacturing footprints and expanding EV battery capacity. Meanwhile, polyurethane resin systems dominate with 38.19% share, yet "other" chemistries display the strongest 6.65% CAGR as formulators pivot toward acrylic, epoxy and non-isocyanate alternatives to stay ahead of incoming regulation.

Global Flock Adhesives Market Trends and Insights

Surging Demand for Coated Fabrics and Luxury Finish Products

Automotive and luxury-goods producers are stepping up use of flocked materials to signal elevated quality. Cabin parts such as dashboards, pillars and storage trays gain a plush feel that improves grip and cuts rattling noise. Premium packaging makers adopt the same technology so that jewelry boxes or smartphone cases feel exclusive from first touch. The tactile upgrade supports higher retail prices and strengthens brand differentiation. Together these factors translate into a wider, more stable demand base for flock adhesives.

Lightweight, Low-Carbon Vehicle Interior Parts Push Adoption

Car makers are substituting heavy fasteners with adhesive-bonded composite panels to shave grams from every model. Flock adhesives secure thin plastics and fabric laminates while meeting crash, vibration and durability tests. Mass reductions directly extend EV driving range, a metric closely watched by consumers and regulators. Assembly lines also benefit because fewer clips and screws cut cycle times and simplify recycling. As electrification spreads, the weight-saving argument keeps flock solutions on engineering shortlists.

Volatile Isocyanate and Acrylate Feedstock Prices

Adhesive makers rely on petrochemical derivatives whose costs whipsaw with oil and supply-chain shocks. Recent methacrylic-acid oversupply drove a 12% price drop, only for resin producers to impose sharp increases weeks later. Long fixed-price contracts with automotive OEMs limit the ability to pass surcharges through. Smaller formulators are especially exposed because they lack hedging scale and diversified portfolios. Margin uncertainty discourages bold capacity investments during turbulent periods.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Shift Toward Water-Based / VOC-Free Chemistries

- Flocked Thermal-Management Liners in Electric Vehicles Battery Packs

- Tightening Solvent-Emission Regulations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polyurethane captured 38.19% of flock adhesives market share in 2024, buoyed by broad compatibility with automotive substrates and strong thermal resilience. Yet regulatory scrutiny of isocyanates is shifting demand, evidenced by the 6.65% CAGR projected for "other" resin types. The flock adhesives market size for non-isocyanate chemistries is expected to outpace incumbents as acrylic and epoxy alternatives gain traction, driven by inherently lower VOCs and simplified handling. Henkel's bio-based polyurethane containing 71% renewable content demonstrates a 60% CO2 reduction versus standard formulas, signaling how sustainability narratives translate into purchasing criteria.

Regulators require worker training and stricter labelling for diisocyanate products, prompting OEMs to request compliant substitutes. Formulators respond by scaling acrylic dispersions and non-isocyanate polyurethane (NIPU) chemistries that meet adhesion, flexibility and heat-cycling needs without surpassing 0.1% diisocyanate thresholds. Suppliers able to balance compliance, performance and cost will command premium margins as legacy options face phased restriction.

The Flock Adhesives Market Report is Segmented by Resin Type (Acrylic, Polyurethane, Epoxy, Other Resin Types), Application (Automotive, Textiles, Paper and Packaging, Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 51.84% flock adhesives market share in 2024 and is set to grow at 6.19% CAGR through 2030. China anchors regional demand as domestic brands and export-oriented assemblers adopt flocked interiors to elevate perceived quality and meet low-VOC mandates. Sika's new Liaoning and Singapore plants illustrate local capacity investments aimed at shortening lead times and tailoring chemistries for emerging battery-thermal needs. Japan and South Korea complement volume with materials science leadership, scaling epoxy-based and low-formal-emission systems for electronics as well as autos.

North America follows with mature but technologically demanding consumption. OEMs enforce strict sourcing criteria on sustainability and supply-chain transparency, incentivizing rapid adoption of water dispersions and bio-based content. Public infrastructure and military procurement channels support niche flocked applications in rail interiors and aerospace cabin fittings, keeping baseline demand intact despite plateaued vehicle output.

Europe blends tight regulation with innovation leadership. The continent's Circular Economy Action Plan requires removable batteries in devices by 2027, spawning new debondable-adhesive niches where flock must cleanly separate at end-of-life. Companies like Power Adhesives recently introduced certified biodegradable hot-melt systems containing 44% bio-based content, a template likely to spread into flock formulations. South America, the Middle East and Africa collectively represent modest volumes but rising importance as supply chains diversify. Brazil expands automotive assembly capacity that relies on locally sourced flocked trims, while petrochemical integration in the Gulf provides competitive resin feedstock. African markets remain early-stage yet draw investment from consumer-electronics packagers seeking proximity to high-growth urban centers.

- 3M

- Argent International

- Arkema

- Dow

- H.B. Fuller Company

- Henkel AG and Co. KGaA

- International Coatings

- Kissel + Wolf GmbH

- Nyatex

- Parker Hannifin

- Sika AG

- Stahl Holdings B.V.

- SwissFlock AG

- Toyochem Co. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for coated fabrics and luxury finish products

- 4.2.2 Lightweight, low-carbon vehicle interior parts push adoption

- 4.2.3 Regulatory shift toward water-based / VOC-free chemistries

- 4.2.4 Flocked thermal-management liners in electric vehicles battery packs

- 4.2.5 Premium unboxing aesthetics in consumer-electronics packaging

- 4.3 Market Restraints

- 4.3.1 Volatile isocyanate and acrylate feedstock prices

- 4.3.2 Tightening solvent-emission regulations

- 4.3.3 Competition from laser-texturing and alternative finishes

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Polyurethane

- 5.1.3 Epoxy

- 5.1.4 Other Resin Types (Alkyd, Cyanoacrylate, etc.)

- 5.2 By Application

- 5.2.1 Automotive

- 5.2.2 Textiles

- 5.2.3 Paper and Packaging

- 5.2.4 Other Applications (Printing and Graphics, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Argent International

- 6.4.3 Arkema

- 6.4.4 Dow

- 6.4.5 H.B. Fuller Company

- 6.4.6 Henkel AG and Co. KGaA

- 6.4.7 International Coatings

- 6.4.8 Kissel + Wolf GmbH

- 6.4.9 Nyatex

- 6.4.10 Parker Hannifin

- 6.4.11 Sika AG

- 6.4.12 Stahl Holdings B.V.

- 6.4.13 SwissFlock AG

- 6.4.14 Toyochem Co. Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment